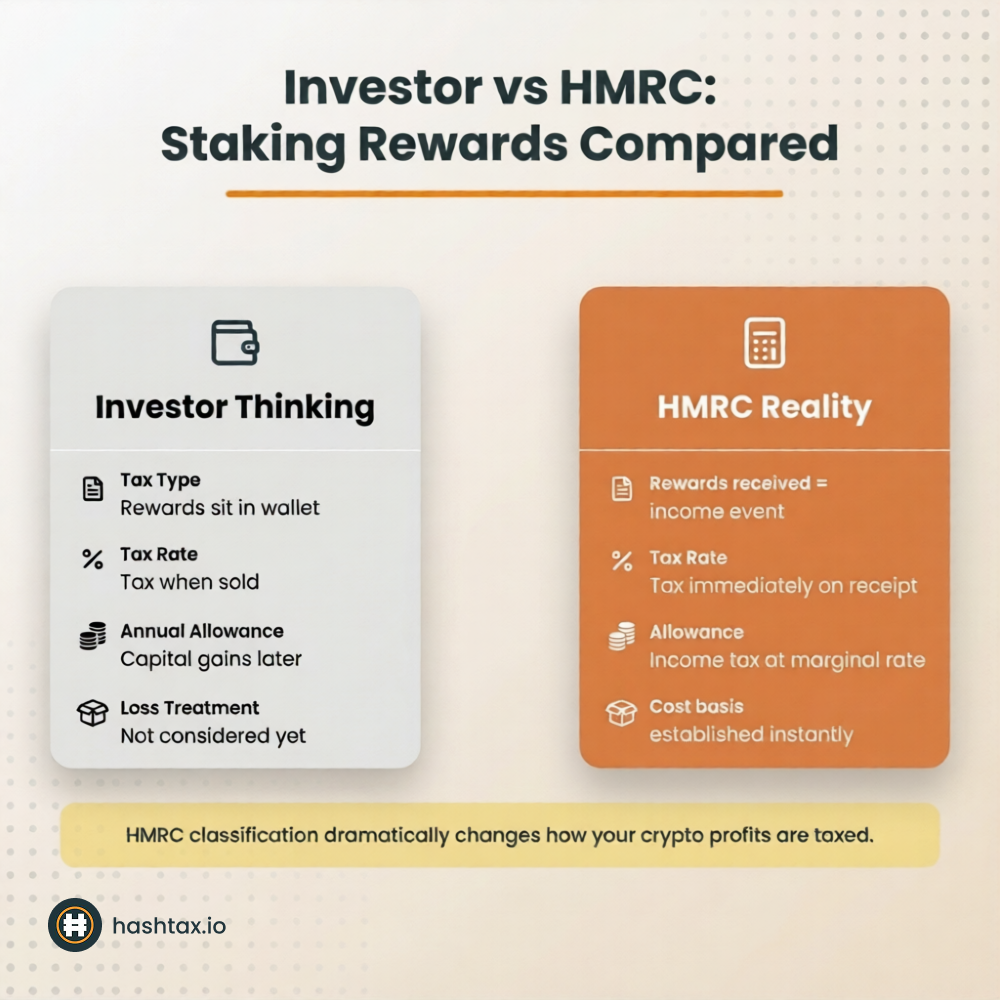

Staking feels like watching an investment grow. You commit your crypto, rewards accumulate, and your balance increases. Nothing about that experience resembles receiving income.

HMRC does not share that intuition.

In HMRC's view, staking rewards are income — taxable at the moment you receive them, at their sterling value on the date of receipt. It does not matter whether you sell them, reinvest them, or leave them untouched for years. The tax obligation arises at the point of receipt.

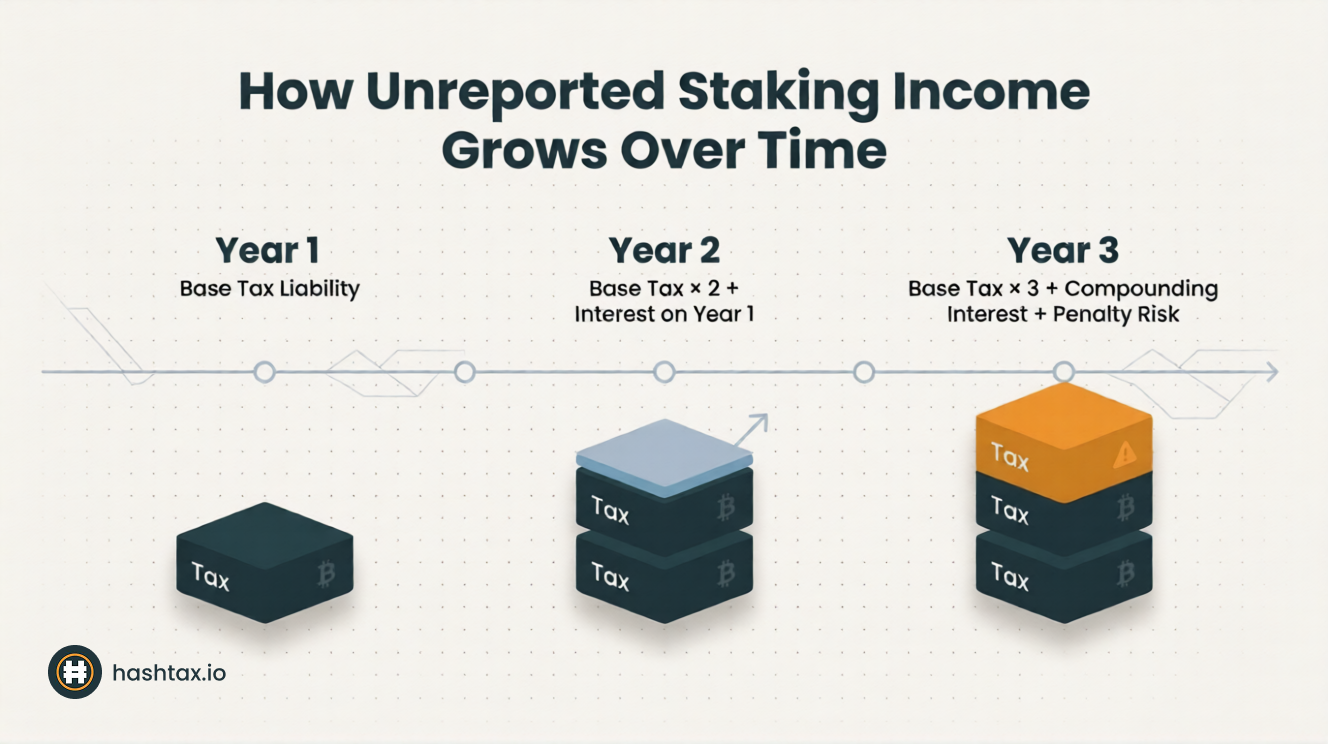

This single rule — and the frequency with which it is misunderstood — drives most of the compliance problems HashTax sees from stakers. An investor who has been staking for two years and never reported their rewards has likely accumulated Income Tax liability across multiple tax years. By the time that comes to light, interest is accruing and penalties may apply.

This guide works through the three mistakes that follow from this misunderstanding, what they cost, and how to correct them.

The most common staking tax mistake is treating rewards as capital appreciation rather than income. The logic feels sound: buy-and-hold investors pay no tax on unrealised gains, so rewards sitting in a wallet surely follow the same rule.

They do not. Capital gains tax applies to disposals of assets you already own. Staking rewards are new assets you have received. HMRC's published guidance treats them as miscellaneous income in the tax year of receipt — the same year-of-receipt principle that applies to employment income, rental income, or any other form of earnings.

When your validator or staking protocol distributes 0.05 ETH as a reward, you have received property with a sterling value. That value is your taxable income. It is reportable through Self Assessment for the tax year in which it arrived — whether or not you have ever sold a single token.

Many staking protocols automatically reinvest rewards. Your balance grows seamlessly. No withdrawal occurs. Nothing feels like income.

But each automatic reinvestment is a receipt event followed immediately by a reinvestment decision. HMRC treats the receipt as taxable regardless of what happens to the tokens afterwards. Auto-compounding does not defer or eliminate the income tax obligation — it creates a continuous series of taxable events that many investors never capture.

An investor who has staked consistently across two or three tax years without reporting rewards faces:

The longer the staking activity has continued unreported, the wider this exposure becomes. Voluntary disclosure — covered later in this guide — is the appropriate response. But the earlier it is addressed, the lower the total cost.

Stakers who do understand that rewards are taxable as income often assume that settles the matter. Report the income, pay the tax, done.

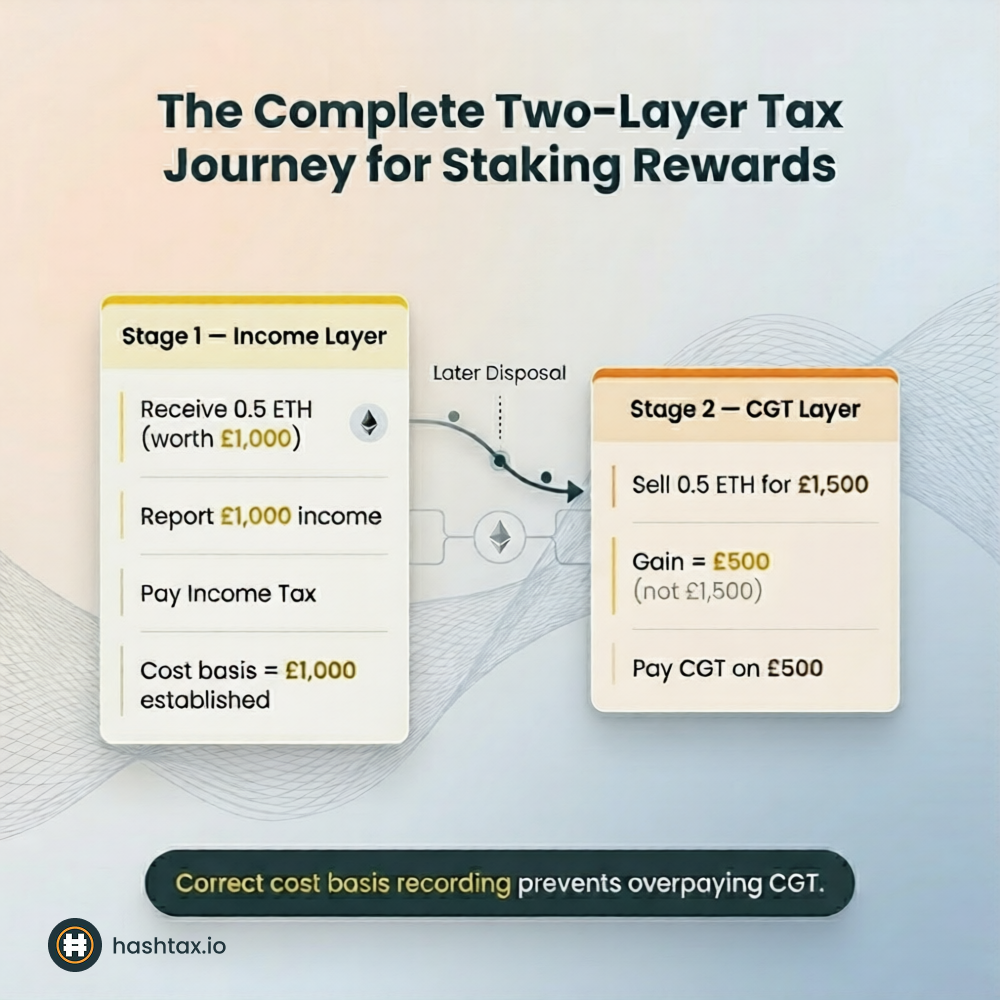

There is a second layer. When you eventually dispose of your staking rewards — by selling, exchanging, or using them — a Capital Gains Tax event arises on any appreciation that has occurred since you received them.

The two layers work as follows:

These are separate tax events, calculated independently. The income tax event establishes your cost basis for the future capital gains calculation — the income value you reported is treated as the acquisition cost of the tokens. This prevents double taxation on the initial value, but it does not eliminate Capital Gains Tax on subsequent appreciation.

Suppose you receive 0.5 ETH as staking rewards when ETH is trading at £2,000 per coin. The sterling value of your reward is £1,000.

You report £1,000 as miscellaneous income on your Self Assessment return for that tax year. This establishes your cost basis for the 0.5 ETH at £1,000.

Eighteen months later, ETH trades at £3,000 per coin. You sell your 0.5 ETH for £1,500. Your capital gain is £500 (£1,500 proceeds minus £1,000 cost basis). Capital Gains Tax applies to that £500 gain after applying the annual exempt amount.

If you had not correctly recorded the income event, your cost basis would default to zero — making the entire £1,500 proceeds appear to be a taxable gain. This error — failing to link the income event to the cost basis — results in significant overpayment of Capital Gains Tax.

Both errors — missing the income event entirely, and failing to link it to a cost basis — are common. The first error creates an income tax liability. The second error creates a Capital Gains Tax overpayment. Neither is immediately obvious without a complete review of the transaction record.

Use the Crypto Tax Health Check to identify whether your staking records are complete enough to support both tax calculations correctly.

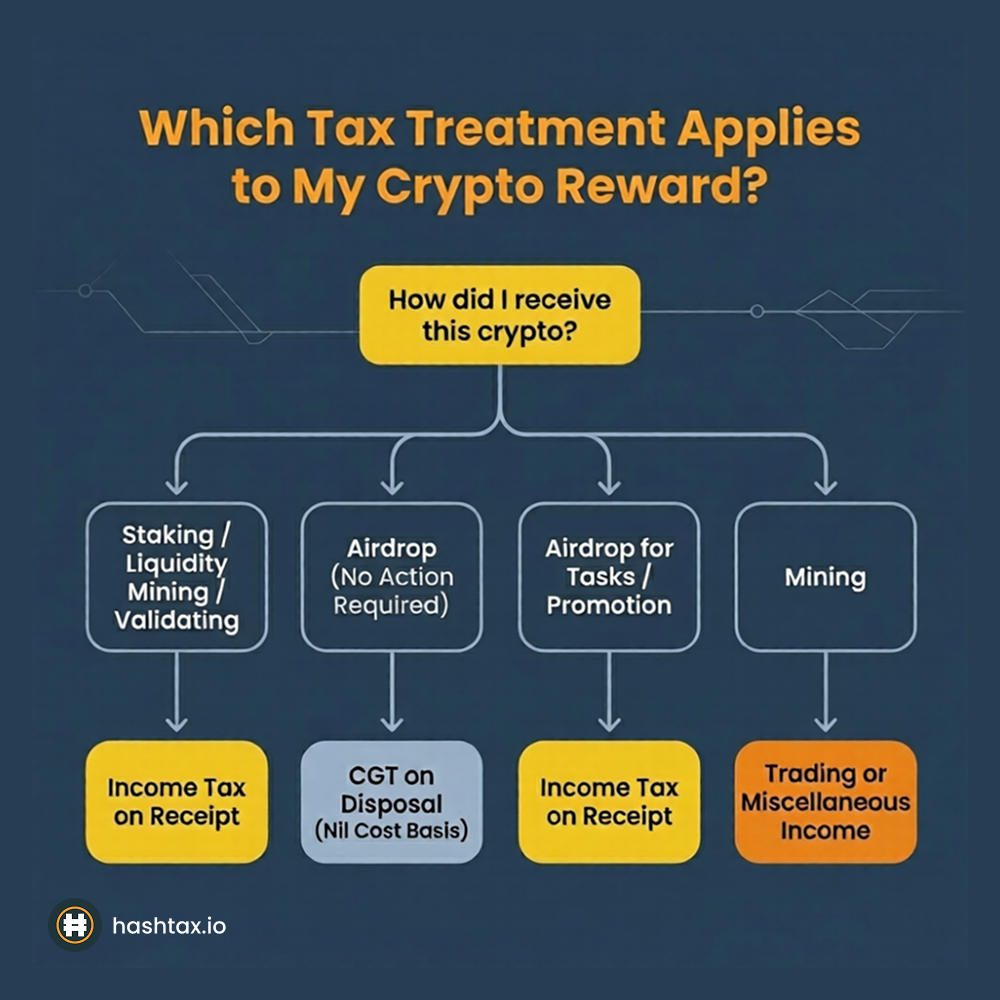

Not all crypto rewards are treated identically by HMRC. The tax treatment depends on the nature of the activity generating the reward. Applying staking rules to a different type of reward — or vice versa — produces incorrect tax calculations.

The main reward types UK investors encounter, and how HMRC approaches each:

The distinction between airdrops as income versus capital is particularly important. An airdrop received for simply holding a token — with no action required — is generally treated as a capital event. HMRC's position is that no income arises at receipt; instead, the cost basis of the airdropped tokens is nil, and Capital Gains Tax applies when you dispose of them.

An airdrop received in exchange for completing tasks, promoting a project, or providing services is treated differently — it is income, taxable at receipt.

Investors who receive multiple types of rewards from different protocols frequently apply a single treatment to all of them. Staking rules get applied to airdrops; airdrop rules get applied to liquidity mining rewards. Each misclassification affects the tax year in which liability arises, the rate at which it is taxed, and how cost basis is subsequently calculated.

If your portfolio includes a mix of staking rewards, airdrops, liquidity provision, and other reward types, each category needs to be assessed and recorded separately. Merging them into a single figure produces a figure that is unlikely to be correct for any of the categories involved.

A common assumption among stakers is that staking rewards are difficult for HMRC to trace — particularly for self-custody wallets that have never been connected to a named exchange.

This assumption is increasingly unreliable.

UK-regulated exchanges are required to share customer data with HMRC. This includes transaction histories showing deposits and withdrawals. Where an account shows staking platform withdrawals or token receipts consistent with reward distributions, HMRC can identify likely staking activity.

HMRC uses blockchain analytics tools capable of tracing wallet activity across the public ledger. Staking contracts have known addresses. Reward distributions to staker wallets are publicly visible on-chain. Connecting a wallet to a named individual requires only one link — often an exchange withdrawal or a KYC-verified deposit — from which activity across multiple wallets can be traced.

HMRC's Connect system cross-references exchange data against Self Assessment returns. Where staking activity is identified but no miscellaneous income is declared, the discrepancy flags for review. Enquiry letters follow.

None of this means every staker will be investigated. It means the risk of discovery is real, grows each year as HMRC's data resources expand, and is best addressed through voluntary compliance rather than the assumption of invisibility.

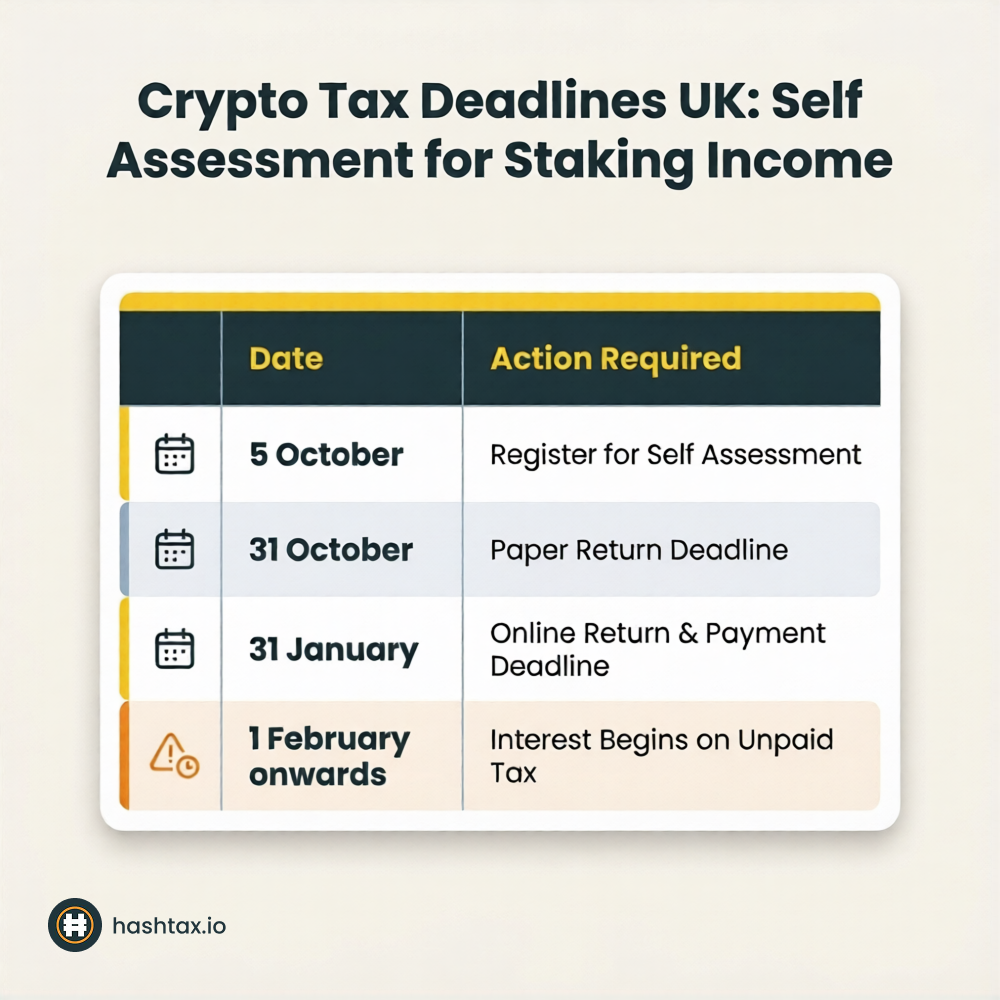

Staking income is reported through Self Assessment in the tax year it is received. The UK tax year runs from 6 April to 5 April. Income received at any point during that period is reportable in that year's return, due by 31 January following the end of the tax year.

Step 1: Register for Self Assessment if not already registered.

If your staking income exceeds £1,000 in any tax year and you are not already in Self Assessment, you must register. The registration deadline is 5 October following the end of the tax year in which the income arose.

Step 2: Calculate total staking income for the tax year.

Add up the sterling value of every reward received during the tax year. Each reward is valued at the market price of the token at the exact time of receipt. Day-end prices are not sufficient — transaction-time valuations are required.

Step 3: Record each reward's sterling value as your cost basis.

The income value you report becomes the acquisition cost of those tokens for future Capital Gains Tax purposes. Maintain a separate record linking each reward receipt to its income value. This prevents overpaying Capital Gains Tax when you later dispose of the tokens.

Step 4: Report income on the correct Self Assessment page.

Staking rewards are reported as miscellaneous income on the SA100 return. If your total miscellaneous income exceeds £2,500, you must complete the full additional income pages. Employed individuals who have not previously used Self Assessment will need to register and file a return specifically for this income.

Step 5: Report separately for each tax year.

Each tax year has its own allowances and filing obligation. Staking income from 2023/24 and 2024/25 cannot be combined — each year requires its own calculation and return. If you have multiple years of unreported income, each year must be addressed individually.

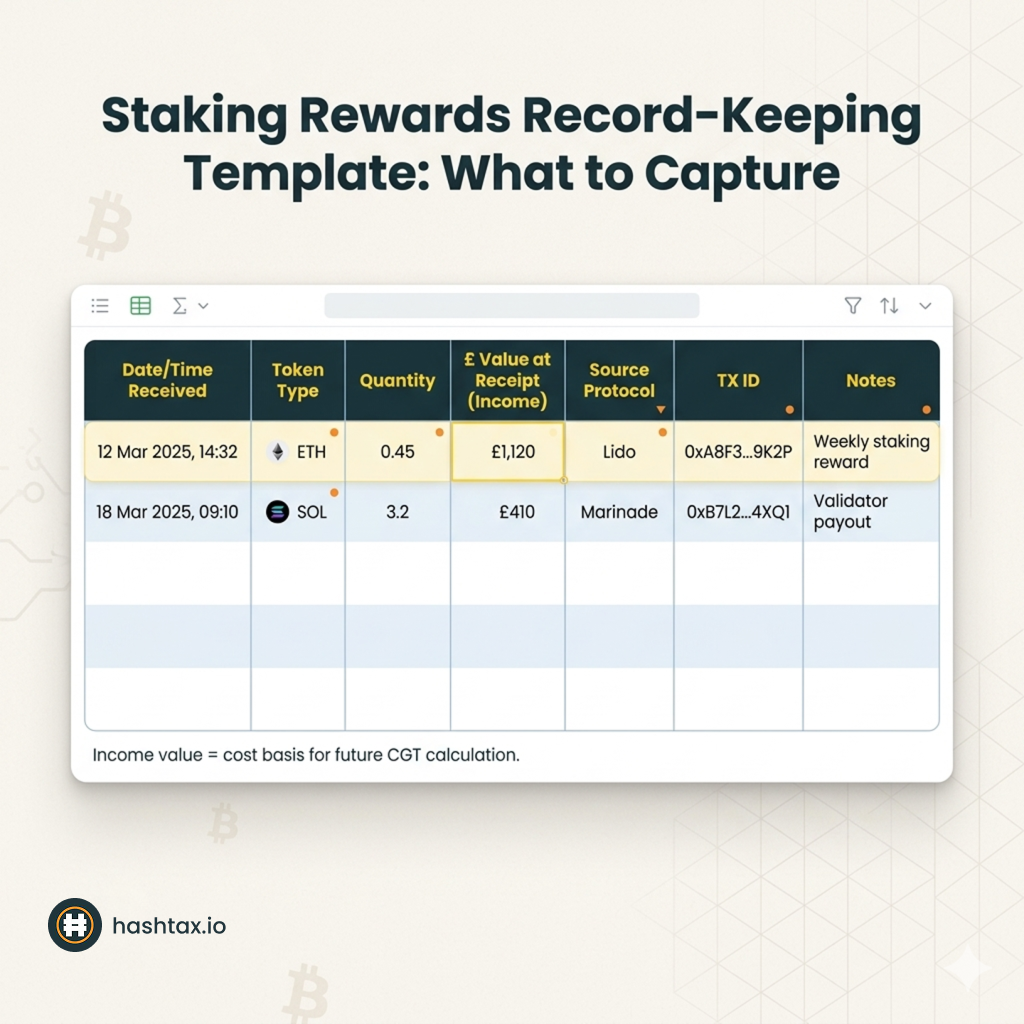

The documentation requirement for staking rewards is demanding because of the frequency of reward events. A staker receiving daily rewards across a full tax year may have over 300 individual income events to record — each requiring a transaction-time sterling valuation.

A compliant record for each reward receipt must include:

Transaction-time valuation is the requirement most frequently missed. HMRC expects valuations based on the market price of the token at the specific time of receipt — not the day's opening price or a daily average. Exchange price feeds and blockchain explorers with timestamp correlation are the standard method.

For investors receiving frequent rewards, a weekly documentation session prevents year-end reconstruction. Logging rewards as they arrive — rather than attempting to reconstruct 365 days of data in January — reduces both the risk of errors and the time required.

Cost basis records must be maintained as a separate, linked system. For every reward receipt, record the income value alongside the future disposal tracking. When you eventually sell the tokens, the disposal calculation depends on being able to identify the cost basis established at receipt. A single spreadsheet with columns for receipt date, quantity, income value, disposal date, disposal proceeds, and gain makes both calculations accessible in one place.

Staking tax compliance looks manageable until you are confronted with the full picture: hundreds of reward events, transaction-time valuations for each, two separate tax calculations per token batch, multiple reward types requiring different treatment, and the possibility of several years of unreported activity requiring voluntary disclosure.

Each stage involves precision. Transaction-time valuations must use reliable, defensible price sources. Cost basis linkage between income events and future disposals must be accurate. The correct Self Assessment pages must be used. Voluntary disclosures must cover all affected years and include correct interest calculations.

Errors at any stage produce incorrect filings. Incorrect filings create enquiry risk. Enquiries resolved after the fact carry higher costs — in both professional fees and penalties — than compliance achieved proactively.

HashTax provides expert human analysis across the full staking tax lifecycle. Our ACCA-registered specialists review your complete reward history, apply correct valuations, and prepare Self Assessment returns that are defensible if challenged. Where voluntary disclosure is needed, we prepare and submit through the appropriate HMRC channels. We are not an automated platform — every case is reviewed by a qualified professional.

Services are delivered by qualified human specialists. HashTax is not an automated platform or software solution.

Book a staking tax consultation with a HashTax specialist

A HashTax specialist will review your staking activity and identify whether you have an unreported liability. We will confirm which tax years are affected, clarify the reward types involved, and advise on the correct path to compliance.

The assessment carries no obligation to proceed. Addressing your position voluntarily, before HMRC contacts you, significantly limits your penalty exposure.

Book your free staking tax assessment

If you have unreported staking income from previous tax years:

Book an urgent consultation — voluntary disclosure through HMRC's Digital Disclosure Service resolves your position and limits penalties before enforcement begins.

If you are currently staking and want to confirm your records are correct:

Complete the Crypto Tax Health Check to identify gaps before your next Self Assessment filing deadline.

If you want to calculate your likely current year liability:

Use the Tax Impact Calculator to estimate your staking income tax position based on your rewards to date.

Interest accrues on unpaid Income Tax from 31 January following the tax year in which income arose. An unreported staking income liability from 2022/23 has been accumulating interest since February 2024. Each additional year of inaction adds a further layer.

Voluntary disclosure, made before HMRC opens an enquiry, attracts significantly lower penalties than disclosures made after contact. The distinction between unprompted and prompted disclosure is one of the most consequential factors in penalty calculation.

Staking is an increasingly visible activity for HMRC. Exchange data-sharing, blockchain analytics, and the expansion of HMRC's Connect system make unreported staking income progressively easier to identify. The calculation that favours voluntary disclosure today becomes less favourable the longer it is delayed.

Visit HashTax to learn more about our professional crypto tax services, or book a consultation to discuss your staking position with a specialist.

Your crypto tax compliance matters. Let's address it properly together.

HashTax Specialists

Our team of ACCA-qualified accountants specializing in UK cryptocurrency taxation. We provide expert guidance on HMRC compliance, tax planning, and professional advisory services for crypto investors and businesses.

.svg)

.svg)