A crypto investor with one exchange account and no wallet activity has a manageable record-keeping task. Download the annual transaction history, apply the share pooling methodology, and file.

Most active investors are nowhere near that simple. They have accounts spread across two, three, or six exchanges. They hold assets in self-custody wallets. They have interacted with DeFi protocols. Some of those exchanges no longer exist. Some wallets were set up years ago and not touched since. Some transactions were peer-to-peer, with no platform involved at all.

Every one of those assets, across every one of those platforms, represents potential taxable events that HMRC expects you to account for — accurately and completely.

The challenge is not knowing the rules. Most investors understand that disposals are taxable. The challenge is the data: fragmented across platforms, in different formats, with gaps, inconsistencies, and transfers between accounts that look like disposals but are not.

This guide provides a structured, phased approach to resolving that problem — from the initial audit of what you have, through to a sustainable system that keeps your records clean going forward.

HMRC's guidance on cryptoasset record keeping is clear. For every transaction, you are required to maintain:

HMRC specifies that records must be kept for at least 22 months from the end of the relevant tax year for employees, and five years and ten months for the self-employed and those registered for Self Assessment. For most crypto investors, five years and ten months is the applicable standard.

This retention requirement means that the record-keeping gaps of today become the evidence problems of a future enquiry. HMRC's ability to identify cryptoasset activity — through exchange data-sharing, blockchain analytics tools, and its Connect system — means that incomplete records are not simply a filing inconvenience. They are a liability.

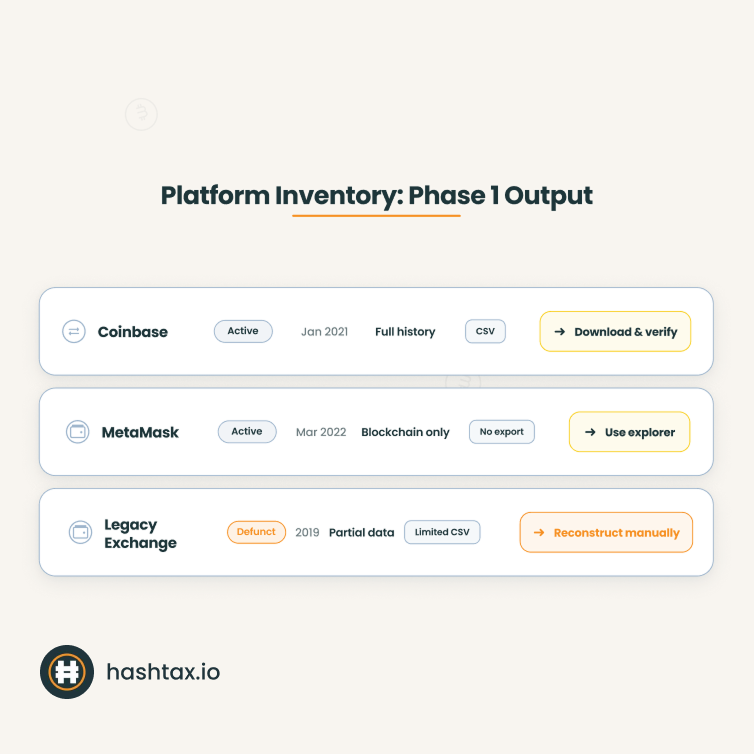

The first phase is the one most investors skip. They assume they know what platforms they have. They rarely do.

The goal of Phase 1 is not to collect any transaction data. It is to produce a complete list of every platform, wallet, and protocol where crypto has ever been held or traded — and to assess what records exist for each.

Search your email history for registration confirmations, KYC notifications, deposit confirmations, and withdrawal alerts from any crypto exchange or wallet service. Many investors discover accounts they had forgotten — exchanges used briefly in 2020 or 2021, test accounts opened during the DeFi summer, referral accounts never actively used.

Any bank transfer to a crypto exchange created a fiat purchase record. Search bank statements from the earliest date you became involved in crypto. Each transfer identifies an exchange that was used. Cross-reference against your email audit.

This includes hardware wallet addresses, software wallet addresses, MetaMask or similar browser extension wallets, and any addresses associated with DeFi protocol positions. Blockchain explorers allow you to check the transaction history of any address — the wallet does not need to still be accessible for its history to be recoverable.

Once you have your complete inventory, assess the record-keeping situation for each:

Phase 2 is the most time-intensive phase. Its output is a complete set of raw transaction records from every source identified in Phase 1.

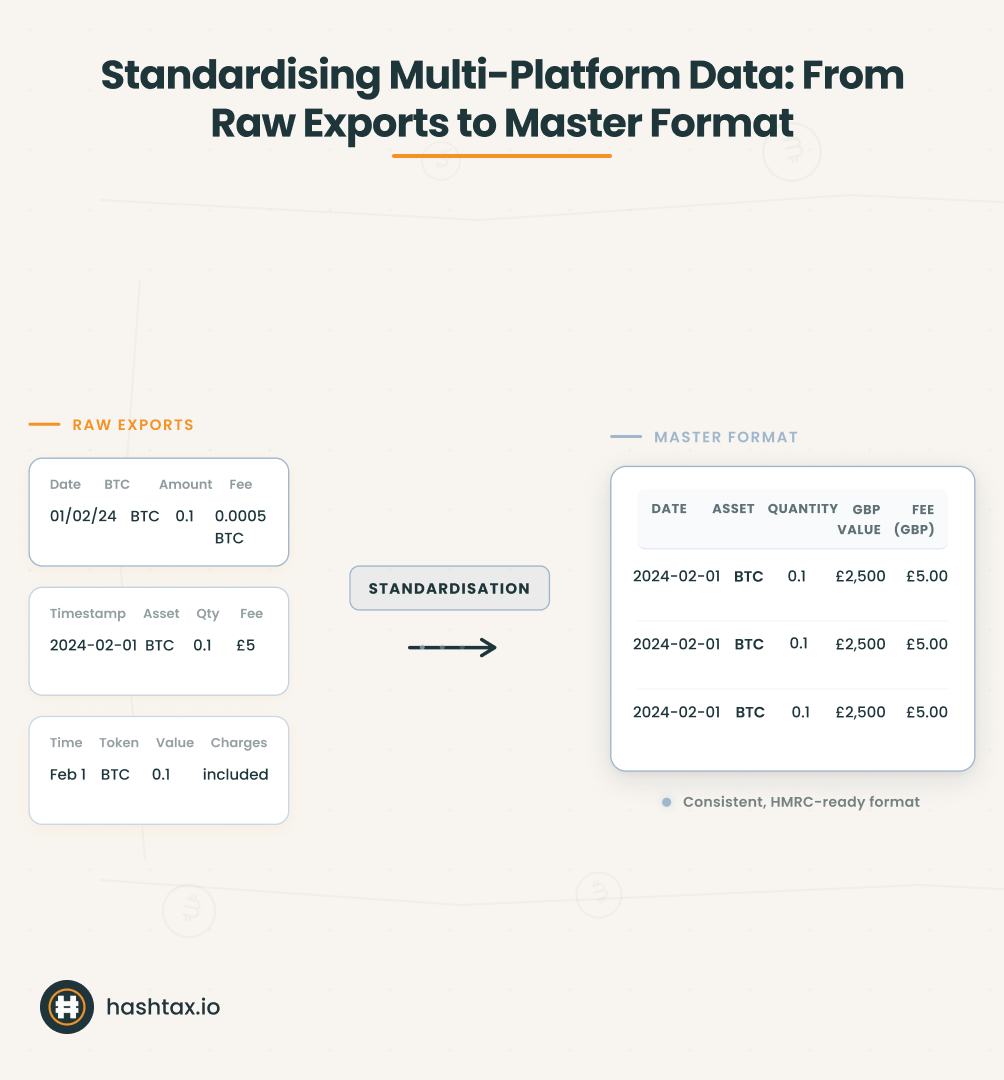

For each exchange, download every available export type. This typically includes trade history, deposit history, withdrawal history, and where applicable, staking or rewards history. Download the full history from the earliest date available — do not limit to the current tax year.

Different exchanges export in different formats. Column headers will not be consistent. Date formats will vary. Some platforms record fees separately; others include them in transaction amounts. Document how each platform formats its data as you download it. This documentation becomes essential during the standardisation step.

For exchanges that no longer operate, or accounts you no longer have access to, blockchain reconstruction is the primary option. Every on-chain transaction is permanently recorded on the public ledger.

To reconstruct using a blockchain explorer:

Step 2a: Identify the wallet addresses associated with the defunct platform account (from old emails, withdrawal confirmation notes, or blockchain traces from other wallets you controlled).

Step 2b: Search those addresses on the relevant blockchain explorer (Etherscan for Ethereum, blockchain.com for Bitcoin, etc.).

Step 2c: Export the transaction history shown. Note that blockchain explorers show all on-chain movements — they will not show internal exchange trades that were never settled on-chain.

Step 2d: For internal exchange trades without on-chain records, HMRC's guidance acknowledges that reconstruction using available evidence is acceptable where original records are genuinely unavailable. Document your reconstruction methodology clearly.

Purchases made directly from individuals, with no exchange involved, require manual documentation. Acceptable supporting evidence includes:

Gather all available supporting evidence and store it alongside your transaction records with a clear reference link.

Before reconciliation can begin, all transaction records must share a consistent structure. Create a master template with the following columns:

Convert every raw export into this format. This step is methodical and takes time. Skipping it makes reconciliation significantly harder and error-prone.

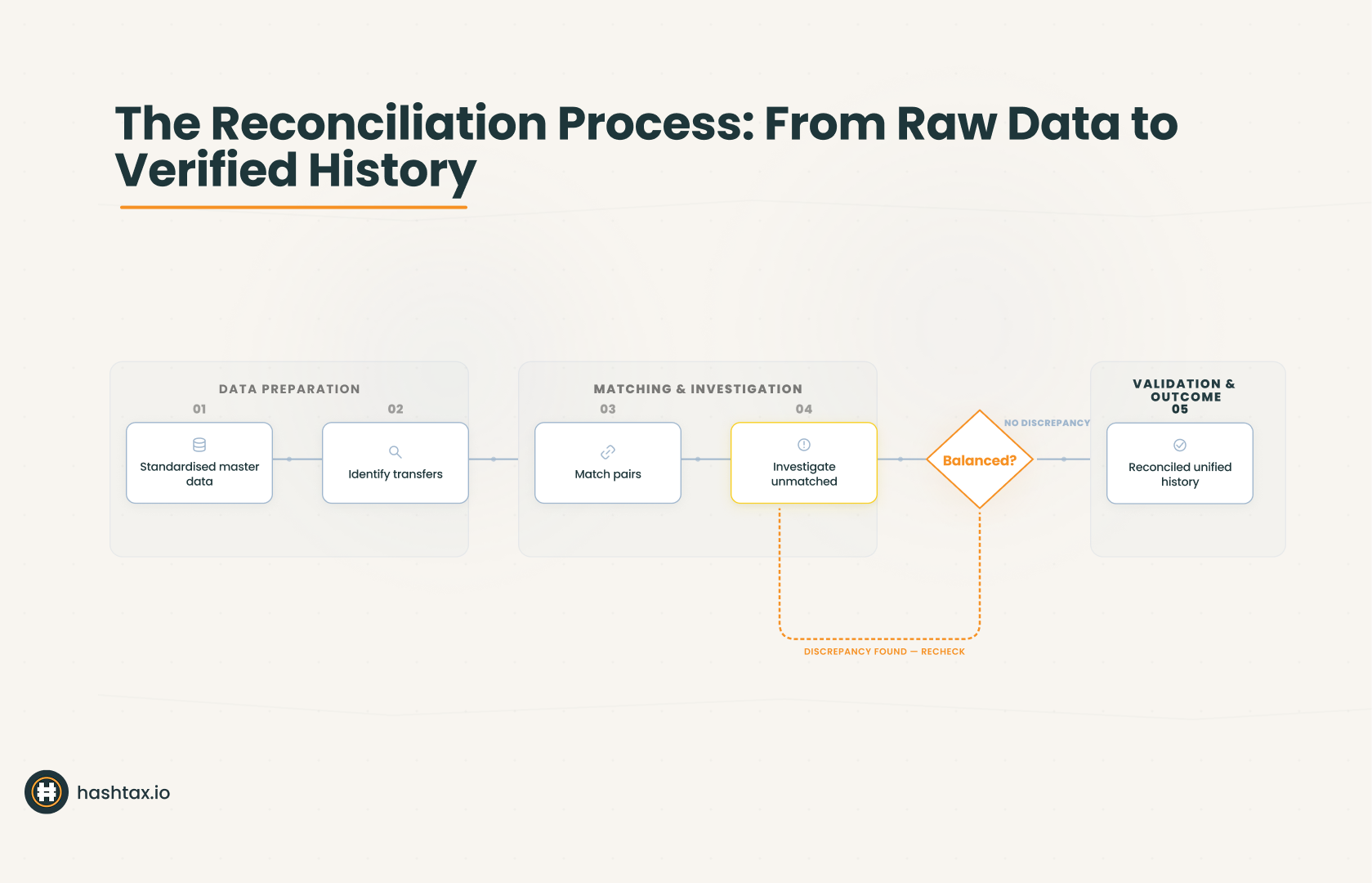

Reconciliation is the process of turning a collection of individual platform records into a single, coherent transaction history. Its central challenge is the transfer problem.

When you move crypto from one exchange to another, or from an exchange to a self-custody wallet, two records are created: an outbound record on one platform and an inbound record on another. Neither record is a taxable disposal. But both must be identified and linked — otherwise the outbound record looks like an unexplained reduction in holdings, and the inbound record looks like an unexplained acquisition with an unknown cost basis.

Unmatched transfers produce incorrect pool calculations. Incorrect pool calculations produce incorrect gain figures. This is the single most common source of material error in multi-platform crypto tax filings.

Filter your master spreadsheet for all transfer types — withdrawals on centralised exchanges, sends from self-custody wallets, deposits on centralised exchanges, receives into self-custody wallets. These are your transfer candidates.

For each outbound movement, identify the corresponding inbound movement on another platform. Matching criteria:

Create a dedicated transfer log documenting each matched pair with both sides' transaction IDs. Mark both transactions as confirmed non-taxable transfers in your master spreadsheet.

Any outbound or inbound movement that cannot be matched requires investigation. Work through these systematically:

Document your investigation process for each unresolved item. Where a transfer cannot be matched but there is strong circumstantial evidence it was an internal transfer (matching amounts, plausible timing, consistent with known trading patterns), document your reasoning clearly. This documentation supports your position if HMRC queries the transaction.

For each platform and each asset, verify that your calculated closing balance matches the platform-reported closing balance. The calculation is:

Opening balance + all acquisitions − all disposals − all fees = calculated closing balance

Any material discrepancy between your calculated and actual closing balance indicates a missing transaction. Investigate before proceeding.

With a verified, reconciled transaction history, you can now construct accurate Section 104 pool records for each cryptocurrency. The pool tracks:

Each acquisition adds to the pool. Each disposal reduces it, using the average cost at the time of disposal. Apply the same-day rule and 30-day rule before consulting the pool for any disposal — as covered in the trading tax guide.

The most valuable outcome of completing Phases 1–3 is not the reconciled history itself. It is the system that prevents the problem from recurring.

Phase 4 establishes a monthly maintenance process that keeps your records current with minimal effort — so that next year's tax preparation begins from a position of order, not chaos.

On a fixed date each month, download transaction history from every active platform covering the previous month. Store exports in a folder structure organised by platform and year. A consistent folder structure means records are always findable:

Crypto Tax Records /

2025-26 /

Coinbase /

Binance /

Self-Custody Wallets /

DeFi Protocols /

Manual Documentation /

2024-25 /

[same structure]

Add each month's new transactions to your master spreadsheet using the standardised format established in Phase 2. Match any transfers that occurred. Update your Section 104 pool records. Verify balances.

Monthly processing keeps each session manageable. Leaving six months of transactions to process in a single session compounds the difficulty of transfer matching — you are less likely to remember why specific movements occurred, and the investigation trail is colder.

Your Section 104 pool should be a living record, updated with each new transaction. A pool record that is only calculated once per year — at filing time — requires reconstructing every transaction for the year in sequence. A pool record updated monthly requires only adding the most recent month's activity.

On 6 April each year, review your complete platform list. Have any platforms closed or announced closure? Have you opened any new accounts? Have you used any new DeFi protocols? Update your inventory and amend your monthly download schedule accordingly.

The goal of this process is not the records themselves. The records are a means to an end.

Complete, reconciled records enable an accurate Self Assessment filing. An accurate filing is the most effective defence against HMRC enquiry. An enquiry into a well-documented position is a straightforward exchange of records. An enquiry into an undocumented position is an open-ended investigation with uncertain outcomes.

Complete records also enable meaningful tax planning. If your pool balances are accurate, you can model the tax impact of planned disposals before making them. You can identify loss positions that could be crystallised before the tax year closes. You can assess whether the annual exempt amount is being used efficiently.

Records reconstructed retrospectively — under time pressure, before a filing deadline, or in response to an HMRC letter — are always less reliable than records maintained contemporaneously. They are also significantly more expensive to produce with professional assistance when the original data is partially missing.

At HashTax, the clients who arrive with complete, well-organised records receive a faster, more accurate service. The analysis focuses on tax strategy and optimisation rather than data reconstruction.

This 8-week plan is achievable for an organised, methodical investor willing to invest the time. For many active traders, however, the combination of volume, complexity, and time available makes professional assistance the more practical option.

The question is not whether your records are worth reviewing professionally. It is what that review provides.

A HashTax multi-platform review covers the full reconciliation process — transfer matching, pool verification, balance reconciliation, and identification rule application — using the same methodology described in this guide. The difference is that our specialists do this regularly, have access to institutional price data for sterling valuation, and know where the common gaps and errors occur for each platform type.

The review output is a verified transaction history, accurate Section 104 pool records, and a Self Assessment filing that reflects your actual tax position. It also identifies any years where gaps in records suggest voluntary disclosure may be appropriate — before HMRC raises the issue.

The question of crypto tax software versus professional review is worth addressing directly. Software tools can automate data import and produce calculations quickly. They rely entirely on the quality of the data fed into them. Transfer mismatches, incorrect categorisations, and identification rule misapplication produce plausible-looking but incorrect outputs. Professional review catches these errors. Software alone cannot.

Services are delivered by qualified human specialists. HashTax is not an automated platform or software solution.

A HashTax specialist will review your current record-keeping position and identify the gaps that need to be resolved before your next Self Assessment filing. We will confirm which platforms require attention, whether any years carry unresolved transfer discrepancies, and advise on the most efficient path to a compliant position.

The assessment carries no obligation to proceed. Understanding what your records currently support — and what they do not — is the essential first step.

Book your free records assessment

If you have multiple years of unreconciled records across several platforms: Book an urgent consultation — multi-year reconstruction takes time, and the January 31 filing deadline does not move.

If you want to understand your current compliance position before beginning the 8-week plan: Complete the Crypto Tax Health Check to identify the specific gaps in your records before you start.

If you want to estimate your tax liability once your records are complete: Use the Tax Impact Calculator to model your CGT position based on your reconciled transaction history.

HMRC's record-keeping requirements apply to every tax year in which you held or traded crypto. Records that do not exist cannot be produced in response to an enquiry. Reconstruction from incomplete data produces results that are difficult to defend under scrutiny.

The 8-week plan in this guide requires consistent effort applied over two months. Beginning in March leaves insufficient time before the April 5 tax year-end to implement the full system and still act on the planning opportunities your completed records may reveal.

Beginning now — with a clear inventory and a structured approach — gives you the information you need before decisions about the current tax year have to be made.

Visit HashTax to learn more about our professional crypto tax services, or book a consultation to discuss your record-keeping position with a specialist.

Your crypto tax compliance matters. Let's address it properly together.

HashTax Specialists

Our team of ACCA-qualified accountants specializing in UK cryptocurrency taxation. We provide expert guidance on HMRC compliance, tax planning, and professional advisory services for crypto investors and businesses.

.svg)

.svg)