Rachel thought she was doing everything right. She kept spreadsheets of her cryptocurrency purchases, noted the dates she bought Bitcoin and Ethereum, and saved screenshots from Coinbase showing her transactions.

When she received an HMRC compliance check letter eighteen months later, her confidence evaporated. The tax officer's questions revealed gaps she never knew existed: missing cost basis documentation for crypto-to-crypto swaps, no records of staking rewards received, incomplete transaction histories from a defunct exchange, and zero evidence of the sterling values she had used in her calculations.

The compliance check stretched across nine months of reconstructive work, professional fees, and penalties for "careless" errors. At HashTax, we see situations like Rachel's regularly — crypto holders who genuinely believe they are compliant discovering painful gaps only when HMRC scrutinises their reporting.

This guide identifies the specific requirements HMRC expects, shows where most holders fall short, and provides the roadmap for closing gaps before they become serious problems. Not sure where your own position stands? Our free Crypto Tax Health Check takes ten minutes and identifies your specific risk areas before you read another word.

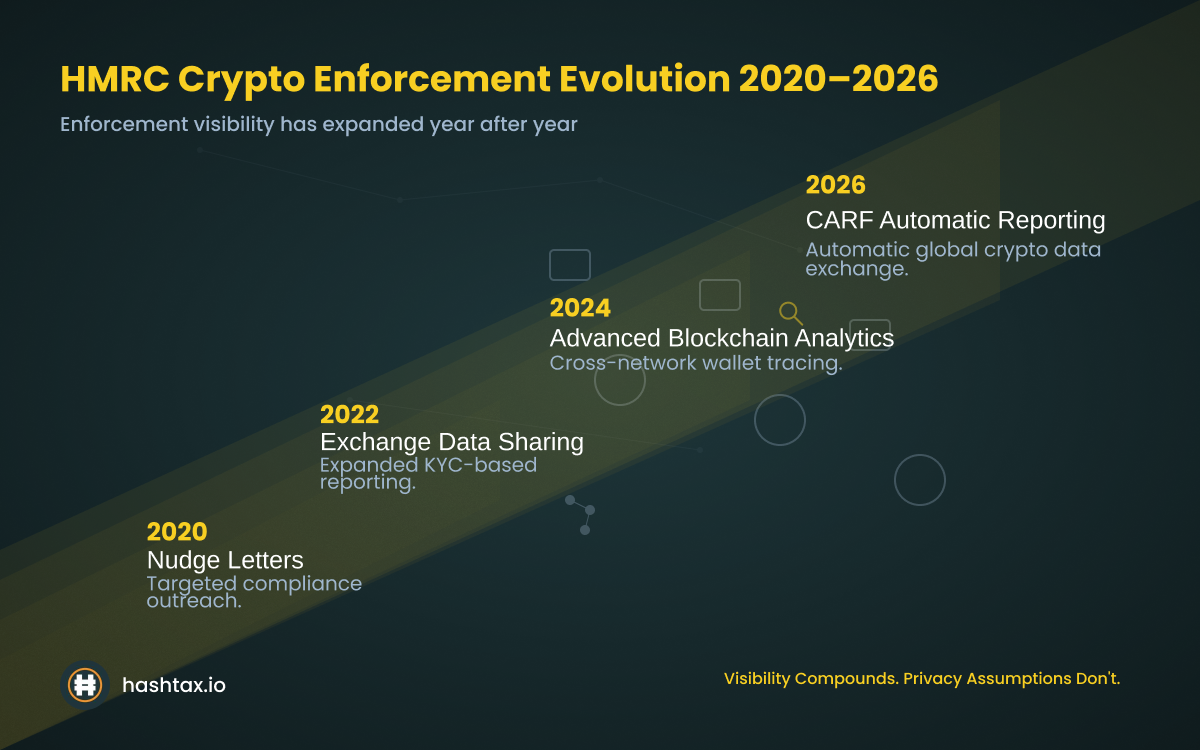

HMRC's approach to cryptocurrency compliance has transformed dramatically since 2022. What began as limited enforcement targeting obvious non-compliance has evolved into sophisticated, data-driven surveillance affecting all crypto holders.

The Cryptoasset Reporting Framework (CARF), now operational from January 2026, is HMRC's most significant enforcement enhancement to date. This international agreement requires cryptocurrency exchanges to automatically report customer transaction data to tax authorities across 48 countries including the UK. Every trade, every stake, every transfer — HMRC receives comprehensive data without needing to request it.

Penalty structures for crypto non-compliance now match HMRC's most serious enforcement categories:

These are not theoretical maximums. HMRC actively applies substantial penalties when gaps suggest deliberate avoidance rather than genuine misunderstanding.

Current enforcement initiatives include the "nudge letters" campaign — which has contacted over 30,000 crypto investors suspected of non-compliance since 2020 — alongside data sharing agreements with Coinbase, Kraken, eToro, and other major platforms.

One of the most common misconceptions among UK crypto holders is that their on-chain activity is invisible to HMRC. This is no longer accurate.

HMRC employs specialist blockchain analytics tools that trace wallet activity across multiple networks, linking pseudonymous on-chain addresses to verified identities through exchange KYC data. When you withdraw from Coinbase to a personal wallet and later deposit to Binance, HMRC's systems can reconstruct that journey.

HMRC also purchases data from blockchain intelligence firms and participates in international data-sharing through CARF. The result is that HMRC can, in many cases, construct a more complete picture of your crypto activity than you may have yourself. The assumption of privacy that many holders held as recently as 2022 is no longer supportable.

Addressing gaps before HMRC identifies them places you in the strongest possible position. Waiting until enforcement contact removes your ability to access voluntary disclosure terms, which carry substantially lower penalty rates. If you have concerns about your current position, speak with a HashTax specialist before HMRC makes contact first.

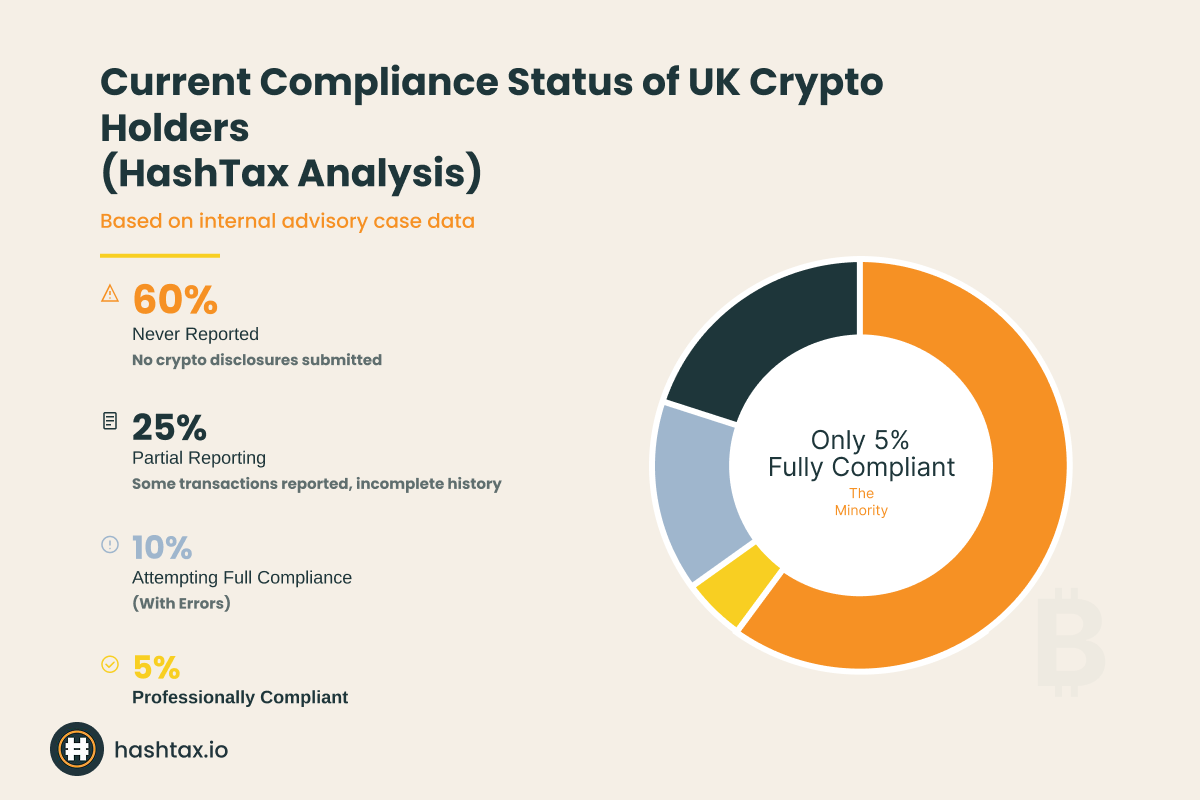

At HashTax, analysing hundreds of crypto portfolios annually reveals consistent patterns — patterns that create serious compliance vulnerabilities.

60% have never reported any cryptocurrency activity to HMRC. This non-reporting usually stems from genuine confusion rather than deliberate evasion. Many believe crypto only becomes taxable when converted to pounds sterling, missing that crypto-to-crypto swaps are taxable disposals. Others assume small holdings fall below thresholds that do not actually exist.

Of the 40% who do report something, most only report part of their activity. A typical pattern is reporting crypto-to-fiat sales while ignoring crypto-to-crypto swaps. This single error can understate taxable gains by 70–90% for active traders. Staking and DeFi rewards are another common omission — the income tax obligations from yields and liquidity provider rewards are frequently missed entirely.

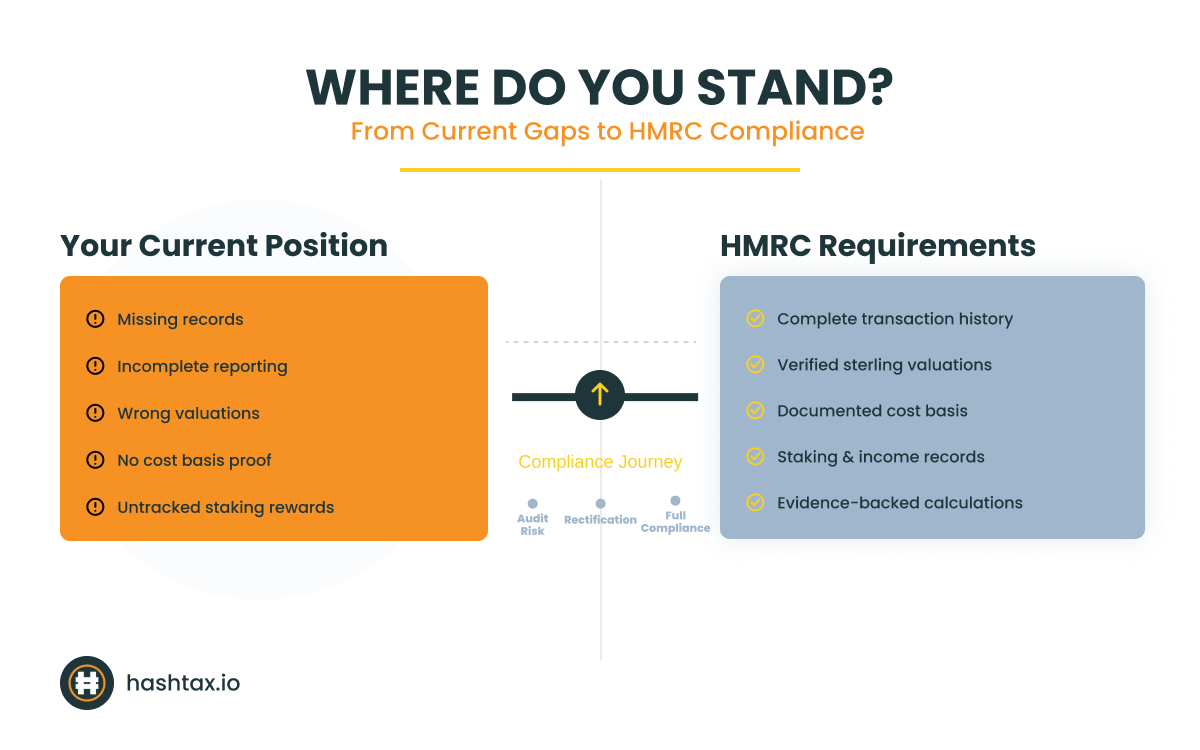

Record-keeping quality rarely meets HMRC standards. Common gaps include missing cost basis information for early purchases, incomplete records from defunct exchanges, no documentation for airdrops or forks, and no tracking of wallet-to-wallet transfers.

Valuation methodology errors affect even good-faith filers. Many use month-end valuations rather than actual disposal date prices, potentially mis-stating gains by 20–40% in volatile markets. Using first-in-first-out instead of HMRC's required share pooling is another pervasive error.

HMRC's expectations far exceed what most holders understand. These are mandatory requirements enforced through penalties — not optional record-keeping suggestions.

Every UK tax resident with cryptocurrency activity faces mandatory reporting obligations, regardless of transaction volume, holding size, or profit levels. A disposal includes:

Capital gains are reported through SA108 Capital Gains Summary pages. You must report each cryptocurrency separately with total disposal proceeds, allowable costs, and the resulting gain or loss. Even if total gains fall below the £3,000 annual exemption, reporting is required if total disposal proceeds exceed £12,000.

Crypto income is reported through different SA sections depending on source:

HMRC's manual CRYPTO22250 specifies what you must produce during an enquiry. For each transaction, your records must capture:

Valuation evidence is critical during enquiries. HMRC expects you to demonstrate how you determined the sterling value at each transaction moment — timestamp-specific exchange prices, averaged multi-source prices, or for exotic tokens, a consistently applied reasonable approach.

Cost basis documentation must show a running share pool for each cryptocurrency: all acquisitions with dates and costs, all disposals reducing the pool, and the resulting gain or loss on each disposal.

Use our Crypto Tax Health Check to identify whether your current record-keeping meets these standards before an HMRC enquiry does it for you.

Missing HMRC deadlines triggers automatic penalties regardless of your reasons for lateness. These are the dates that govern your compliance position:

On voluntary disclosure: There is no formal cut-off, but the terms deteriorate significantly once HMRC opens an enquiry or issues a compliance check. Unprompted disclosures attract penalty rates of 0–30% for offshore matters and 10–30% for UK-only matters. Once HMRC contacts you first, penalty minimums increase substantially.

Interest on unpaid tax runs at Bank of England base rate plus 2.5% from the original due date. If an upcoming deadline is creating pressure, book a consultation with our team to establish a clear action plan before the deadline passes.

HMRC does not provide a single "crypto box" — your obligations span multiple SA pages depending on the nature of your activity. Here is the complete filing process:

Step 1: Register for Self Assessment Register by 5 October following the end of the relevant tax year. If you had crypto activity in 2024/25, the registration deadline was 5 October 2025.

Step 2: Gather your complete transaction history. Collect all exchange download histories, wallet records, DeFi protocol statements, and receipts for crypto received as income. Do not rely on a single exchange export — your complete picture must span every platform you have used.

Step 3: Calculate your capital gains. Apply HMRC's share pooling rules to each cryptocurrency separately. Identify same-day and 30-day bed-and-breakfasting transactions first (calculated outside the pool), then apply the Section 104 pool calculation to the remaining disposals.

Step 4: Identify and categorise crypto income. Staking rewards, mining income, DeFi yield, airdrops, and hard fork receipts each carry specific tax treatment. Confirm the correct income category for each type before reporting.

Step 5: Complete the relevant SA pages, SA108 for capital gains; SA100 or SA103 for income, depending on source. For complex situations involving multiple income types and substantial gains, run our Crypto Tax Health Check first to identify whether a professional review before submission is warranted.

Step 6: Submit by the applicable deadline. Online submission is recommended over paper — it is faster and allows amendments if needed.

If your situation involves multiple years of unreported activity, reconstructive work, or complex DeFi transactions, professional guidance from a specialist cryptocurrency tax consultant ensures accuracy and appropriate HMRC positioning.

The reporting route depends on whether you are filing for the current year, correcting a previous return, or disclosing historical non-reporting. Each route carries different procedural requirements and penalty implications.

Report through your standard Self Assessment return. Complete SA108 with capital gains details and the relevant income pages for any crypto received as income. When completing your return online, the Capital Gains pages must be manually selected — they do not appear by default.

If you have filed a previous return with errors or omissions, you can amend it within 12 months of the original filing deadline. A 2022/23 return filed in January 2024, for example, can be amended until 31 January 2025. Amendments within this window do not automatically attract penalties, though interest on additional tax will apply from the original due date.

For tax years outside the amendment window, or for several years of unreported activity, the voluntary disclosure process applies. This involves contacting HMRC proactively — typically through the Worldwide Disclosure Facility — to disclose the full extent of unreported crypto activity.

A complete voluntary disclosure requires:

Professional preparation of voluntary disclosure submissions substantially improves outcomes, both in terms of completeness and in correctly characterising the disclosure to minimise penalty exposure. Our CryptoTax Navigator service includes full voluntary disclosure preparation, handled by qualified specialists with an unbroken record of HMRC acceptance.

Many crypto holders assume that losing access to cryptocurrency eliminates any tax obligation. The rules are more nuanced — and the procedural requirements are specific.

Losing access through a lost private key or forgotten seed phrase is not automatically treated as a disposal by HMRC. No beneficial ownership has transferred, so no CGT disposal arises.

However, if the cryptocurrency is genuinely irrecoverable, you may be able to make a negligible value claim — a formal assertion to HMRC that the asset has become worthless. This creates a deemed disposal and reacquisition at negligible value, crystallising a capital loss you can use against gains in the same or future tax years. The claim must be made formally; it does not arise automatically.

Where an exchange has collapsed and your assets are trapped in administration, the appropriate action depends on the likely recovery outcome.

Keep all documentation of your holdings at the point of collapse: account statements, transaction histories, and correspondence with administrators.

Theft does not constitute a disposal for CGT purposes in most circumstances, as beneficial ownership was not voluntarily transferred. You cannot therefore, crystallise a capital loss from theft in the same way as from a disposal. The specific facts of how the theft occurred affect the analysis significantly. Speak with a HashTax specialist if you have experienced crypto theft and are uncertain about your reporting obligations.

Hard forks are one of the most technically complex areas of UK cryptocurrency taxation — and one of the most frequently mishandled.

HMRC treats hard fork tokens received by existing holders as having a nil acquisition cost at the time of receipt. This means:

This creates a significant and often overlooked exposure. Many holders received Bitcoin Cash, Ethereum Classic, or other forked tokens and either forgot about them or assumed some cost base transferred. When disposing of these tokens — even years later — the nil cost base rule applies in full.

If you received forked tokens at any point since you began holding crypto:

For older hard forks where records are incomplete, professional reconstruction is often necessary. Our Crypto Tax Health Check will flag whether your hard fork history represents an unaddressed compliance gap.

Closing compliance gaps requires a structured approach across three phases. The complexity of your situation determines which elements apply and how much professional support is appropriate.

For each year with gaps, determine:

Our Crypto Tax Health Check provides a structured assessment of your compliance position, identifying specific risk areas and flagging which elements require professional attention versus straightforward self-resolution.

HashTax provides professional cryptocurrency compliance services delivered by qualified specialists. All services involve expert human analysis — we are not an automated software platform.

Not sure which service applies to your situation? Book a free consultation and we will match you to the right level of support.

HMRC's enforcement capabilities are accelerating. The window for proactive gap closure on the most favourable terms is narrowing.

HashTax offers free 30-minute compliance assessments for all UK crypto holders concerned about their HMRC position. During your confidential assessment, our specialists:

There is no obligation to engage our services. Book your free assessment here.

Path 1 — Immediate Professional Engagement. For readers with multiple years of unreported activity, substantial unpaid tax liabilities, or imminent deadlines with incomplete records.

Contact our priority support team within 24 hours.

Path 2 — Scheduled Professional Planning. For readers with partial reporting gaps, documentation deficiencies, or methodology errors that do not create immediate HMRC risk.

Schedule a planning consultation within the next two weeks.

Path 3 — Guided Self-Resolution. For readers with simple situations and good records.

Start with our Crypto Tax Health Check to understand exactly what needs addressing before you proceed.

Every month of delay increases your financial exposure. Interest accumulates on unpaid tax from the original due date. Voluntary disclosure terms worsen the moment HMRC makes contact before you do. Penalties grow more severe as non-reporting periods lengthen.

The psychological cost compounds too. Living with uncertainty about your HMRC position — anxiety about enforcement letters, the weight of unresolved obligations — creates chronic stress that undermines decision-making. Resolution delivers the clarity and confidence that clients consistently describe as the most valuable outcome of the process.

Visit hashtax.io or contact our specialist team directly to take the first step.

Your crypto tax compliance matters. Let's address it properly together.

Disclaimer: This guide provides general information about UK cryptocurrency tax compliance requirements as at early 2026. Individual circumstances vary significantly and HMRC guidance continues to evolve. Seek professional advice specific to your situation before taking action. HashTax provides professional cryptocurrency accounting services through expert human analysis — we are not automated software.

About HashTax: UK cryptocurrency accounting specialists providing professional tax services exclusively for crypto investors, traders, and businesses. ACCA-registered and HMRC-supervised for Anti-Money Laundering purposes.

HashTax Specialists

Our team of ACCA-qualified accountants specializing in UK cryptocurrency taxation. We provide expert guidance on HMRC compliance, tax planning, and professional advisory services for crypto investors and businesses.

.svg)

.svg)