James had been investing in Bitcoin and Ethereum for three years, building a portfolio worth £47,000. When he finally sat down to file his Self Assessment, panic set in.

Which transactions needed reporting? Was his staking income taxable now or later? Would HMRC consider him a trader or an investor?

After spending an entire weekend buried in HMRC guidance documents, James still wasn't confident he'd gotten it right. The potential penalties for getting it wrong kept him awake at night.

This comprehensive guide provides the clarity James needed. Whether you hold a simple Bitcoin position or trade across multiple DeFi protocols, understanding UK crypto tax rules transforms anxiety into confidence.

At HashTax, we've analysed thousands of crypto portfolios for UK investors, and this guide distills everything you need to know about cryptocurrency taxation in one authoritative resource.

Not sure where you stand? Take our free Crypto Tax Health Check to assess your compliance status in 3 minutes.

.png)

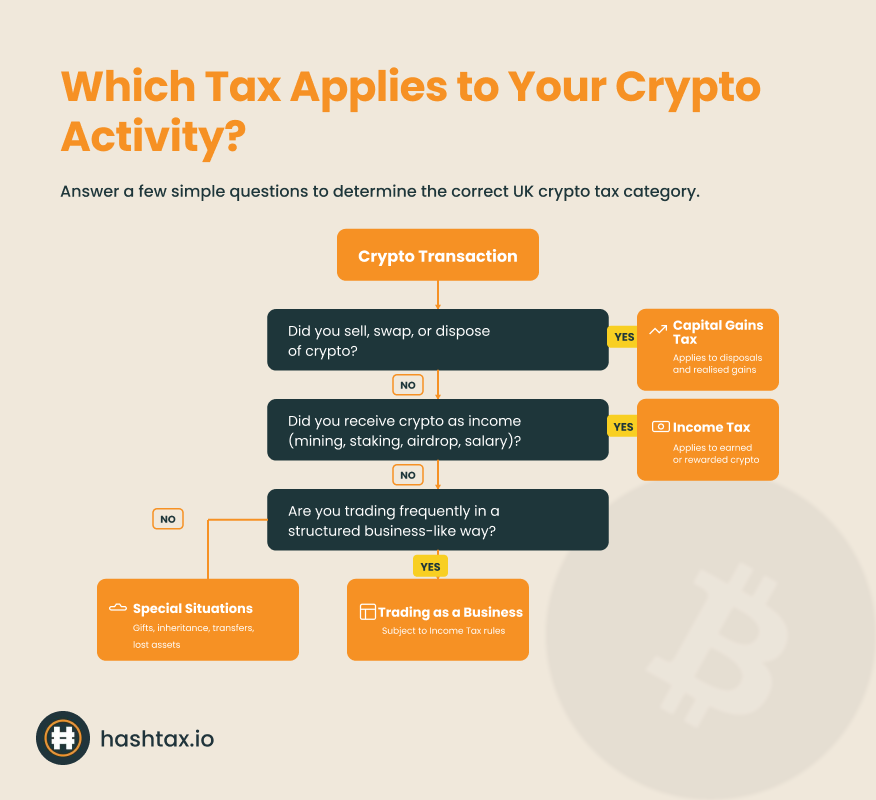

The UK tax treatment of cryptocurrency depends entirely on your specific activities and circumstances.

HMRC doesn't view all crypto transactions the same way, and this is where most confusion begins.

Understanding which category your activities fall into determines everything from your tax rates to your reporting obligations.

HMRC's foundational position is straightforward: cryptocurrency is property, not currency or money. This single principle drives all subsequent tax treatment.

When you dispose of cryptocurrency by selling it, swapping it for another crypto, or using it to purchase goods, you've made a disposal that may trigger tax obligations.

The nature of those obligations depends on whether you're investing, earning income, or running a business.

For most UK crypto holders, tax obligations fall into four distinct categories:

Each category carries different rates, allowances, and reporting requirements.

The 2025/26 tax year brings specific rates and thresholds every crypto holder must know. Capital Gains Tax allows a £3,000 annual exemption before tax applies at either 10% or 20% depending on your overall income.

Income Tax applies to crypto earnings using your marginal rate, which ranges from 0% to 45% based on total income.

Understanding these fundamentals prevents costly mistakes that HMRC increasingly scrutinises through enhanced crypto enforcement capabilities.

Capital Gains Tax represents the most common tax treatment for UK crypto holders.

If you're buying cryptocurrency as an investment and occasionally selling for profit, this category almost certainly applies to you.

HMRC treats each disposal of cryptocurrency as a potential capital gain or loss, requiring you to track your acquisition costs and disposal proceeds meticulously.

Every time you dispose of cryptocurrency, you must calculate whether you've made a gain or loss.

Disposals include:

The only exception is transfers between your own wallets, which HMRC doesn't consider disposals.

This means even crypto-to-crypto swaps within your portfolio trigger taxable events requiring documentation.

Your capital gain equals the disposal proceeds minus your acquisition cost and any allowable expenses like trading fees.

The calculation sounds simple, but complexity emerges with multiple acquisitions at different prices.

The 2025/26 tax year provides a £3,000 annual Capital Gains Tax allowance that applies across all your disposals, not just cryptocurrency.

This exemption represents the amount of gains you can realise completely tax-free each year.

Understanding how to maximise this allowance delivers immediate tax savings for strategic investors.

The £3,000 threshold applies to your total gains after deducting losses. If you realise £8,000 in crypto gains and £2,000 in losses from other investments, your net gain of £6,000 uses £3,000 of your allowance, leaving £3,000 subject to Capital Gains Tax.

Strategic timing of disposals across tax years allows you to utilise your allowance fully each year rather than wasting it.

Many investors unknowingly forfeit thousands of dollars in tax-free capital gains by not actively managing their CGT allowance.

Someone holding appreciated crypto could sell £3,000 worth each tax year completely tax-free, then immediately repurchase if desired (subject to bed-and-breakfast rules).

Over five years, that's £15,000 of gains realised without paying a penny in tax.

The allowance doesn't roll over—unused portions from previous years disappear forever. If you only realised £1,000 in gains this year, you can't carry forward the unused £2,000 to next year.

This use-it-or-lose-it structure creates strategic opportunities for investors with unrealised gains to harvest profits systematically while minimising lifetime tax obligations.

Take our Tax Impact Calculator to estimate your 2026 tax liability based on your transactions.

Once your gains exceed the £3,000 annual exemption, Capital Gains Tax applies at rates determined by your overall income position.

The rate you pay depends on your combined income from all sources plus your crypto gains.

If you earn £45,000 from employment and realise £10,000 in crypto gains, your total income of £55,000 pushes you into higher-rate territory.

The first £5,270 of gains (the gap between £45,000 and the £50,270 threshold) faces 10% tax, while the remaining £4,730 faces 20% tax. This band straddling creates complex calculations requiring careful planning.

Strategic investors optimise their rate exposure through timing. Someone expecting a lower-income year due to career changes or a sabbatical might accelerate crypto disposals into that year to benefit from 10% rates rather than 20%.

Conversely, high earners approaching retirement might defer disposals until income drops, potentially saving thousands in tax through rate arbitrage. The difference between 10% and 20% CGT rates proves substantial at scale.

On a £50,000 crypto gain above your allowance, the rate difference equals £5,000 in tax—enough to justify professional strategic planning. Understanding your marginal CGT rate enables informed decisions about when to realise gains, how much to realise annually, and whether deferring disposals makes sense financially.

HMRC's same-day rule prevents you from selling cryptocurrency and repurchasing it on the same day to crystallise losses while maintaining your position.

This anti-avoidance rule requires that crypto sold and repurchased on the same day be matched together for cost basis purposes, effectively eliminating any loss claim from the transaction. The same day rule works differently from the more well-known bed-and-breakfast rule. With same-day matching, if you sell 1 Bitcoin at £25,000 at 10 am and buy 1 Bitcoin at £24,000 at 3 pm the same day, HMRC matches these transactions together.

Your cost basis for the repurchase becomes £25,000 (the sale price), not £24,000 (the actual purchase price), eliminating the £1,000 loss you might have claimed. This rule matters most for active traders attempting tax-loss harvesting.

Someone selling depreciated crypto to offset gains must ensure they don't repurchase that same crypto on the same day, or their loss disappears for tax purposes.

The timing window is strict—it covers the entire calendar day from midnight to midnight UK time, regardless of when during the day transactions occur.

Sophisticated strategies work around the same-day rule:

If you want to maintain crypto exposure while harvesting losses, you could sell Bitcoin and immediately purchase Ethereum, as the rule only applies to repurchasing.

The same specific cryptocurrency. Alternatively, waiting until the next day allows loss claims while only exposing you to one day of price movement risk.

Bed and breakfasting extends the same-day rule principles across a longer time period.

HMRC's bed-and-breakfast rule prevents you from selling cryptocurrency to crystallise a loss, then repurchasing the same crypto within 30 days, as this would allow artificial loss creation while maintaining your investment position.

Under this rule, crypto sold and repurchased within 30 days gets matched together for cost basis calculation purposes, using the repurchase price as your cost basis rather than recognising the loss.

If you sell 1 Ethereum at a £500 loss and repurchase it 20 days later, HMRC treats the sale and repurchase as a wash, disallowing your £500 loss claim for tax purposes.

The 30-day window runs from the day after your sale.

Selling on March 1st means you must wait until April 1st (31 days later) before repurchasing to preserve your loss claim.

This waiting period creates price risk—the cryptocurrency might appreciate during those 30 days, forcing you to buy back at a higher price than you sold, or it might depreciate further, allowing you to purchase at an even better price.

Strategic approaches to bed-and-breakfast restrictions:

Option 1: Purchase similar but different cryptocurrencies during the 30-day windowOption 1: Purchase similar but different cryptocurrencies during the 30-day window Someone holding Bitcoin who wants to harvest losses could sell Bitcoin, wait 30 days, then repurchase Bitcoin while maintaining crypto exposure through Ethereum or other large-cap coins during the waiting period.

Option 2: Use spouse's account Married couples can use spousal transfers to navigate bed-and-breakfast rules, though this requires careful documentation and genuine transfers, not just paper arrangements.

Option 3: Accept the 30-day price riskOption 3: Accept the 30-day price risk For investors with high conviction in the asset, accepting 30 days of price risk might be worthwhile to secure the tax loss claim.

Not sure if your trading patterns trigger these rules? Not sure if your trading patterns trigger these rules? Complete our Crypto Tax Health Check to identify potential compliance issues.

.png)

QUICK ACTION: Calculate your 2026 CGT liability now with our free Tax Impact Calculator. Get an instant estimate based on your transaction volume and portfolio size.

Income Tax applies when you receive cryptocurrency as payment rather than purchasing it as an investment.

This distinction fundamentally changes your tax treatment, often resulting in higher effective rates than the capital gains tax.

HMRC views crypto received for services, as employment compensation, from mining, or as staking rewards, as taxable income at receipt, regardless of whether you convert it to pounds.

Mining and staking rewards represent the most common income tax scenarios for crypto holders.

When you stake Ethereum and receive rewards, HMRC considers those rewards taxable income on the date you receive them, valued at their pound sterling equivalent at that moment.

This creates an immediate tax liability even if you don't sell the rewards.

Many stakers discover unexpected tax bills when they've accumulated rewards worth thousands but haven't realised those gains in cash. The pounds needed to pay tax on £5,000 of staking income must come from somewhere, even if those tokens remain staked.

Understanding whether cryptocurrency constitutes income or capital gains fundamentally changes your tax position.

Income Tax rates range from 20-45% with no exemption threshold, while Capital Gains Tax offers lower rates (10-20%) plus a £3,000 annual allowance.

Getting this categorisation wrong can cost you thousands in unnecessary tax or create compliance issues with HMRC.

The distinction centres on how you acquired the cryptocurrency.

Income arises when you receive crypto as payment for goods or services, as employment compensation, through mining operations, from staking rewards, as lending interest, from yield farming, or as protocol incentives.

Capital gains arise when you dispose of crypto you previously purchased or received, whether through sales, swaps, or using it for purchases.

Consider identical scenarios with different tax treatment:

Person A purchases £10,000 of Ethereum and sells it a year later for £15,000. They pay Capital Gains Tax on the £5,000 gain, paying £400 after their £3,000 exemption (assuming 20% rate).

Person B receives £10,000 of Ethereum as staking rewards and sells it immediately for £10,000. They pay Income Tax on the full £10,000 at their marginal rate— potentially £4,500 at 45%—despite making identical £10,000 in the same cryptocurrency.

The double taxation scenario confuses many crypto holders.

Staking rewards create income tax obligations at receipt, establishing a cost basis equal to that taxable value.

Later selling those rewards creates capital gains or losses based on price changes since receipt.

Someone receiving £3,000 in staking rewards taxed as income who later sells them for £4,000 pays Income Tax on £3,000 and Capital Gains Tax on £1,000. The £4,000 total isn't double-taxed, but it does face two different tax calculations at two different times.

Professional guidance proves particularly valuable for income versus capital categorisation. We've seen DIY investors incorrectly report £20,000 of staking rewards as capital gains, owing HMRC an additional £4,000 plus penalties when reviewed.

Proper categorisation from the outset prevents these costly mistakes while ensuring you're not overpaying through incorrect self-assessment.

Unsure if your crypto activities create income? Take our Tax Complexity Score to understand whether professional guidance would benefit your situation.

The income value you report establishes your cost basis for subsequent Capital Gains Tax calculation.

If you receive £3,000 of staking rewards in June and later sell them for £4,000, you've paid Income Tax on the £3,000 at receipt and Capital Gains Tax on the £1,000 appreciation at sale.

This layered taxation catches many crypto holders by surprise, particularly those actively staking multiple tokens throughout the year.

Crypto received as employment income faces similar treatment with additional complications:

Advanced income scenarios include lending interest, yield farming returns, and protocol incentives.

DeFi lending that generates interest creates taxable income as you accrue it, not when you withdraw. Liquidity provision rewards from protocols like Uniswap constitute income at receipt.

Governance token distributions may qualify as income or capital depending on circumstances.

We've seen retail investors face £8,000-£15,000 unexpected tax bills from DeFi income they thought was just "free crypto" rather than taxable earnings.

The Income Tax rates you face depend on your total income including all sources, not just crypto:

This can create situations where staking rewards generate 45% immediate tax liability despite being illiquid assets you can't immediately convert to pay that tax.

Professional guidance helps structure DeFi activities to manage these cash flow challenges while maintaining compliance.

.png)

HMRC applies Income Tax to crypto trading profits in rare cases where your activity constitutes a financial trade rather than investment.

This categorisation dramatically changes your tax treatment, typically resulting in higher effective rates but also allowing business expense deductions unavailable to investors.

Understanding whether you're a trader or investor represents one of the most consequential tax questions facing active crypto holders. The distinction between investing and trading doesn't depend on volume alone.

HMRC examines multiple factors:

A software developer trading crypto daily using technical analysis and leverage likely qualifies as trading. A retail worker making monthly Bitcoin purchases remains an investor even with fifty annual transactions. The assessment considers your overall pattern of behaviour rather than arbitrary transaction counts. If HMRC determines you're trading, all profits become subject to Income Tax rather than Capital Gains Tax.

This eliminates your £3,000 CGT allowance and applies rates from 20-45% instead of 10-20%.

However, trading status allows deducting platform subscriptions, research costs, trading course fees, and home office expenses that investors cannot claim. For high-volume traders with substantial expenses, trading status may actually reduce tax despite higher rates. The trading determination carries significant long-term implications.

Once classified as a trader, you'll struggle to revert to investor status later. HMRC expects consistency across years unless your circumstances fundamentally change.

This creates strategic considerations: accepting trading status early may prevent future arguments about when your activity crossed the threshold, but it also locks you into potentially higher tax rates permanently. Business entity structure becomes relevant for substantial trading operations.

Operating as a sole trader subjects all profits to Income Tax and National Insurance, potentially reaching 47% effective rates.

Incorporating as a limited company introduces Corporation Tax at 19-25% with additional flexibility around dividend timing and expense recognition.

For traders generating £50,000+ annual profits, corporate structures often deliver significant tax savings despite added compliance complexity. Our CryptoBiz Complete service specifically addresses these structural decisions.

Concerned about trading classification? Concerned about trading classification? Complete our Crypto Tax Health Check to identify red flags HMRC might notice.

.png)

PROFESSIONAL REVIEW:PROFESSIONAL REVIEW: If HMRC might classify your activity as trading, don't risk it alone. Book a free 15-minute consultation to discuss your specific circumstances with our specialists.

Beyond standard investment, income, and trading scenarios, several special situations create unique tax treatment requiring careful attention.

These edge cases often generate the most confusion and penalties because crypto holders either don't realise special rules apply or misunderstand their implications.

Understanding these situations prevents costly mistakes while identifying legitimate planning opportunities.

Gifting cryptocurrency to family members seems straightforward but creates multiple tax implications.When you gift crypto, HMRC treats it as a disposal at market value, potentially triggering Capital Gains Tax even though you received no proceeds. If the gift value exceeds £3,000, you may face CGT on gains above that threshold despite having no cash to pay the tax.

The recipient receives the crypto at the market value on the gift date as their cost basis, creating potential double taxation if values have risen substantially.

Spousal transfers represent the major exception: Gifts between married couples or civil partners carry no immediate tax implications, with the recipient inheriting thegiver's original cost basis.

Inheritance and death bring specific crypto complications:

International complications emerge when UK tax residents trade on foreign exchanges, hold crypto with overseas custodians, or receive income from foreign sources.

Your worldwide crypto gains and income remain taxable in the UK regardless of where exchanges or protocols are located.

Foreign exchange conversions add complexity when converting crypto through US dollars or other currencies before reaching pounds.

Double taxation treaties may provide relief if foreign jurisdictions also tax your crypto activity, but navigating these provisions requires specialist knowledge.

Lost or stolen cryptocurrency creates particularly painful tax situations:

Crypto purchased with inherited funds or received in divorce settlements faces special basis calculations:

Complex portfolio? Our Tax Complexity Score helps determine if your situation requires specialist professional guidance.

.png)

Understanding UK crypto tax theory matters little if common mistakes still trigger penalties.

These five errors represent 80% of problems we identify when reviewing new client portfolios.

Each mistake costs UK crypto holders between £800-£5,000 annually in unnecessary tax or penalties.

The most prevalent misunderstanding treats crypto-to-crypto exchanges as non-taxable.

Trading Bitcoin for Ethereum, Ethereum for Cardano, or any token for any other token constitutes a disposal event triggering Capital Gains Tax calculation.

Many investors assume only crypto-to-pounds conversions matter. This misconception leaves entire transaction histories unreported.

HMRC explicitly states that exchanging crypto assets for different crypto assets creates tax obligations identical to selling for pounds.

The pound sterling value of both cryptocurrencies at the swap moment determines your gain or loss.

If you acquired 1 Bitcoin at £25,000 and later swapped it for 15 Ethereum when Bitcoin was worth £35,000, you've realised a £10,000 gain requiring reporting regardless of never touching pounds.

This mistake compounds dramatically for active traders.

Someone executing 200 crypto-to-crypto swaps annually while only reporting their three fiat withdrawals faces severe non-compliance risk.

HMRC can access exchange records through regulatory frameworks, and the gap between actual activity and reported transactions creates obvious audit triggers.

Many crypto holders trade actively throughout the year without maintaining comprehensive records, assuming they'll "figure it out at tax time."

By January, they've lost access to exchange accounts, deleted trading apps, or simply forgotten passwords to platforms used months earlier.

Reconstructing complete transaction histories proves impossible without proper record keeping.

HMRC requires you to maintain records supporting your tax calculations for at least five years.

"I don't remember what I bought or when" doesn't constitute an acceptable tax position.

Lost records force you into conservative assumptions that typically result in substantially higher reported gains than actual economic reality.

Without proof of your cost basis, HMRC may assume zero acquisition cost, making your entire disposal proceeds taxable.

We recommend monthly export procedures:

On the first of every month:

This simple habit prevents the panic of attempting December reconstruction of January's forgotten trades.

Many platforms only provide 3-6 months of historical data, making delayed downloads permanently irretrievable.

Some investors mentally establish thresholds like "I don't need to track anything under £100" or "small transactions don't matter."

HMRC provides no de minimis exemption for cryptocurrency transactions.

Every disposal, regardless of size, technically requires gain or loss calculation contributing to your annual position.

A hundred £50 transactions creates £5,000 of activity requiring documentation.

This mistake particularly affects people using cryptocurrency for actual purchases:

The annual £3,000 exemption helps here, but only if you've actually calculated all your gains properly.

You can't claim "small transactions fall under the exemption" without first determining your actual total gains.

Many investors discover their supposedly insignificant transactions aggregate to £8,000-£15,000 of gains once properly calculated.

Staking and lending arrangements create immediate income tax obligations that many crypto holders misunderstand as "tax-free until I sell."

When you stake Ethereum and receive rewards, HMRC treats those rewards as taxable income on the day you receive them, valued in pound sterling at that moment. You owe income tax on that value now, not later when you eventually sell.

This timing distinction catches people by surprise. Accumulating £6,000 of staking rewards throughout the year creates a £2,400-£2,700 income tax bill (assuming 40-45% rate) even if you've never sold any rewards.

The tax money must come from somewhere else in your finances since the crypto remains staked.

Many investors don't realise they've created tax obligations until receiving surprising self-assessment calculations.

Compound the confusion with subsequent capital gains treatment

We regularly review situations where investors have calculated accurate transaction totals but applied wrong tax rates.

Treating income as capital gains, or inversely treating capital gains as income, creates substantial miscalculations.

Someone reporting £20,000 of staking rewards as capital gains at 20% rather than income at 40% owes HMRC an additional £4,000 plus penalties.

The categorisation matters enormously:

Understanding which activities generate income versus capital gains prevents this mistake:

Income: Every staking reward, every mining payment, every interest receipt from lending.

Capital Gains: Every sale of held cryptocurrency, every crypto-to-crypto swap.

Getting this distinction right matters more than sophisticated optimisation strategies.

Want to verify you're avoiding these mistakes? Complete our Crypto Tax Health Check for a free assessment identifying potential issues in your current approach.

Reporting cryptocurrency to HMRC requires systematic documentation and accurate Self Assessment completion.

Many first-time filers feel overwhelmed by the process, but breaking it into clear steps transforms complexity into manageable tasks. This section provides the exact process ACCA-registered specialists use when preparing crypto tax returns.

Step 1: Gather Complete Transaction History

Begin by collecting comprehensive records from every platform you've used:

The key is completenessmissing even 10% of transactions creates compliance risk and potential underpayment.

Use blockchain explorers for wallet addresses to verify all on-chain activity.

Cross-reference exchange exports with blockchain data to identify any discrepancies.

Many investors discover they forgot about small exchanges used briefly or DeFi positions they established months ago.

Step 2: Categorise Every Transaction

Review each transaction and categorise it correctly:

Accurate categorisation determines whether you're calculating capital gains, recognising income, or simply documenting cost basis.

Crypto-to-crypto swaps require particular attention—they're disposals of the sold crypto (triggering CGT) and purchases of the received crypto (establishing new cost basis).

Someone swapping 1 Bitcoin for 20 Ethereum must calculate their Bitcoin disposal gain or loss using current pound values, then record £X acquisition cost for their new Ethereum position.

Step 3: Calculate Capital Gains Using Share Pooling

Apply HMRC's share pooling methodology to calculate capital gains:

Same-day and bed-and-breakfast matching rules apply first:

Step 4: Value and Report Income

Calculate the pound sterling value of all crypto income at the moment you received it:

All require valuation using reputable market prices from the specific date and time of receipt.

This valuation establishes both your income tax liability and your cost basis for future disposal calculations.

Use CoinMarketCap, CoinGecko, or exchange API data for historical prices.

Screenshot or save evidence of the prices you used in case HMRC questions your valuations.

For tokens without clear market prices, document your valuation methodology thoroughly—HMRC expects reasonable approximations supported by available data.

Step 5: Complete Self Assessment Tax Return

Access HMRC's Self Assessment online system and navigate to the Capital Gains section:

For crypto income, report it in the appropriate employment, self-employment, or other income sections depending on how you received it:

Staking rewards typically appear under "other income" unless you're mining professionally (self-employment) Employment crypto bonuses go in employment income sections

Step 6: Maintain Supporting Documentation

Keep comprehensive records supporting every number on your tax return:

Maintain these for at least five years.

HMRC can review your returns for up to 20 years in cases of suspected tax evasion, though normal reviews cover 4-6 years.

Organise records by tax year with clear file naming.

Future years' calculations will reference previous years' cost basis pools, making organised record keeping essential for ongoing compliance. Software outputs from platforms like Koinly should be supplemented with raw transaction data and manual verification notes.

Step 7: Submit Before January 31st Deadline

Submit your completed Self Assessment by January 31st following the end of the tax year.

The 2025/26 tax year (April 6, 2025 to April 5, 2026) requires submission by January 31, 2027

Late submission triggers automatic £100 penalties plus additional charges for extended delays.Pay any tax owed by the same January 31st deadline.HMRC charges interest on late payment plus potential penalties exceeding 100% of tax owed for serious delays.

Setting up a payment plan before the deadline can avoid some penalty charges if you can't pay the full amount immediately.

Our CryptoTax Navigator service completes this entire process for clients, ensuring accurate calculations, optimal tax positions, and complete HMRC compliance.

HMRC requires comprehensive documentation supporting your cryptocurrency tax calculations.

Proper record keeping transforms compliance from a stressful annual scramble into a manageable routine.These practices protect you during HMRC reviews while reducing your annual tax preparation burden.

HMRC's cryptocurrency guidance explicitly lists required documentation. You must retain records showing:

Practically, this means maintaining transaction-level detail across your complete crypto history. Every purchase, sale, swap, transfer, staking reward, and fee must have verifiable documentation:

These collectively prove your tax position's accuracy.

Missing documentation for even 10-15% of your transactions creates material compliance risk. The five-year retention requirement means you're building a permanent archive.

Documents from the 2025/26 tax year remain required until January 2032.Cloud storage with reliable backup systems protects against data loss. Many crypto holders use encrypted folders in Google Drive, Dropbox, or similar services without omated backup scheduling.

Different cryptocurrency platforms provide varying quality of transaction records:

We recommend monthly exports even from platforms you use infrequently:

Monthly export procedure:

For DeFi activities, blockchain explorers like Etherscan provide complete transaction histories:

Every disposal requires pound sterling valuation at transaction time.

"I sold Ethereum when it was around £2,000" doesn't meet HMRC standards. You need specific prices from reasonable sources at exact transaction times:

Major cryptocurrencies have well-established market prices from reputable exchanges Smaller tokens require more careful documentation.

CoinMarketCap and CoinGecko provide historical price data with timestamp precision.

When you swapped tokens at 14:23 on March 15th, these platforms show exact prices at that moment from multiple exchanges. Screenshot or download these valuations when preparing your tax calculations.

HMRC accepts reasonable valuation methods but expects consistency and documentation. Tokens without liquid markets create valuation challenges.

How do you value an obscure DeFi token with three daily trades?

HMRC guidance suggests using reasonable approximations from available information, but lack of clear market prices doesn't exempt you from reporting obligations. Document your valuation methodology thoroughly in these situations.

Portfolio tracking software automates much of this record keeping burden:

HMRC doesn't mandate specific software or methods.

You can maintain records in spreadsheets if they're accurate and complete.

The critical standard is "can you prove your tax position if questioned?"

Whether that proof comes from sophisticated software or meticulous manual records doesn't matter to HMRC.

What matters is comprehensive, verifiable documentation supporting every number on your tax return.

Professional review adds substantial compliance confidence even with good records.

Software classifies DeFi transactions using automated rules that don't always match HMRC's specific interpretations.

A specialist reviewing your software output identifies misclassifications, ensures proper treatment of edge cases, and provides documentation meeting professional standards.

Most of our clients using software submit it to us for verification rather than directly to HMRC.

Need help establishing proper record keeping systems? Need help establishing proper record keeping systems? Book a free consultation to discuss documentation requirements for your specific crypto activities.

.png)

Understanding UK crypto tax rules transforms from a compliance burden into a strategic advantage when you grasp the full picture.The features, advantages, and benefits framework helps clarify why investing effort in tax knowledge delivers returns far exceeding the work required.

UK crypto tax rules provide clear frameworks despite their reputation for complexity:

These features represent the mechanical reality of what HMRC requires, and they're more accessible than most investors realise.

The rules include specific calculation methods that provide certainty once understood:

This structure means you can learn the rules and apply them consistently, even as your crypto activities evolve.

Proper compliance delivers immediate advantages beyond simply avoiding penalties:

Compliance also provides psychological advantages that active crypto holders often undervalue.Confidence that your tax affairs are in order eliminates the anxiety that undermines investment decision-making.

When you know your current tax position, you can sell appreciating assets without fear of unknown tax consequences.You can explore new DeFi opportunities understanding their tax implications upfront.

You can sleep soundly during HMRC enforcement campaigns knowing your reporting is accurate and comprehensive.

This peace of mind enables better investing by removing tax-driven emotional decision-making.

The audit-protection advantage grows more valuable as HMRC's crypto enforcement capabilities expand:

We've seen compliant clients resolve HMRC questions in days with minimal stress, while those with poor records face months of reconstruction work and substantial penalties.

The ultimate benefits of understanding UK crypto tax extend well beyond compliance.

Strategic tax planning enables optimising your investment returns:

These techniques can improve after-tax returns by 15-25% for active investors compared to ignoring tax optimisation entirely.

Proper understanding enables scaling your crypto activities confidently:

You can increase investment size knowing how gains will be taxed

You can diversify into DeFi understanding income implications

You can potentially transition to trading status strategically if your activity justifies it

This scalability proves impossible when tax uncertainty constrains your activities to situations you're comfortable reporting.

Long-term wealth preservation represents the ultimate benefit.

Crypto investors who optimise tax from day one compound their wealth significantly faster than those who ignore tax until problems emerge.

The difference between 10% and 20% CGT rates on a £100,000 gain equals £10,000 retained in your portfolio.Multiply this across years of investing, and strategic tax awareness delivers tens of thousands in additional wealth accumulation.

.png)

Taking action depends on your current position and crypto activities.

Different situations call for different approaches, but every UK crypto holder should take some action to ensure compliance and optimise their tax position.

For Simple Buy-and-Hold Investors

If you hold Bitcoin and Ethereum on a single exchange with minimal transactions, your path to compliance is straightforward:

Immediate action:

If your total gains remain below £3,000, you may have no immediate tax obligations but should still maintain accurate records for future years.

Set up a simple tracking system for future transactions, even if it's just a spreadsheet noting purchase dates, amounts, and prices.

Review your position annually before the tax year ends on April 5th to identify any beneficial timing opportunities.

Consider whether strategic disposals to use your annual CGT allowance make sense before it expires.

If you trade across multiple exchanges, participate in DeFi protocols, or receive staking rewards, professional assistance almost certainly delivers value exceeding its cost.

The complexity of tracking hundreds or thousands of transactions, determining correct valuations for exotic tokens, and categorising complex DeFi interactions exceeds what reasonable DIY efforts can accomplish reliably.

Begin by consolidating all your transaction histories from every platform you've used:

If you accept crypto business payments, mine professionally, or hold portfolios exceeding £500,000, specialist professional guidance isn't optional—it's essential risk management.

The tax optimisation opportunities and compliance complexities at this level require expertise specifically focused on cryptocurrency taxation combined with broader business and wealth planning knowledge.

Schedule comprehensive tax planning consultations before taking major actions:

Your crypto tax position should integrate with your overall financial planning, estate considerations, and business structure decisions.

The costs of getting these questions wrong dramatically exceed professional fees to get them right proactively.

.png)

All our work is delivered by qualified ACCA-registered specialists—we are not an automated software platform.

HashTax provides specialised cryptocurrency accounting services designed specifically for UK investors and traders.

Unlike generic accountants adding crypto as an aftethought, our entire practice focuses on cryptocurrency taxation, giving us deep expertise in the nuances that determine whether you pay the right amount or substantially overpay.

Our CryptoTax Navigator service provides retail investors with comprehensive tax compliance support at predictable pricing.

We analyse your complete transaction history across all exchanges, calculate your accurate capital gains and income, and prepare HMRC-ready tax reports.

The service includes unlimited transaction processing, meaning you pay one flat fee regardless of whether you have 50 or 5,000 transactions.

Beyond calculations, CryptoTax Navigator provides year-round support answering your crypto tax questions as they arise.

You're not left alone between tax seasons wondering whether new activities create tax obligations. Our educational approach helps you understand your tax position rather than creating dependency on our service.

TraderTax pro serves active traders managing complex multi-exchange portfolios and DeFi activities.

We integrate with 30+ exchanges and protocols to capture complete transaction histories automatically.

Our specialists categorise complex DeFi transactions like liquidity provision, yield farming, and protocol incentives accurately according to HMRC guidance.

The service includes proactive tax-loss harvesting alerts, real-time tax impact analysis, and strategic guidance on timing transactions optimally.

TraderTax Pro clients typically trade 200-2,000 times annually across multiple platforms.

DIY approaches for this volume prove unreliable and enormously time-consuming.

Our professional reconciliation identifies discrepancies between exchanges, ensures no transactions go unreported, and optimises cost basis calculations using share pooling rules.

CryptoBiz Complete addresses businesses accepting crypto payments, operating mining operations, or structuring crypto activities as companies.

We provide specialised accounting that bridges traditional business bookkeeping with cryptocurrency transaction complexities.

The service includes VAT compliance frameworks for crypto transactions, Corporation Tax optimisation strategies, and integration with your existing accountancy systems.

Business clients benefit from ongoing strategic advisory on structure optimisation, expense categorisation, and regulatory compliance.

We help determine optimal entity structures comparing sole trader versus limited company taxation.

Our specialists assist with HMRC registration requirements specific to crypto businesses and provide representation if questions arise.

CryptoWealth Advisor serves sophisticated investors with substantial crypto holdings requiring comprehensive wealth planning.

We provide multi-jurisdiction tax optimisation for clients with international tax exposure, estate planning incorporating crypto assets, and personalised quarterly strategic sessions.

The service includes priority access to senior specialists and concierge support for time-sensitive questions.

High-net-worth clients face unique challenges around privacy, estate planning, and cross-border taxation.

Our specialists coordinate with your solicitors, traditional wealth advisers, and international tax counsel to ensure comprehensive planning.

We assist with trust structures, inheritance planning, and offshore considerations while maintaining full UK compliance.

Book your free 15-minute consultation today — Schedule now

Understanding UK crypto tax represents your first step toward compliance and optimisation.

Taking action transforms knowledge into real outcomes—accurate reporting, optimised tax positions, and confidence in your crypto investing.

Free Compliance Assessment

HashTax offers free 15-minute consultations to assess your specific situation and recommend the optimal path forward.

During your consultation, we review your transaction volume, crypto activities, and tax concerns to provide personalised guidance.

You'll leave with clarity about your obligations, understanding of potential risks, and recommendations for addressing them efficiently.

There's no obligation to proceed with our services—the consultation provides value regardless of whether you engage us professionally.

Book your free 15-minute consultation

Path 1: Immediate Action

If you're facing an urgent deadline, have received HMRC correspondence, or need immediate compliance, book an urgent consultation and we'll prioritise your case.

Path 2: Scheduled Planning

If you're planning ahead for the next tax year or want strategic optimisation, schedule a standard consultation at a time that suits you.

Path 3: Self-Assessment Support

If you prefer to handle filing yourself but want professional verification, start with our Crypto Tax Health Check to identify any gaps in your current approach.

HMRC penalties and interest accumulate from the moment you miss a deadline or file incorrectly.

The longer you wait to address crypto tax compliance, the more complex and costly resolution becomes.

Perhaps more importantly, the psychological burden of unresolved tax obligations undermines your investment decision-making and quality of life.

Addressing it properly brings immediate relief and long-term confidence.

Book your free crypto tax consultation today at hashtax.io/consultation or email hello@hashtax.io to schedule a confidential discussion with one of our ACCA- registered crypto tax specialists.

Whether you're a first-time filer nervous about reporting or an experienced trader seeking optimisation, we'll provide the expertise you need to handle UK crypto taxation with confidence.

Your crypto tax compliance matters. Let's address it properly together. Your crypto tax compliance matters. Let's address it properly together.

Disclaimer: This article provides general guidance on UK cryptocurrency taxation for the 2025/26 tax year. Individual circumstances vary significantly, and you should seek professional advice for your specific situation. Tax rules change regularly, and this guidance reflects our understanding of current HMRC positions. HashTax provides professional cryptocurrency accounting services and strategic tax guidance, not automated software solutions.

About HashTax: We're the UK's leading cryptocurrency accounting specialists, providing professional tax services exclusively for crypto investors, traders, and businesses. Our expertise helps you achieve complete HMRC compliance while optimising your tax position through strategic guidance you can understand and trust.

HashTax Specialists

Our team of ACCA-qualified accountants specializing in UK cryptocurrency taxation. We provide expert guidance on HMRC compliance, tax planning, and professional advisory services for crypto investors and businesses.

.svg)

.svg)