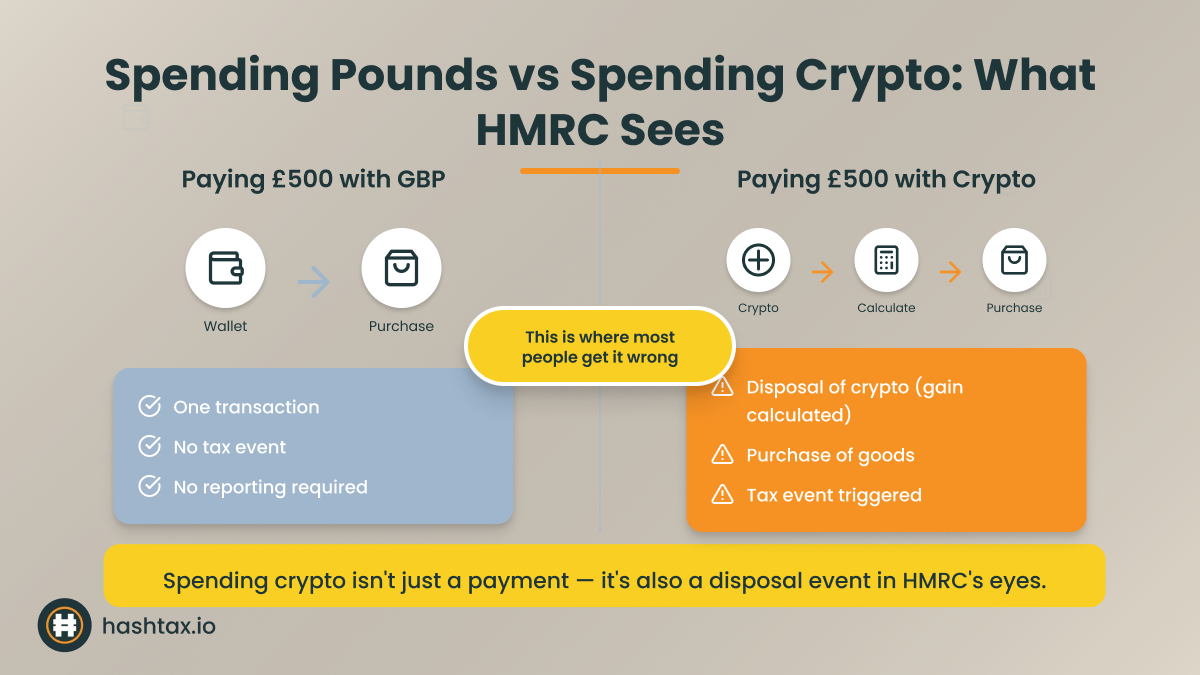

Spending pounds on a laptop triggers no tax. Spending Bitcoin on a laptop triggers Capital Gains Tax.

This is the rule that catches thousands of UK crypto investors every year — and it applies regardless of the purchase amount. A £3.50 coffee bought with Ethereum is, in HMRC's view, a disposal of Ethereum. That disposal requires the same tax treatment as selling crypto on an exchange.

HMRC's position has been clear since 2019: using cryptocurrency to buy goods or services is a disposal. You are treated as having sold your crypto at its current market value, then used the sterling equivalent to make the purchase. If your crypto has appreciated since you acquired it, a taxable gain arises at the moment of the transaction.

The tax mechanics apply identically to:

Every one of these constitutes a disposal. Every one requires a gain or loss calculation.

The confusion is understandable. When you spend crypto, no sterling changes hands. There is no moment that feels like a sale.

You buy coffee, scan your wallet, walk away. Nothing about that transaction feels like it requires a tax return.

But HMRC does not assess tax based on how a transaction feels. It assesses based on the legal character of what occurred. You disposed of an asset. That asset had a cost basis. It had a current market value. The difference between those two figures is your taxable gain.

Several misconceptions make this worse.

Misconception 1: Small purchases don't need reporting.

HMRC does not publish a minimum threshold below which crypto disposals are exempt. Your £3,000 Capital Gains Tax annual exempt amount applies to total gains across all disposals — it is not a per-transaction threshold. Twelve small purchases can collectively exceed the allowance even if each individual transaction appears trivial.

Misconception 2: Crypto debit cards handle the tax.

Crypto debit cards convert your cryptocurrency to sterling at point of sale. This conversion is itself a disposal. The card provider handles the currency conversion; it does not handle your HMRC reporting obligation.

Misconception 3: HMRC cannot see small blockchain transactions.

This is incorrect. HMRC has formal data-sharing agreements with UK-based exchanges. It uses blockchain analytics tools to trace wallet activity. It has issued cryptoasset disclosure campaigns specifically targeting unreported gains. The assumption that small transactions are invisible is a high-risk position.

Consider a retail investor who bought £2,000 of Bitcoin in 2022 at £18,000 per coin. Through 2024 and 2025, they used Bitcoin to make 18 purchases — some small, some significant.

By March 2026, Bitcoin trades at £65,000. The investor has not sold any Bitcoin. They believe they have no tax to report because they have received no sterling.

The reality is different.

Each of the 18 purchases was a disposal of a fraction of their Bitcoin holding. Each disposal was made at the market price prevailing at that moment. The gain on each disposal is the difference between Bitcoin's price at purchase time (their pool average cost) and Bitcoin's price at the moment of each transaction.

Across 18 transactions, the aggregate gain may easily exceed the £3,000 annual exempt amount — in some cases significantly. Two tax years may be involved. Interest has begun to accrue on unpaid tax from the earlier year.

The investor's options at this point are narrowing. Voluntary disclosure is still available and will reduce penalties. But the calculation is now complex, the records are incomplete, and professional assistance is no longer optional.

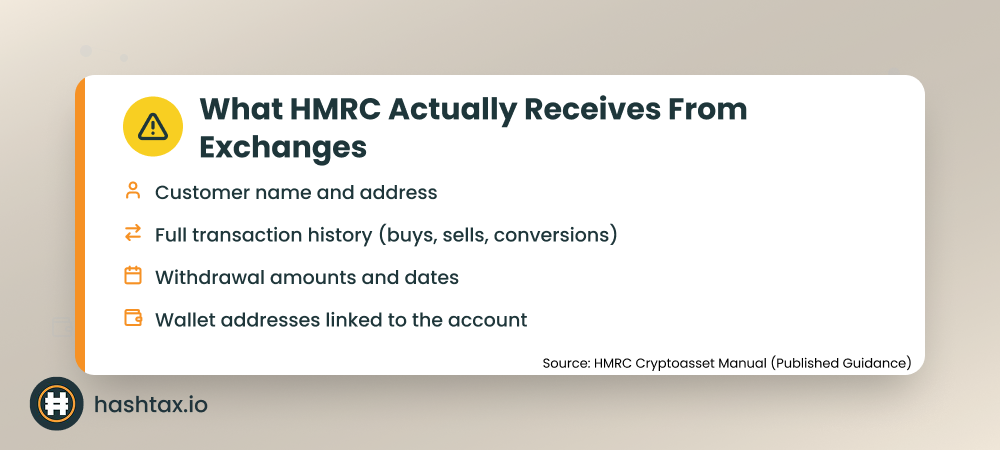

HMRC's capability to identify unreported crypto activity has increased substantially since 2021. Understanding what information they already hold helps explain why voluntary compliance is a far better approach than waiting to be contacted.

UK cryptocurrency exchanges are required to provide HMRC with customer data. This includes Know Your Customer (KYC) information, transaction histories, and withdrawal records.

HMRC's Connect system cross-references this data against Self Assessment returns. Where a taxpayer has exchange activity suggesting disposals but has not declared capital gains, a risk flag is raised. Enquiry letters follow.

Blockchain analytics tools used by HMRC can trace the flow of cryptocurrency between wallets — including from exchange wallets to merchant wallets. The blockchain is a permanent, public record of every transaction. Transactions made years ago remain visible and traceable today.

This does not mean HMRC investigates every transaction. It means that a pattern of undeclared disposals — including purchase transactions — creates a discoverable compliance gap. The longer that gap exists, the larger the penalty exposure grows.

Calculating gains on crypto purchases requires applying the same share pooling methodology used for all other crypto disposals. Each cryptocurrency you hold has a Section 104 pool — a running record of total quantity held and total acquisition cost.

Step 1: Identify every purchase transaction.

List every occasion on which you spent cryptocurrency, including crypto debit card transactions. Include the date, the cryptocurrency used, the quantity spent, and the goods or services received.

Step 2: Determine the sterling value at each transaction.

The gain is calculated using the market value of the cryptocurrency at the precise moment of the transaction. Day-end prices are not sufficient — you need transaction-time valuations. Exchange records and blockchain timestamps are the primary sources.

Step 3: Calculate your pool cost basis for each disposal.

Divide your total cost basis for that cryptocurrency by the total quantity held at the time of each disposal. This gives the average cost per unit for each transaction. Multiply by the quantity disposed to get the allowable cost for that disposal.

Step 4: Apply the identification rules.

Before applying the pool, check whether any cryptocurrency was acquired on the same day as the disposal (same-day rule) or within 30 days after the disposal (30-day rule). These rules take priority over the Section 104 pool and must be applied first.

Step 5: Calculate gain or loss per transaction.

Subtract the allowable cost from the disposal proceeds (sterling value at transaction time). The result is your gain or loss on that disposal.

Step 6: Aggregate across the tax year.

Sum all gains and losses for the tax year. Apply the £3,000 annual exempt amount. Report any net taxable gain through Self Assessment.

If any step in this process involves incomplete records — missing transaction dates, unknown valuations, or uncertain pool balances — the calculation cannot be completed accurately without reconstruction work. Use our Crypto Tax Health Check to assess the completeness of your records before attempting to file.

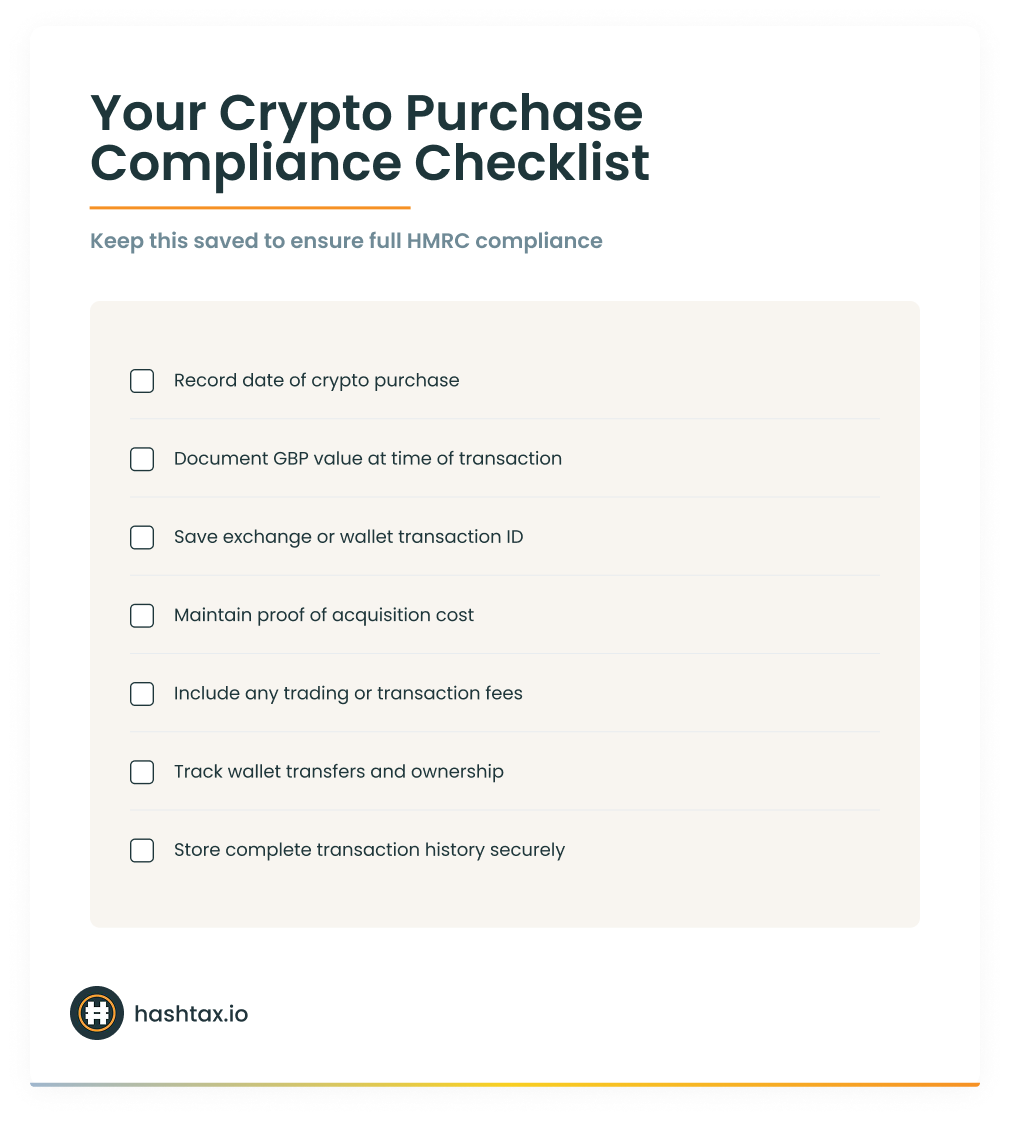

The administrative requirement for crypto purchases is demanding. Every transaction requires documentation captured at the time it occurs. Records collected after the fact are harder to verify and carry less evidential weight with HMRC.

A compliant record for each purchase must include:

Real-time valuation is the most commonly missed requirement. The value must reflect the market price at the moment of the transaction — not the day-end price, the exchange's closing rate, or the value you thought it was worth. Save a screenshot of the price at the time, or record the exchange rate displayed at point of transaction.

Pool calculations must be maintained as a running record. Each disposal reduces your pool. If your pool record is accurate, every subsequent gain or loss calculation is straightforward. If your pool record is missing or incomplete, every subsequent calculation requires reconstruction.

If you have made crypto purchases in previous tax years that were not reported, the appropriate response is voluntary disclosure through HMRC's Digital Disclosure Service — not continued non-disclosure.

Voluntary disclosure substantially reduces penalty exposure. HMRC distinguishes between taxpayers who come forward voluntarily and those who are identified through enquiry. The penalty differential is significant and grows the longer disclosure is delayed.

The resolution process follows a clear sequence.

Step 1: Reconstruct your transaction history.

Obtain full records from every exchange and wallet you have used. Download transaction histories in CSV format where available. Supplement with blockchain records for on-chain transactions.

Step 2: Calculate gains or losses for each tax year.

Apply the share pooling methodology for each year individually. Gains and losses cannot be aggregated across years — each year has its own allowance and its own filing obligation.

Step 3: Determine which tax years require amended returns or new filings.

If you submitted a Self Assessment return for a year in which you had unreported crypto gains, an amendment is required. If you were not in Self Assessment for those years, you may need to register and file returns.

Step 4: Prepare and submit your voluntary disclosure.

The Digital Disclosure Service accepts online submissions. The disclosure must include all years, all gains, and an accurate interest calculation. Incomplete disclosures create additional risk.

Step 5: Pay the outstanding tax and interest.

HMRC charges interest on late-paid tax from the original payment deadline. This interest is not a penalty — it accrues regardless of whether the underpayment was deliberate. Prompt payment after disclosure limits the interest that accrues.

If your purchase history spans multiple years, involves significant sums, or your records are incomplete, professional assistance at steps 1 through 4 is strongly advisable. Errors in voluntary disclosures can result in the disclosure being rejected or penalties being applied at a higher rate.

At HashTax, we have guided many clients through voluntary disclosure for unreported crypto purchase activity. Book a consultation with a HashTax specialist if you believe your position requires resolution.

Crypto purchase taxation looks straightforward in isolation. Applied to a real portfolio — with multiple currencies, partial disposals, incomplete records, and transactions spanning several tax years — it becomes genuinely complex.

The share pooling rules alone require precision. The same-day rule, the 30-day rule, and the Section 104 pool interact in ways that are easy to apply incorrectly. An incorrect pool calculation does not produce an obvious error — it produces a plausible-looking figure that may be materially wrong.

Transaction-time valuations require access to historical price data at a level of granularity that not all sources provide. Missing or approximate valuations expose your filing to challenge if HMRC selects your return for review.

Voluntary disclosures require experience to prepare correctly. A disclosure that omits a year, understates interest, or uses incorrect pooling methodology may not be accepted — and may result in HMRC opening a formal enquiry rather than accepting the disclosure.

HashTax provides expert human analysis at each stage of this process. Our ACCA-registered specialists review your complete transaction history, calculate accurate gains using verified historical price data, and prepare filings that are defensible if challenged. We are not an automated platform. Every case is reviewed by a qualified professional.

Services are delivered by qualified human specialists. HashTax is not an automated platform or software solution.

Book a consultation with a HashTax specialist.

A HashTax specialist will review your crypto purchase history and identify whether you have an unreported liability. We will confirm which tax years are affected, indicate the likely scale of any exposure, and advise on the best path forward.

The assessment takes approximately 30 minutes and carries no obligation to proceed. The earlier you act, the more options remain available.

Book your free compliance assessment

If you have unreported purchases from previous tax years: Book an urgent consultation — voluntary disclosure resolves your position and limits penalty exposure before HMRC contacts you.

If you want to understand your current position first: Complete the Crypto Tax Health Check to identify gaps in your compliance before your next Self Assessment deadline.

If you plan to continue using crypto for purchases: Use the Tax Impact Calculator to model the tax effect of planned transactions before you make them.

Penalties for deliberate non-disclosure are substantially higher than for voluntary disclosure. HMRC's cryptoasset data collection is ongoing — each year that passes adds more exchange data to the risk picture.

Interest on unpaid tax accrues daily from the original due date. A liability that existed for the 2022/23 tax year has been accumulating interest since January 2024. Voluntary disclosure stops the interest clock from the date of payment — not the date of filing.

The investors who achieve the best outcomes are those who address their position before receiving an HMRC enquiry letter, not after.

Visit HashTax to learn more about our professional crypto tax services, or book a consultation to discuss your specific position with a specialist.

Your crypto tax compliance matters. Let's address it properly together.

HashTax Specialists

Our team of ACCA-qualified accountants specializing in UK cryptocurrency taxation. We provide expert guidance on HMRC compliance, tax planning, and professional advisory services for crypto investors and businesses.

.svg)

.svg)