Sarah began collecting NFTs in 2021. Over three years she bought, traded, and sold dozens of pieces — some purchased with Ethereum, some swapped directly for other NFTs, some sold for significant gains. She assumed that because she was dealing in digital art rather than straightforward cryptocurrency, different rules might apply.

They do not.

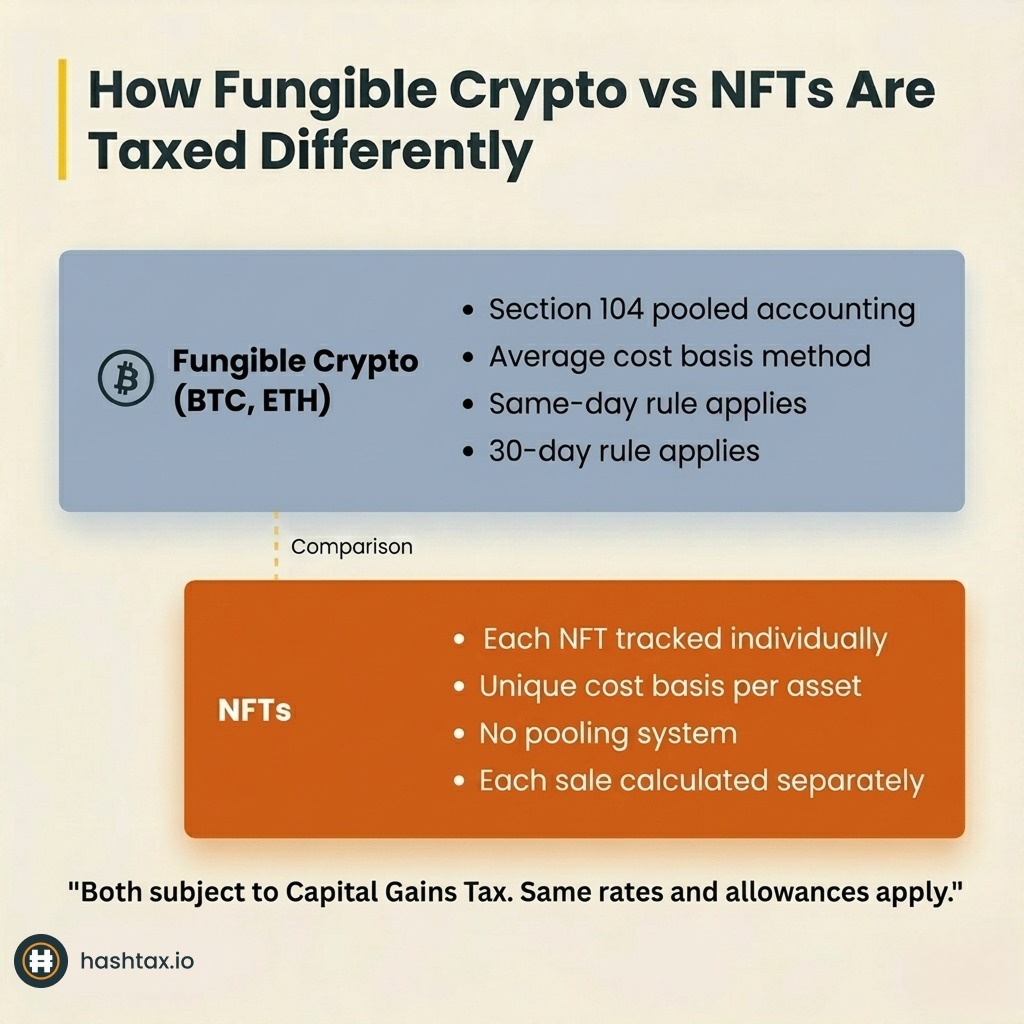

HMRC treats NFTs as cryptoassets. The same Capital Gains Tax framework that applies to Bitcoin and Ethereum applies to NFTs — with one important structural difference. Where fungible cryptocurrencies are pooled using the Section 104 methodology, NFTs are unique assets. Each NFT is valued and tracked individually. There is no pooling. Every acquisition establishes an individual cost basis, and every disposal is calculated against that specific asset's cost.

This individual asset treatment has significant practical consequences. A holder of 40 NFTs has 40 separate cost bases to maintain. A holder who traded extensively over two or three years may have dozens of disposal calculations to complete — each one requiring transaction-time sterling valuations and accurate record-keeping that most collectors never implemented at the time.

The sections below follow the NFT lifecycle — from acquisition through to disposal — with the tax treatment applicable at each stage.

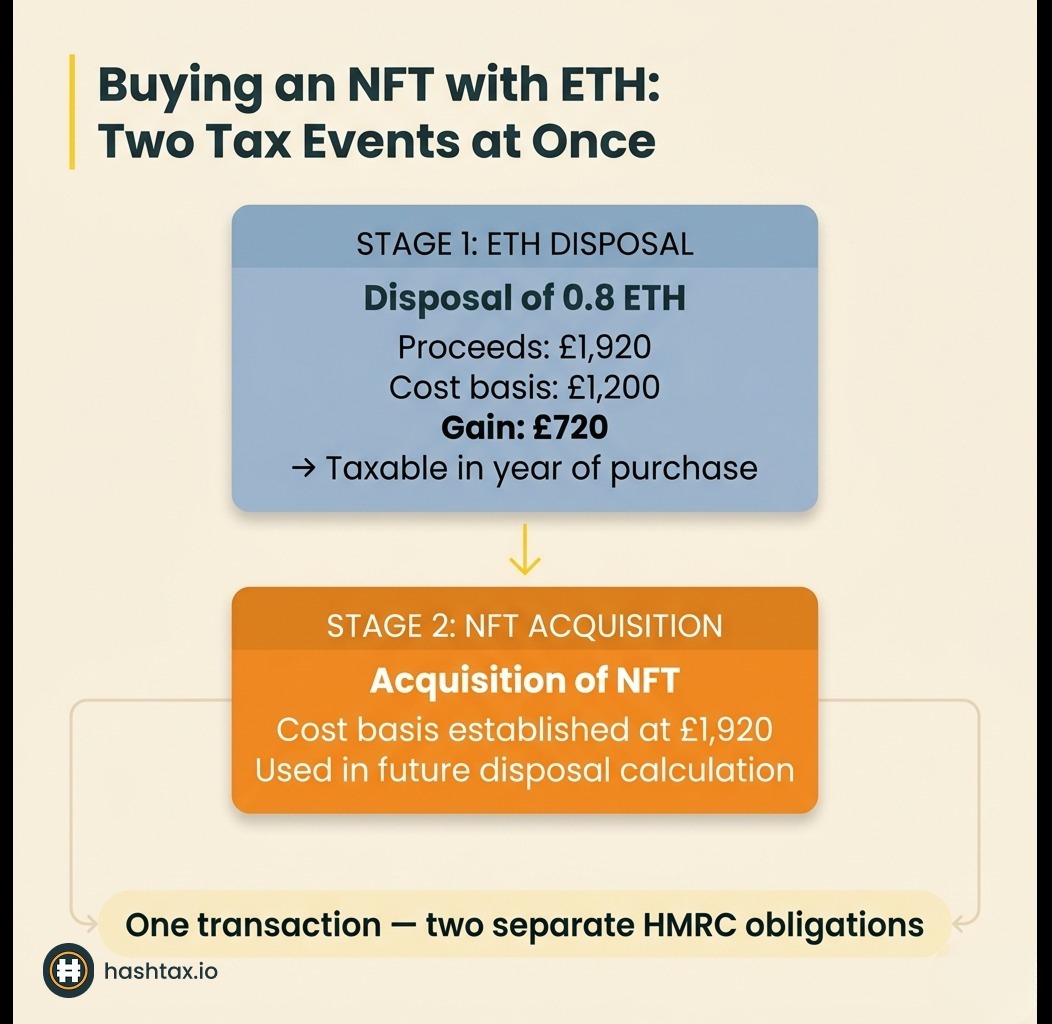

The most common way to acquire an NFT is to purchase it with cryptocurrency. When you do this, two tax events occur simultaneously:

The disposal of your cryptocurrency is a Capital Gains Tax event. If the Ethereum you used to purchase the NFT had appreciated since you acquired it, you have realised a capital gain on that Ethereum at the moment of the NFT purchase — regardless of whether you have received any sterling.

Sarah purchased an NFT in March 2022 for 0.8 ETH. She had acquired that ETH at an average pool cost of £1,500 per coin. ETH was trading at £2,400 at the point of purchase. The sterling value of the NFT was £1,920 (0.8 × £2,400). On the Ethereum she spent, she realised a gain of £720 (£1,920 − £1,200 allowable cost). That gain was taxable in 2021/22, the year of the transaction.

This is the tax event most NFT collectors miss entirely. The focus is on whether the NFT itself has gone up in value. The taxable event on the cryptocurrency used to fund the purchase goes unnoticed.

Purchasing an NFT directly with pounds — where a platform allows sterling payment — creates no immediate Capital Gains Tax event. The purchase establishes the NFT's cost basis at the sterling amount paid, including any platform fees or gas costs that form part of the acquisition.

This is the simpler acquisition route from a tax standpoint. The cost basis is clearly denominated in sterling at the time of purchase, with no secondary calculation required.

Receiving an NFT as a gift establishes your cost basis at the market value of the NFT on the date of receipt. If the NFT was gifted by a connected party — a spouse, civil partner, or certain company relationships — different rules may apply.

Where an NFT is received in exchange for a service or as a form of payment, it may be treated as income rather than a capital acquisition. The tax treatment in that case follows the income rules described in the creators section below.

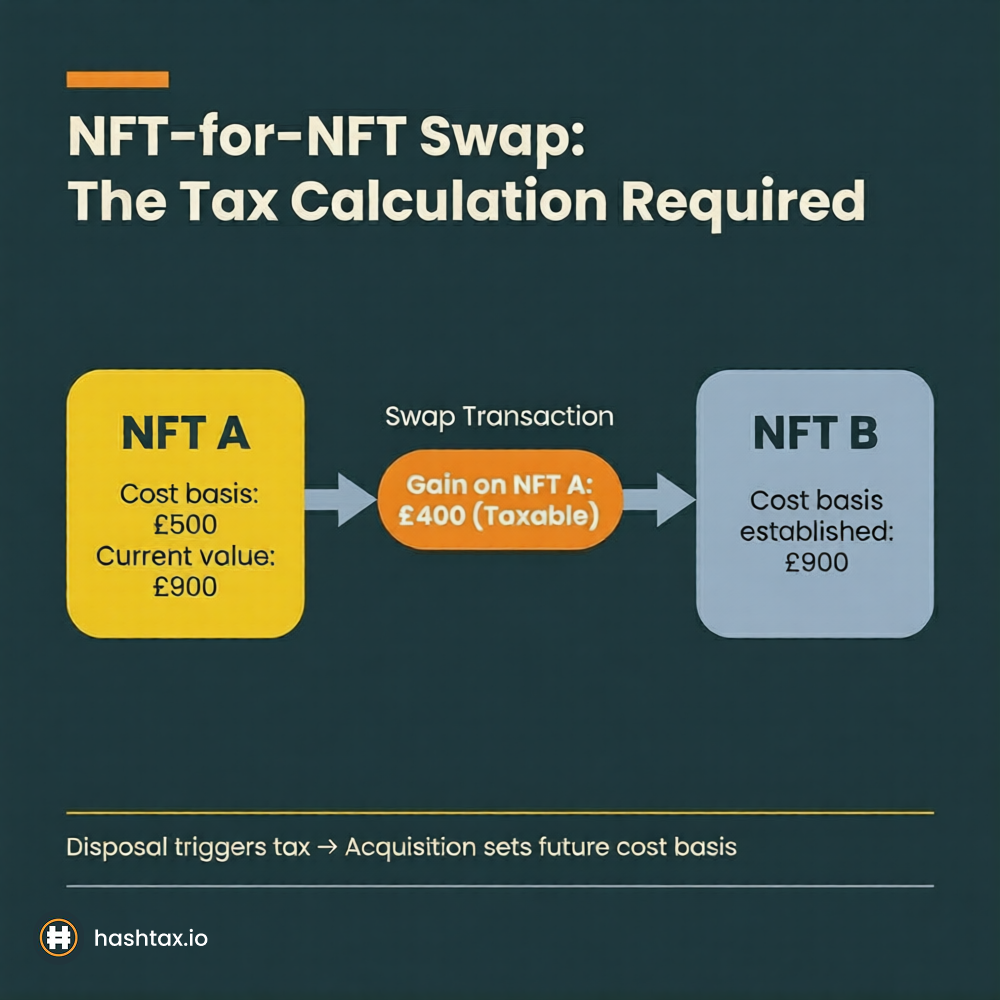

Exchanging one NFT for another is a disposal of the first NFT at its current market value, and an acquisition of the second at the same value. Capital Gains Tax applies to any gain on the NFT disposed of, calculated against its original cost basis.

This is the NFT equivalent of the crypto-to-crypto trade rule. No sterling changes hands — but HMRC treats the transaction as if you had sold the first NFT for its sterling market value and used those proceeds to purchase the second.

At the time of the swap, you need to know:

The gain is calculated as disposal proceeds minus allowable cost. The new NFT's cost basis is its market value at the time you received it.

An active NFT trader who executes several swaps across a tax year quickly accumulates a chain of interdependent calculations. Each disposal's proceeds feed into nothing — but each acquisition's cost basis is critical to every future disposal from that asset.

If Sarah traded twelve NFTs over the course of 2022/23, she had twelve disposal calculations to complete. Each required the original cost basis of the NFT disposed of, the sterling value of the consideration received, and transaction-time valuations for both sides of every swap.

The complexity compounds when NFTs are swapped multiple times. An NFT acquired at £500, traded to NFT B when its value was £900, which was later sold for £1,200, requires tracking the full chain to calculate that the gain on the final sale was £300 — not £700.

Holding an NFT does not trigger any tax event. Unrealised gains on NFTs — however large — are not taxable until disposal. The April 5 tax year-end creates planning opportunities: if you are approaching the £3,000 annual Capital Gains Tax exempt amount, you may wish to consider whether crystallising a loss position before the year closes makes sense for your overall position.

Use the Tax Impact Calculator to model the effect of any planned NFT disposals before the tax year ends.

Selling an NFT for cryptocurrency or sterling produces a disposal at the market value of the consideration received. The Capital Gains Tax calculation is:

Disposal proceeds (sterling value of crypto or cash received) minus allowable cost (original acquisition cost plus any acquisition costs) = gain or loss

Allowable costs include the original purchase price of the NFT, platform fees paid on acquisition, and gas fees paid to complete the acquisition transaction. Platform fees paid on sale are deductible from disposal proceeds.

Where the sale proceeds are received in cryptocurrency rather than sterling, you must determine the sterling value of that cryptocurrency at the exact time the transaction completed. This is not the day-end price or the weekly average — it is the market price at transaction time.

This requirement creates a record-keeping obligation at the point of sale. Save the exchange rate or price feed at the time of the transaction. Blockchain timestamps provide the reference point; price feed screenshots provide the valuation.

Net capital gains across all disposals in a tax year — including NFT disposals — are assessed against the £3,000 annual exempt amount. If your total net gains (across all cryptoassets, shares, and other chargeable assets) remain below £3,000, no Capital Gains Tax is payable.

Losses on NFT disposals can offset gains from the same tax year. A loss crystallised by selling an NFT at below its acquisition cost reduces your net gain figure and may bring you within the exempt amount. Losses that exceed gains in one year can be carried forward indefinitely.

.png)

If you hold NFTs that have declined in value below your acquisition cost, disposing of them before 5 April crystallises those losses and reduces your net taxable gain for 2025/26. This is a legitimate planning strategy — losses are recognised at disposal, and the April 5 deadline is the last opportunity to act within the current tax year.

The 30-day rule does not apply to NFTs in the same way it applies to fungible cryptocurrencies — because each NFT is a unique asset. Selling NFT A and reacquiring a different NFT B does not trigger the reacquisition matching rules. However, selling an NFT and reacquiring the identical NFT from the same collection at the same serial number or token ID within 30 days would attract scrutiny. Professional advice is warranted before implementing any loss harvesting strategy on NFTs you intend to reacquire.

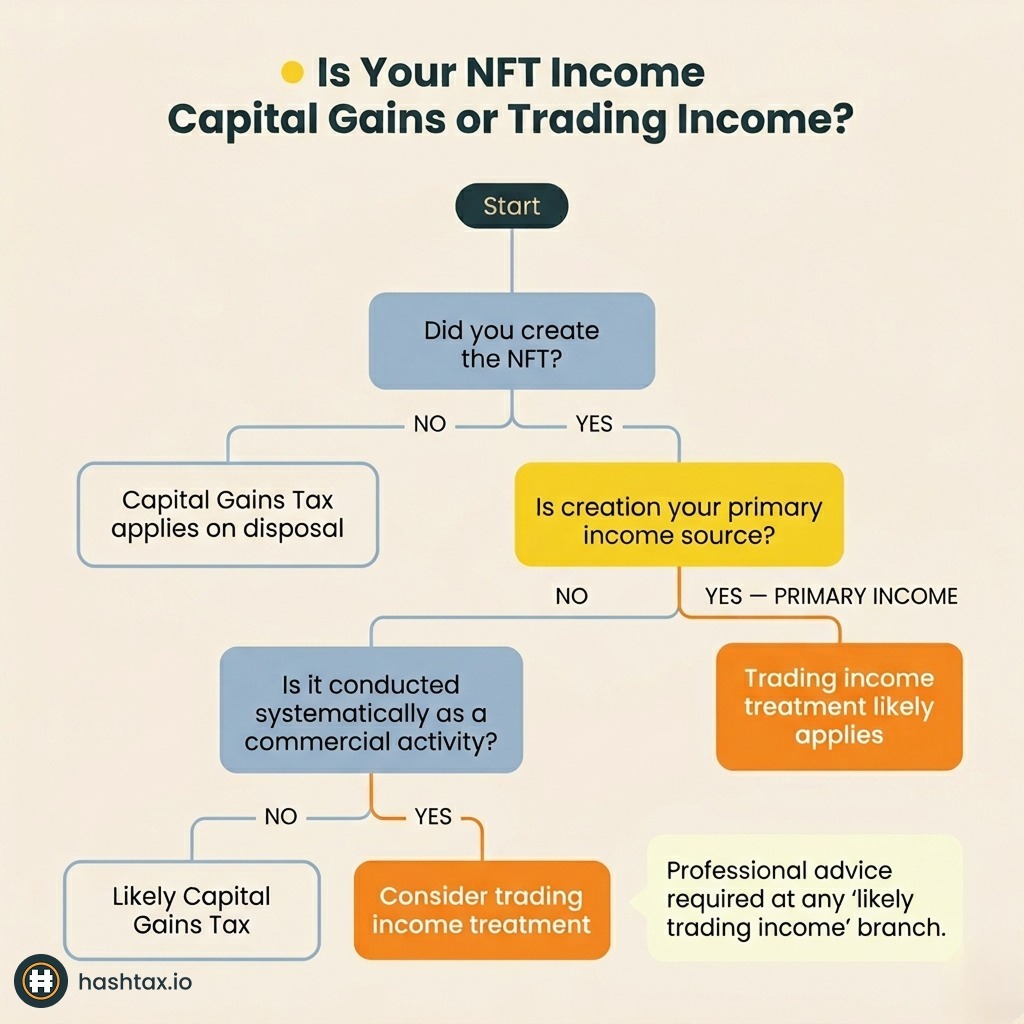

Artists, developers, and studios who create and sell NFTs face a different tax analysis. Where an individual creates NFTs as part of a business or regular commercial activity, the proceeds from primary sales may be treated as trading income rather than capital gains.

HMRC applies the same badges of trade test to NFT creation that it applies to other commercial activities. Relevant factors include:

A hobbyist who mints one NFT and sells it is unlikely to be treated as trading. A developer who launches regular collections, generates consistent sales income, and operates in a business-like manner is more likely to face trading income treatment.

The distinction carries material consequences. Trading income is subject to Income Tax at your marginal rate, plus Class 4 National Insurance contributions. There is no annual exempt amount equivalent. Trading losses, however, can be offset against other income — which may be advantageous for creators in loss-making years.

Secondary royalties — where an NFT contract automatically pays the creator a percentage of each subsequent sale — are a separate consideration. These payments are likely income at receipt, valued at the sterling equivalent on the date received.

Transferring an NFT as a gift is a disposal at market value on the date of transfer, regardless of whether any consideration is received. If the NFT has appreciated since acquisition, Capital Gains Tax applies to the gain at that market value.

The exception applies to transfers between spouses and civil partners. These are treated as no gain, no loss disposals — the recipient acquires the NFT at the original donor's acquisition cost. Capital Gains Tax is deferred until the recipient disposes of the NFT.

An NFT lost due to a lost wallet key, hacked account, or platform failure may qualify for a negligible value claim if it can be demonstrated that the asset has become worthless or the loss is permanent. HMRC's negligible value process allows a deemed disposal at nil proceeds, crystallising a capital loss that can be offset against gains elsewhere.

The burden of demonstrating negligible value rests on the claimant. Documentation of the loss event — wallet failure, platform insolvency notices, evidence of permanent inaccessibility — is required to support the claim.

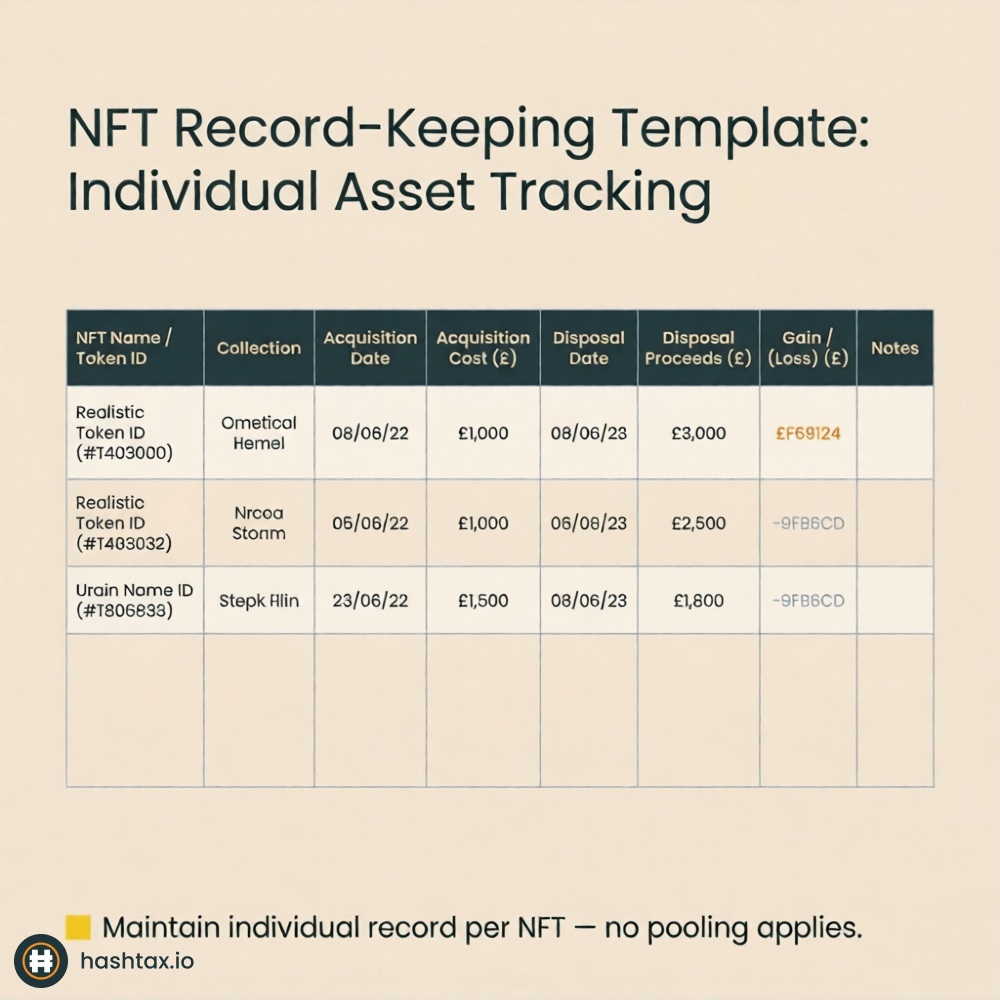

Because each NFT is a unique asset rather than a fungible token, the record-keeping obligation for NFTs is particularly detailed. There is no pooling to simplify the calculation — every individual NFT requires its own complete record.

For each NFT you hold or have held, maintain:

These records must be maintained for five years and ten months from the Self Assessment filing deadline for the relevant tax year. For NFT activity in 2021/22, records should be retained until at least January 2029.

Transaction-time sterling valuations are particularly challenging for NFT swaps, where both sides of the transaction must be valued simultaneously. Where NFT prices are illiquid and price feeds unreliable, HMRC accepts a reasonable and consistent valuation methodology — but that methodology must be documented and applied uniformly.

Complete the Crypto Tax Health Check to assess whether your current NFT records are complete enough to support an accurate Self Assessment filing.

NFT tax combines most of the complexities found elsewhere in cryptoasset taxation — CGT on fungible crypto (when buying with ETH), unique-asset tracking (for the NFTs themselves), potential income treatment (for creators and royalties), and manual record reconstruction (for collectors who did not keep contemporaneous records).

The interaction between these elements is where errors occur. A collector who correctly calculates their NFT gain but ignores the CGT event on the Ethereum used to purchase it is underreporting. A creator who reports all proceeds as capital gains when trading income treatment should apply has misclassified the income type entirely.

At HashTax, our ACCA-registered specialists review the full picture — the cryptocurrency used for acquisitions, the NFT disposal calculations, the creator income question, and the royalty treatment — and prepare a Self Assessment filing that addresses each element correctly. We are not an automated platform. Every engagement involves qualified human analysis.

Services are delivered by qualified human specialists. HashTax is not an automated platform or software solution.

Book an NFT tax consultation with a HashTax specialist

A HashTax specialist will review your NFT activity, identify the tax events arising at each stage of your collecting or trading history, and advise on the correct approach for your Self Assessment filing. We will confirm which years require reporting and whether any records need reconstruction.

The assessment carries no obligation to proceed.

Book your free NFT tax assessment

If you have bought, traded, or sold NFTs in previous tax years without reporting: Book an urgent consultation — voluntary disclosure through HMRC's Digital Disclosure Service resolves unreported activity and limits penalty exposure.

If you are currently holding NFTs and want to understand your compliance position: Complete the Crypto Tax Health Check to identify gaps in your records before your next Self Assessment deadline.

If you want to model the tax impact of planned NFT disposals before April 5: Use the Tax Impact Calculator to estimate the Capital Gains Tax effect of any disposals you are considering in the current tax year.

HMRC's data-sharing arrangements with UK-based platforms extend to NFT marketplaces operating in the UK. Blockchain analytics tools can trace NFT transactions through public on-chain records. The pseudonymity of wallet addresses is not the same as anonymity — a single connection between a wallet and a verified identity (an exchange KYC, a bank transfer, a public social media post) is sufficient to link a complete transaction history to a named individual.

Voluntary disclosure, made before HMRC contacts you, attracts meaningfully lower penalties than disclosure made after an enquiry opens. The correct time to address unreported NFT activity is before an enquiry letter arrives — not after.

Visit HashTax to learn more about our professional crypto tax services, or book a consultation to discuss your NFT tax position with a specialist.

Your crypto tax compliance matters. Let's address it properly together.

HashTax Specialists

Our team of ACCA-qualified accountants specializing in UK cryptocurrency taxation. We provide expert guidance on HMRC compliance, tax planning, and professional advisory services for crypto investors and businesses.

.svg)

.svg)