When Alex began using decentralised finance in early 2023, each step felt like a natural progression. Simple token swaps led to lending positions. Lending evolved into liquidity provision. Liquidity provision expanded into yield farming across multiple protocols. By late 2024, his DeFi portfolio had generated significant rewards and profits — and 892 separate tax events.

Alex is not unusual. DeFi is structured in a way that multiplies taxable activity at every level. Each swap is a disposal. Each reward claim is a potential income event. Each liquidity pool entry and exit creates a sequence of transactions. Each protocol migration is a taxable swap. None of these events generate a statement, a tax certificate, or a platform notification. They exist on-chain, permanently recorded, and entirely the user's responsibility to document and report.

HMRC's guidance on DeFi is explicit: the decentralised nature of a protocol does not affect the tax treatment of the underlying transactions. The tax analysis follows what actually happened — not the platform through which it happened. A swap on Uniswap is taxed identically to a swap on a centralised exchange. A yield farming reward is income in the year of receipt, regardless of whether it arrived from a protocol or a custodial platform.

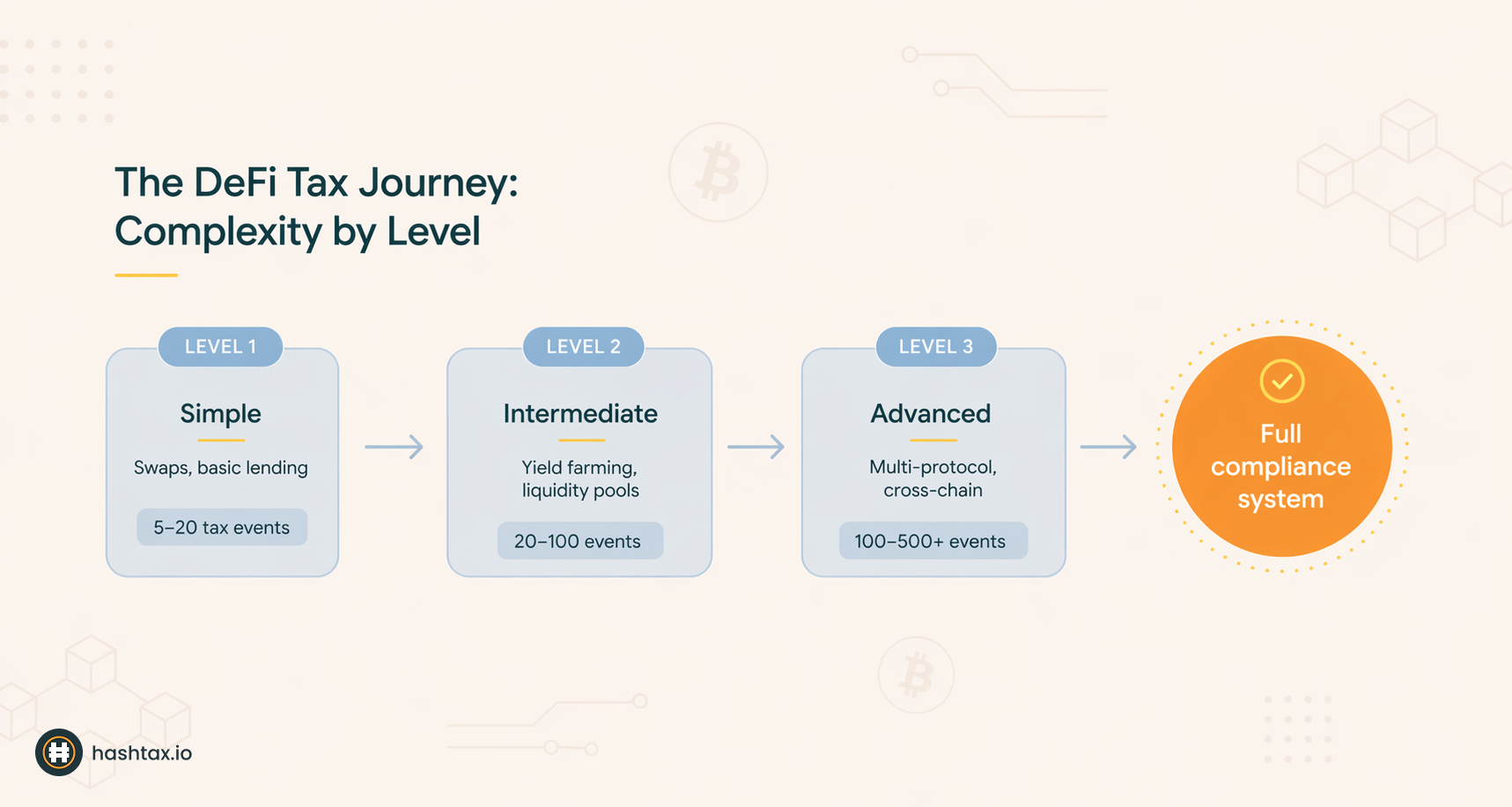

This guide maps the DeFi tax journey level by level — from the entry point of simple swaps through to advanced multi-protocol farming. At each stage, it explains what tax obligations arise, how they are calculated, and what records are needed to support a defensible Self Assessment filing.

Simple DeFi encompasses the entry-level activities that most users encounter first: token swaps on decentralised exchanges and basic single-asset lending on lending protocols.

A DEX token swap — exchanging ETH for USDC on Uniswap, for example — is a disposal of the asset given up and an acquisition of the asset received. The tax treatment is identical to a crypto-to-crypto trade on a centralised exchange. The disposal proceeds are the sterling value of the tokens received at transaction time. The allowable cost is the Section 104 pool cost basis of the tokens given up.

Basic lending — depositing a single asset into a lending protocol and receiving receipt tokens in return — requires careful analysis of whether the deposit itself constitutes a disposal. HMRC's position is that where receipt tokens represent the same underlying asset plus accrued interest (as with aTokens on Aave), the deposit does not create a disposal event. The receipt tokens are treated as representing the original deposit. Interest earned and claimed is taxable income in the year of receipt.

Borrowing against collateral creates no immediate tax event. Taking a USDC loan against ETH collateral is not income. Tax events arise on the subsequent use or disposal of the borrowed assets, and when the collateral position is eventually closed.

At Level 1, each transaction type maps cleanly to established HMRC principles. DEX swaps follow the same capital gains rules as any crypto disposal. Lending interest follows the same income treatment as staking rewards. The transaction count is manageable — 5 to 20 annual events — and each event can be verified against exchange records and blockchain explorers without specialist protocol knowledge.

Gas fees paid in ETH on each transaction are allowable costs that reduce the gain on that disposal. At low transaction volumes, individual gas fees are small. Recording them accurately is worth the effort — they form part of the allowable cost of each transaction and reduce the taxable gain accordingly.

Level 1 DeFi activity is achievable for a methodical investor to document independently. The requirement is consistency: capturing the transaction time, the assets involved, the quantities, and the sterling value at the time of each transaction. A spreadsheet maintained in real time — updated after each transaction rather than reconstructed at year end — is sufficient for most Level 1 users.

Use the Tax Impact Calculator to model the CGT effect of Level 1 swap activity before committing to larger positions.

Level 2 introduces the two activities that most significantly increase DeFi tax complexity: yield farming and liquidity pool (LP) provision.

Liquidity pool provision requires depositing two assets into a protocol in exchange for LP tokens. Each step in this process requires careful tax analysis.

At the point of depositing assets into a liquidity pool, HMRC's guidance is that a disposal may occur if you receive LP tokens that represent a fundamentally different asset from what you deposited. Where LP tokens entitle you to a proportional share of a pool's assets (which change in composition over time), this is treated as an exchange — a disposal of the deposited assets and an acquisition of the LP tokens. Capital Gains Tax applies to any gain on the assets disposed of at the point of deposit.

When you withdraw from the pool, you dispose of the LP tokens and receive back a proportion of the pool's assets (which will differ in composition from your original deposit due to trading activity). This is a further disposal of the LP tokens, and an acquisition of the assets received. Both entry and exit create taxable events.

Yield farming rewards received from liquidity provision — distributed as protocol tokens, governance tokens, or additional LP rewards — are income in the year of receipt at their sterling value on the date received. The two-layer treatment described in the staking tax guide applies: income at receipt establishes the cost basis for future CGT when the reward tokens are eventually disposed of.

Impermanent loss does not create a separate tax event in itself. It is reflected in the reduced value of the assets returned on withdrawal — which affects the disposal proceeds calculation on exit, and therefore the gain or loss on the LP token disposal.

Level 2 activity creates a high volume of taxable events, but each individual event follows a defined rule. The challenge is not ambiguity in the rules — it is the discipline to capture every event accurately and in real time.

Farming rewards that are received and immediately reinvested still require documentation as income at receipt. The reinvestment is a separate acquisition at market value. These two steps — receipt as income, reinvestment as acquisition — must both be recorded. Auto-compounding protocols that reinvest rewards without a manual claim step require particular attention: each automatic reinvestment is an income receipt followed by a reinvestment acquisition, creating two records per compounding cycle.

Investors who establish robust record-keeping practices at Level 2 are significantly better positioned for the complexity that follows at Level 3. The habits built here — transaction-time sterling valuations, protocol-by-protocol documentation, income vs capital event classification — become essential at higher levels where errors compound across hundreds of transactions.

Complete the Tax Complexity Score to assess whether your Level 2 DeFi activity warrants professional review before your next filing.

Level 3 encompasses the DeFi activities that create the most complex tax analysis: multi-protocol farming, governance token receipt and use, cross-chain bridge transactions, and wrapped or synthetic token positions.

Governance token distributions received for participating in protocol governance or as farming rewards are income in the year of receipt. Their sterling value at receipt establishes the cost basis for future CGT calculations. The challenge at this level is that governance tokens are often received from multiple protocols simultaneously, at different frequencies, and may be subject to vesting schedules that affect when receipt — and therefore income — is recognised.

Cross-chain bridge transactions require specific treatment. When you bridge ETH from Ethereum to a Layer 2 or alternative chain, you are not necessarily creating a disposal — if you receive a representation of the same asset (wrapped ETH that is directly redeemable 1:1), HMRC may treat this as a non-disposal transfer. However, where bridging involves exchanging one token for a different token (even if both represent ETH), the exchange is a disposal. The distinction depends on the technical structure of the bridge and is not always obvious from the user interface.

Wrapped tokens — such as wBTC (Wrapped Bitcoin) — typically involve depositing the native asset and receiving a different token in return. HMRC treats this as a disposal of the original asset at the current market value, and an acquisition of the wrapped token at the same value. Unwrapping reverses the process. Each wrap and unwrap creates a taxable event.

Protocol migrations — moving liquidity from one version of a protocol to another, or migrating positions following a protocol upgrade — are taxable disposal events if a different token is received. Even migrations marketed as "seamless upgrades" may require full CGT analysis if the underlying token changes.

At Level 3, the volume of events — often exceeding 100 per tax year across multiple protocols and chains — makes systematic documentation not just advisable but practically necessary for accurate compliance. The key advantage of understanding Level 3 treatment fully is the ability to make informed decisions before executing transactions. Protocol migrations, bridge transactions, and governance participation all carry tax consequences that affect the economics of the activity.

Governance participation in particular creates income that is often overlooked. Where governance tokens are received for voting, participating in governance proposals, or providing liquidity to newer protocols, each receipt is a potential income event. Aggregated across a year of active governance participation, this income may be material and requires reporting.

Level 3 activity is where the gap between what automated tools calculate and what the correct tax position actually is becomes most pronounced. Protocol-specific rules, bridge transaction treatment, and multi-chain valuation requirements require specialist knowledge that general-purpose calculations do not reliably apply.

At this level, the Crypto Tax Health Check serves a different function than for simpler activity. It identifies not just whether records are complete, but whether the correct tax treatment has been applied to each transaction type in your specific protocol mix.

The common thread across all DeFi complexity levels is the record-keeping requirement. HMRC's expectation is that every taxable event is documented with transaction-time sterling valuations, regardless of the protocol or chain on which it occurred.

A compliant DeFi record-keeping system requires four components.

Component 1: Wallet and protocol inventory.

Maintain a complete list of every wallet address and every protocol where you have held positions or executed transactions. Blockchain explorers make every on-chain transaction traceable — but only if you know which addresses to look for. A wallet address inventory is the foundation of complete records.

Component 2: Transaction-level documentation.

For every taxable event, record:

Component 3: Income vs CGT classification.

Each event must be classified as either an income event (subject to Income Tax in the year of receipt) or a capital event (subject to CGT on disposal, with pool cost basis tracking). The classification determines which tax calculation applies. Errors in classification — treating income events as capital events, or vice versa — affect both the rate of tax and the year in which it is due.

Component 4: Running pool records.

For every cryptocurrency and token received through DeFi activity, maintain a running Section 104 pool record that incorporates both market acquisitions and DeFi-acquired tokens. The cost basis of farming rewards received as income feeds directly into the pool at the value reported as income. This linkage between the income record and the pool record prevents both underpayment on future disposals and overpayment through cost basis errors.

DeFi records become exponentially harder to reconstruct the longer they are left. A transaction executed three weeks ago is recoverable with blockchain explorers and reasonable confidence. The same transaction from eighteen months ago requires the same blockchain work, plus the challenge of locating reliable transaction-time price data for potentially obscure tokens.

A monthly maintenance session — reviewing all transactions from the previous month, classifying each, recording valuations while price data is readily accessible, and updating pool records — transforms a year-end reconstruction task into a manageable ongoing process. The discipline is the system. Without it, the records deteriorate in quality with every passing month.

DeFi tax sits at the intersection of rapid protocol innovation, limited HMRC guidance, and high transaction volumes. Each of these factors independently creates compliance risk. Together, they make DeFi the area of cryptoasset taxation where errors are most common and most consequential.

HMRC guidance on DeFi is evolving. Formal published guidance lags behind protocol development. In areas where guidance is absent or ambiguous — the treatment of certain LP token structures, the classification of bridge transactions on specific networks, the timing of income recognition for vesting governance tokens — the correct position requires professional judgement informed by the most recent HMRC communications and case precedent.

Automated tools cannot apply this judgement. They apply rules mechanically, and where the rules are ambiguous or the transaction type is novel, they either misclassify or flag the transaction for manual review. In a portfolio with 300 annual transactions, a significant proportion may fall into categories where automated classification is unreliable.

HashTax provides specialist human analysis for DeFi portfolios at every complexity level. Our ACCA-registered specialists maintain current knowledge of HMRC's evolving DeFi guidance, apply protocol-specific treatment to each transaction type, and document the reasoning behind classification decisions — creating a defensible filing record if HMRC queries any element of the return.

We are not an automated platform. Every DeFi engagement involves qualified professional review.

Services are delivered by qualified human specialists. HashTax is not an automated platform or software solution.

Book a DeFi tax consultation with a HashTax specialist

A HashTax specialist will review your DeFi activity, identify the tax events arising across your protocol interactions, and advise on the correct approach for your Self Assessment filing. We will confirm your current compliance position, identify any years where records need reconstruction, and explain the treatment applicable to your specific protocol mix.

The assessment carries no obligation to proceed.

Book your free DeFi tax assessment

If you have DeFi activity from previous tax years that has not been reported: Book an urgent consultation — voluntary disclosure through HMRC's Digital Disclosure Service addresses unreported DeFi income and capital gains before enforcement begins.

If you are currently active in DeFi and want to confirm your records are adequate: Complete the Tax Complexity Score to understand whether your current DeFi activity level warrants professional review before your next filing.

If you want to understand your estimated DeFi tax liability for the current year: Use the Tax Impact Calculator to model your position based on your transactions to date.

DeFi records deteriorate with time. Transaction-time sterling valuations for obscure tokens become progressively harder to source accurately as months pass. Blockchain records remain permanent — but supporting price data, protocol documentation, and personal recollection of why specific transactions were executed all diminish.

HMRC's blockchain analytics capability extends to DeFi protocols. On-chain transactions — including interactions with smart contracts, LP deposits, reward claims, and bridge transactions — are publicly recorded and traceable. The pseudonymity of wallet addresses is one verified exchange withdrawal away from being resolved.

Addressing DeFi tax proactively — with complete records and correct classification — produces a filing that is both accurate and defensible. The alternative — a filing that is incomplete, or one that has been prepared without protocol-specific expertise — creates risk that grows in proportion to the complexity of the activity and the time elapsed since it occurred.

Visit HashTax to learn more about our professional crypto tax services, or book a consultation to discuss your DeFi tax position with a specialist.

Your crypto tax compliance matters. Let's address it properly together.

HashTax Specialists

Our team of ACCA-qualified accountants specializing in UK cryptocurrency taxation. We provide expert guidance on HMRC compliance, tax planning, and professional advisory services for crypto investors and businesses.

.svg)

.svg)