The single most common misunderstanding among UK crypto traders is the belief that tax only arises when converting to sterling. It does not.

HMRC treats each cryptocurrency as a separate asset. Exchanging Bitcoin for Ethereum is a disposal of Bitcoin and an acquisition of Ethereum. The disposal is taxable — the same way selling Bitcoin for pounds would be. The absence of sterling at any point in the transaction does not change its tax character.

This applies to every trade type:

Each event requires a gain or loss calculation. The gain is the difference between the sterling value of the asset received and the allowable cost of the asset disposed of, calculated using the share pooling rules.

The volume of trades you make determines how complex this obligation becomes — and, at sufficient volume, whether Capital Gains Tax rules continue to apply at all.

Trading activity across a tax year falls broadly into three tiers. Each tier carries distinct tax treatment, record-keeping demands, and compliance risk.

These thresholds are proxies, not precise rules. HMRC does not publish a transaction number that automatically triggers professional trader classification. The boundaries are indicators. The sections below explain what each tier means in practice.

The casual trader makes occasional, deliberate transactions — portfolio rebalances, strategic exits, selective swaps. Trades are spread across the year with days or weeks between them.

Typical casual trader characteristics:

Tax treatment operates entirely under Capital Gains Tax. Each disposal requires calculating disposal proceeds, allowable cost (using the Section 104 pool), and the resulting gain or loss. Net gains above the £3,000 annual exempt amount are taxable at 18% (basic rate taxpayers) or 24% (higher rate taxpayers).

Record-keeping at this level is demanding but manageable. With under 20 transactions, a spreadsheet capturing the date, asset, quantity, sterling value at transaction time, fees, and pool balance after each trade provides sufficient documentation.

The Section 104 pool is straightforward at low transaction volumes. With 10–15 disposals across the year, each pool calculation can be verified manually. There is no ambiguity about which cost basis applies — the pool methodology is mechanical and produces a clear result.

The £3,000 annual exempt amount provides meaningful shelter. A casual trader whose total net gains fall below this threshold owes no Capital Gains Tax for the year, regardless of the number of disposals.

Strategic use of the allowance is achievable without professional support at this level. Spreading disposals across two tax years, crystallising losses before April 5 to offset gains, and timing sales around the annual exempt amount are all strategies that casual traders can implement with reasonable confidence.

Compliance at this tier is achievable with good habits. The primary risk is underreporting — particularly the failure to recognise crypto-to-crypto swaps as taxable disposals. An investor who understands the basic rule and keeps accurate records can handle their Self Assessment reporting without undue complexity.

Use the Tax Impact Calculator to model your estimated CGT position before the tax year closes.

The active trader transacts regularly — across multiple exchanges, multiple cryptocurrencies, sometimes multiple times per week. Activity at this level introduces complexity that casual trading does not.

Typical active trader characteristics:

Each disposal still falls under Capital Gains Tax at this tier. But the interaction of high transaction volumes with HMRC's identification rules creates significant scope for error.

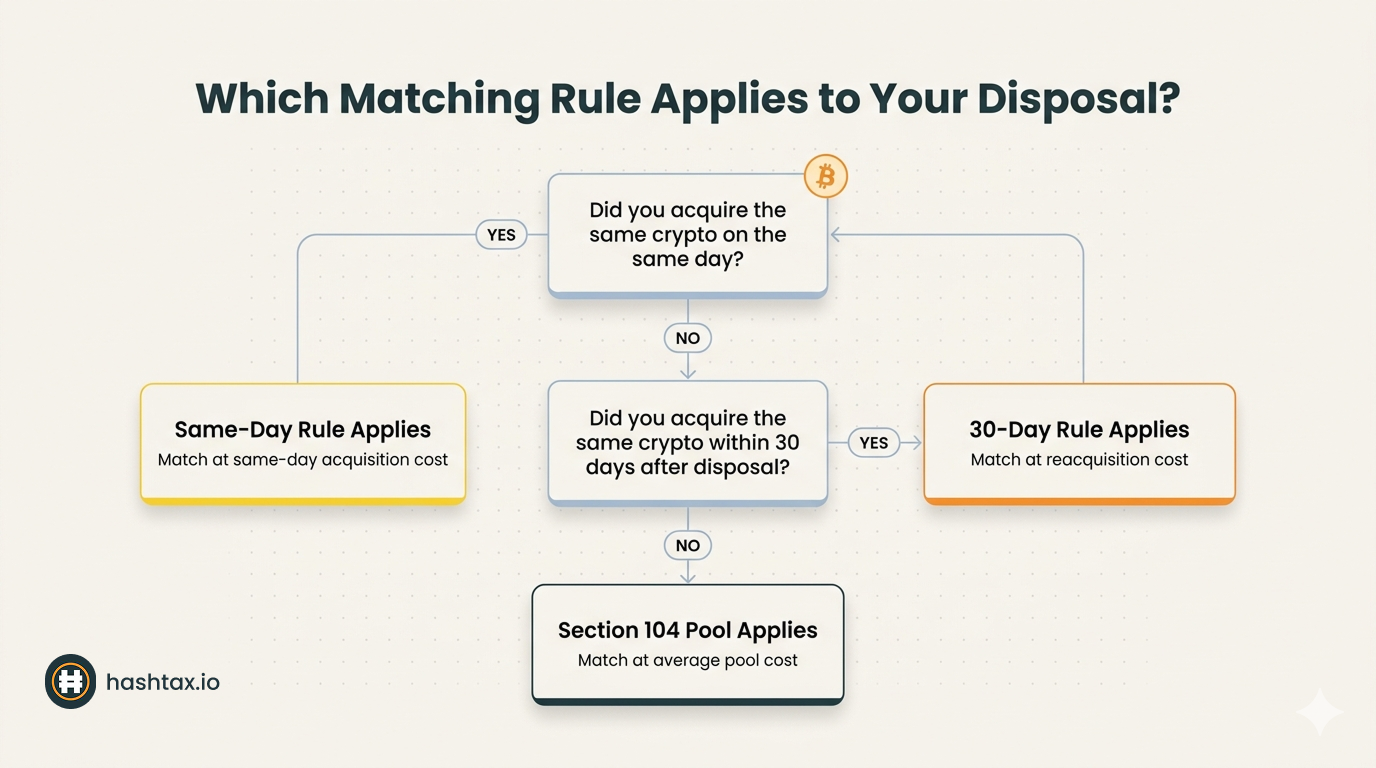

The Section 104 pool does not apply to every disposal. Before pooling, two priority rules must be applied in sequence to each disposal:

Rule 1 — Same-day rule: Any cryptocurrency acquired on the same day as a disposal is matched against that disposal first, at acquisition cost, before the pool is consulted.

Rule 2 — 30-day rule (bed and breakfasting): Any cryptocurrency acquired within 30 days after a disposal is matched against that disposal, before the pool. This rule prevents investors from selling assets to crystallise a loss and immediately reacquiring them to reset their cost basis.

Only after both priority rules have been applied does the Section 104 pool come into play.

Applying these rules incorrectly — or ignoring them entirely — produces incorrect gain calculations. An active trader making 200 trades per year may have dozens of disposals where the priority rules apply. Each error compounds into a cumulative misstatement.

Active traders have access to tax-loss harvesting as a meaningful strategy. Where positions have declined in value, crystallising those losses before the tax year ends offsets gains realised elsewhere. At higher transaction volumes, there are more opportunities to identify and act on these positions.

Deductible costs also become more significant at this tier. Transaction fees, gas fees on DeFi protocols, and exchange commissions are all potentially allowable costs that reduce taxable gains. At low transaction volumes, these amounts are minor. At 200–500 transactions per year, the cumulative impact can be material.

Active traders who maintain accurate, complete records and apply the identification rules correctly can produce defensible Self Assessment filings. The challenge is that the rules are precise and the volume of data is high. A single spreadsheet approach becomes increasingly error-prone as transaction frequency grows.

At this tier, the Tax Complexity Score tool is worth completing. It will indicate whether your portfolio's complexity suggests professional review is warranted before you file.

The professional trader executes a high volume of transactions systematically. At this level, HMRC may no longer treat trading activity as investment — it may classify it as a trade, subject to Income Tax rather than Capital Gains Tax.

This reclassification is not triggered by transaction count alone. HMRC applies a multi-factor test considering:

A full-time employee who makes 600 trades from personal capital, without leverage, as part of a broader portfolio may remain an investor. A self-employed individual making 600 trades using leveraged positions, following systematic technical strategies, and deriving primary income from trading is more likely to be classified as a trader.

The distinction has significant consequences.

.png)

The risk of misclassification runs in both directions. An investor who should be classified as a trader but files under CGT rules may have underpaid Income Tax and National Insurance. A trader who claims professional trader status incorrectly, seeking to deduct business expenses, may face challenge on both the classification and the deductions.

HMRC does not signal reclassification in advance. It emerges through enquiry — often when a pattern of high-volume trading activity does not match the CGT treatment reported.

Traders who are correctly classified as running a trading business face an additional decision: the appropriate legal structure. Operating as a sole trader subjects all profits to Income Tax and Class 4 National Insurance. Incorporating as a limited company introduces Corporation Tax at current rates, with different treatment of profit extraction and loss carry-forward.

These decisions depend on profit levels, withdrawal patterns, and long-term plans. There is no universally correct answer. The appropriate structure should be determined with professional advice specific to your circumstances.

The same-day rule and 30-day rule described in the active trader section apply to all traders — including casual traders. They are not optional advanced considerations. They are mandatory components of the CGT calculation that must be applied before the Section 104 pool.

The most common error at every tier is applying pool cost basis to disposals that should have been matched under the priority rules first.

Same-day rule in practice: You sell 1 BTC and also buy 0.5 BTC on the same day. The 0.5 BTC acquired is matched against 0.5 of the BTC sold at today's acquisition price. The remaining 0.5 BTC sold is matched against the pool. Two different cost bases apply to a single disposal event.

30-day rule in practice: You sell 2 ETH on 1 March and buy 2 ETH on 20 March (19 days later). The reacquisition matches against the earlier disposal. The pool is not used. If the purpose was to crystallise a loss by selling low and rebuying, the rule prevents that loss from being recognised. The disposal and reacquisition are matched instead, and the gain or loss reflects the difference between the two recent prices.

Bed and breakfasting and the 31-day gap: The 30-day rule does not prevent you from selling and rebuying after a 31-day gap. A gap of 31 or more days between disposal and reacquisition allows the disposal to be matched against the pool cost basis. The loss or gain is recognised. This is a legitimate planning tool used by traders who want to crystallise losses while maintaining their position, and it requires precise timing.

Transaction count is a starting point. It is not the complete answer.

Work through the following questions to assess your classification risk:

A casual investor who answers "no" to most of these questions and has under 20 disposals is unlikely to face reclassification. A high-frequency participant who answers "yes" to several should consider professional review of their classification before filing.

If you are uncertain whether your activity places you at the boundary between active and professional trader treatment, that uncertainty itself is a reason to seek professional advice before submitting your return. A filing made on an incorrect classification basis is significantly more difficult to correct after submission than before it.

Complete the Crypto Tax Health Check to assess your current compliance position before proceeding with Self Assessment.

Crypto trading tax becomes progressively more demanding as activity increases. At the casual level, the risks are manageable with care and good records. At the active level, the identification rules introduce precision requirements that are easy to apply incorrectly at scale. At the professional level, classification questions and business structure decisions carry long-term consequences that are difficult to reverse.

Professional advice at each tier serves a different purpose. For casual traders, it provides accuracy assurance and compliance confidence. For active traders, it ensures the identification rules are correctly applied across every disposal and that the Self Assessment filing is defensible if reviewed. For professional-level traders, it addresses classification, structure, and ongoing compliance as a trading business.

HashTax provides specialist human analysis across all trading tiers. Our ACCA-registered specialists review your full transaction history, apply the correct identification rules to every disposal, and prepare Self Assessment filings that reflect your actual tax position accurately. We are not an automated platform. Every engagement is reviewed by a qualified professional.

Services are delivered by qualified human specialists. HashTax is not an automated platform or software solution.

Book a trading tax consultation with a HashTax specialist

A HashTax specialist will review your trading activity, identify your tier classification, and confirm whether any identification rule issues affect your current position. We will advise on the correct approach for your Self Assessment filing before the 31 January 2027 deadline.

The assessment carries no obligation to proceed. Understanding your position before you file is always preferable to correcting it after.

Book your free trading tax assessment

If you have already filed returns that may contain identification rule errors: Book an urgent consultation — amended returns can be submitted within 12 months of the original filing deadline, but the window closes.

If you want to check whether your records are complete enough to file correctly: Complete the Crypto Tax Health Check for an immediate assessment of your compliance position.

If you want to model your estimated tax liability before filing: Use the Tax Impact Calculator to estimate your CGT position based on your transaction history.

The 31 January 2027 deadline for 2025/26 Self Assessment returns is the payment deadline as well as the filing deadline. Interest on late-paid tax begins the day after. Penalties for late filing begin 30 days after the deadline and escalate at 3, 6, and 12 months.

Errors in trading tax returns — particularly misapplication of the identification rules — are among the most common triggers for HMRC enquiry into crypto portfolios. A correctly prepared return is the most effective protection against enquiry risk.

For traders approaching the active-to-professional boundary, classification decisions made now determine the tax treatment of your entire year's activity. This decision should be made deliberately, with professional input, before your return is submitted — not retrospectively after HMRC has formed its own view.

Visit HashTax to learn more about our professional crypto tax services, or book a consultation to discuss your trading position with a specialist.

Your crypto tax compliance matters. Let's address it properly together.

HashTax Specialists

Our team of ACCA-qualified accountants specializing in UK cryptocurrency taxation. We provide expert guidance on HMRC compliance, tax planning, and professional advisory services for crypto investors and businesses.

.svg)

.svg)