The UK tax year ends on 5 April 2026. After that date, your options for the 2025/26 tax year close permanently.

Every crypto strategy that could have reduced your liability — crystallising losses, optimising your Capital Gains Tax allowance, restructuring holdings — becomes unavailable the moment the tax year ends. You cannot go back.

At HashTax, we see the same pattern every year. Clients contact us in May with complex portfolios and ask what we can do to reduce their bill. The answer is always the same: very little, because the planning window has passed.

The good news is that the planning window is still open. This guide sets out the strategies available to you right now, and what each requires in practice.

Before applying any strategy, you need to understand your current position. That means knowing two things: what you have disposed of, and what that disposal is worth in sterling at the time of the transaction.

HMRC treats every crypto disposal as a potential taxable event. Disposals include selling crypto for fiat, exchanging one crypto for another, using crypto to buy goods or services, and gifting crypto to anyone other than a spouse or civil partner.

Your tax rate depends on whether a disposal produces a capital gain or income. These are treated very differently.

These are the rates that apply after using your available annual allowances. Understanding which rate applies to each transaction in your portfolio is the starting point of any strategy.

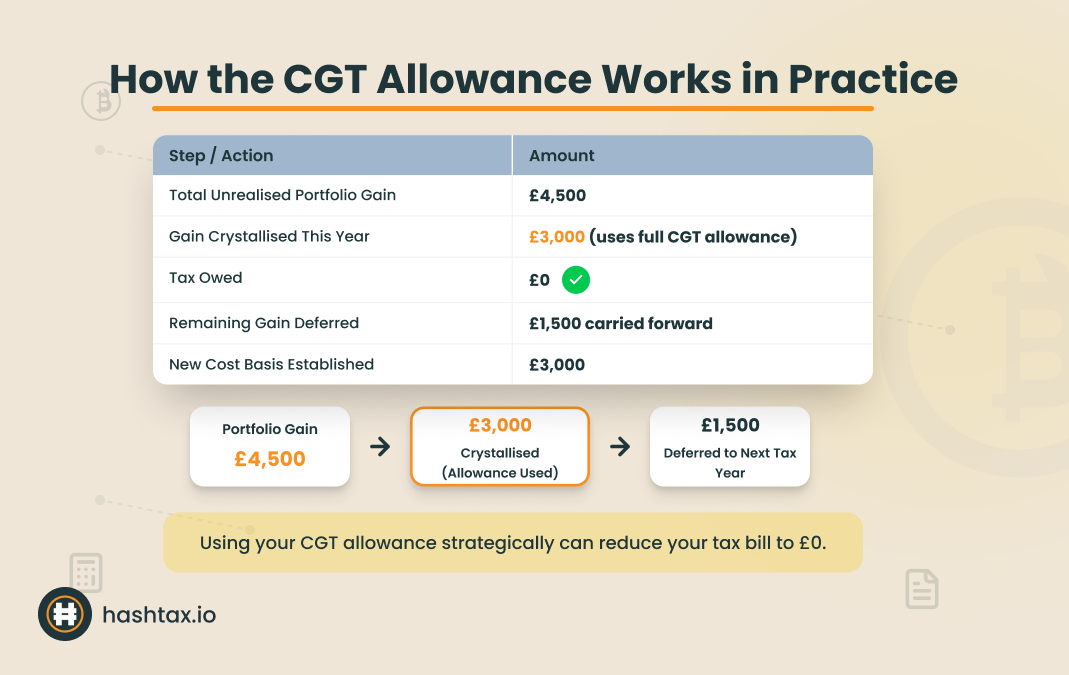

The Capital Gains Tax annual exempt amount for 2025/26 is £3,000. This allowance resets on April 6 — it cannot be carried forward.

If your total capital gains are below £3,000 after offsetting losses, you pay no Capital Gains Tax on crypto disposals for the year. If you have not yet made sufficient gains to reach this threshold, you may be leaving tax-free disposal capacity unused.

Consider crystallising gains on holdings that have appreciated, up to the £3,000 limit. This resets the cost basis of those assets at current market value. Future gains will be calculated from the new, higher base.

This strategy requires careful timing. If you are considering this approach, use our Tax Impact Calculator to model the effect on your specific portfolio before making any disposals.

Capital losses reduce your taxable gains on a pound-for-pound basis. If you hold assets that are currently worth less than you paid for them, disposing of them before April 5 locks in those losses for use in the current tax year.

Losses that exceed your gains in one year are not wasted. You can carry them forward indefinitely and offset them against future gains. But losses only enter the system once they are crystallised — unrealised losses do nothing for your tax position.

To crystallise a loss, you must dispose of the asset. A disposal for tax purposes requires an actual transaction, not simply a decision to treat the asset as worthless.

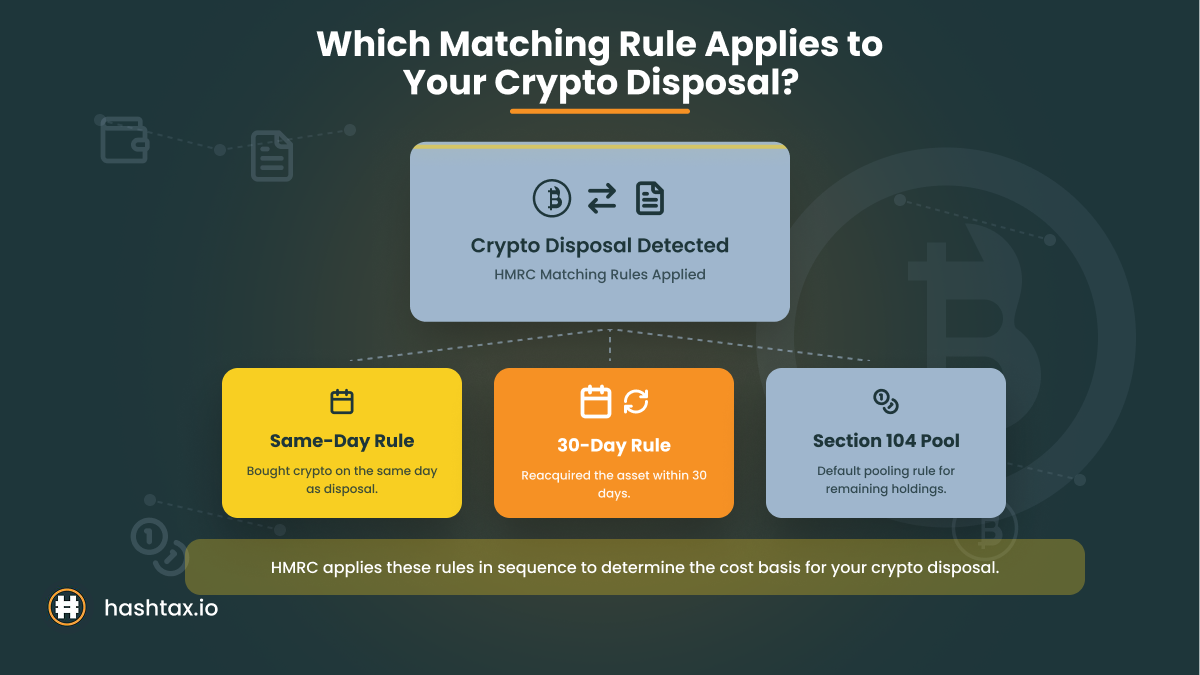

Bed and breakfasting is the practice of selling an asset and rebuying it shortly after, with the intention of establishing a loss or resetting a cost basis. HMRC has specific rules that apply to crypto, derived from share identification rules.

The key rules are:

These rules prevent you from simply selling and immediately rebuying to crystallise losses artificially. However, they do not prevent you from selling and reacquiring after 30 days. A 31-day gap between disposal and reacquisition is sufficient for the loss to be recognised against the original pool.

The critical requirement is precision in your records. The timing of each transaction — to the minute, not just the day — determines which rule applies. Errors here are a common source of incorrect tax calculations.

If you are unsure which rule applies to your transactions, this is not an area for estimation. Incorrect matching can overstate or understate a gain significantly. Book a consultation with a HashTax specialist to review your specific transaction history.

Transfers between spouses and civil partners are treated as made at no gain, no loss. This means you can transfer crypto to a spouse without triggering a disposal, and they can then dispose of the asset using their own CGT allowance and tax rates.

If your spouse is a basic rate taxpayer and you are a higher rate taxpayer, disposals made by your spouse will be taxed at 18% rather than 24%. If your spouse has not used their £3,000 CGT allowance, the first £3,000 of their gains will be free of tax entirely.

This strategy works only where the transfer is a genuine gift, not a transaction designed purely to avoid tax. HMRC will scrutinise arrangements where the asset is transferred and immediately repurchased by the original owner.

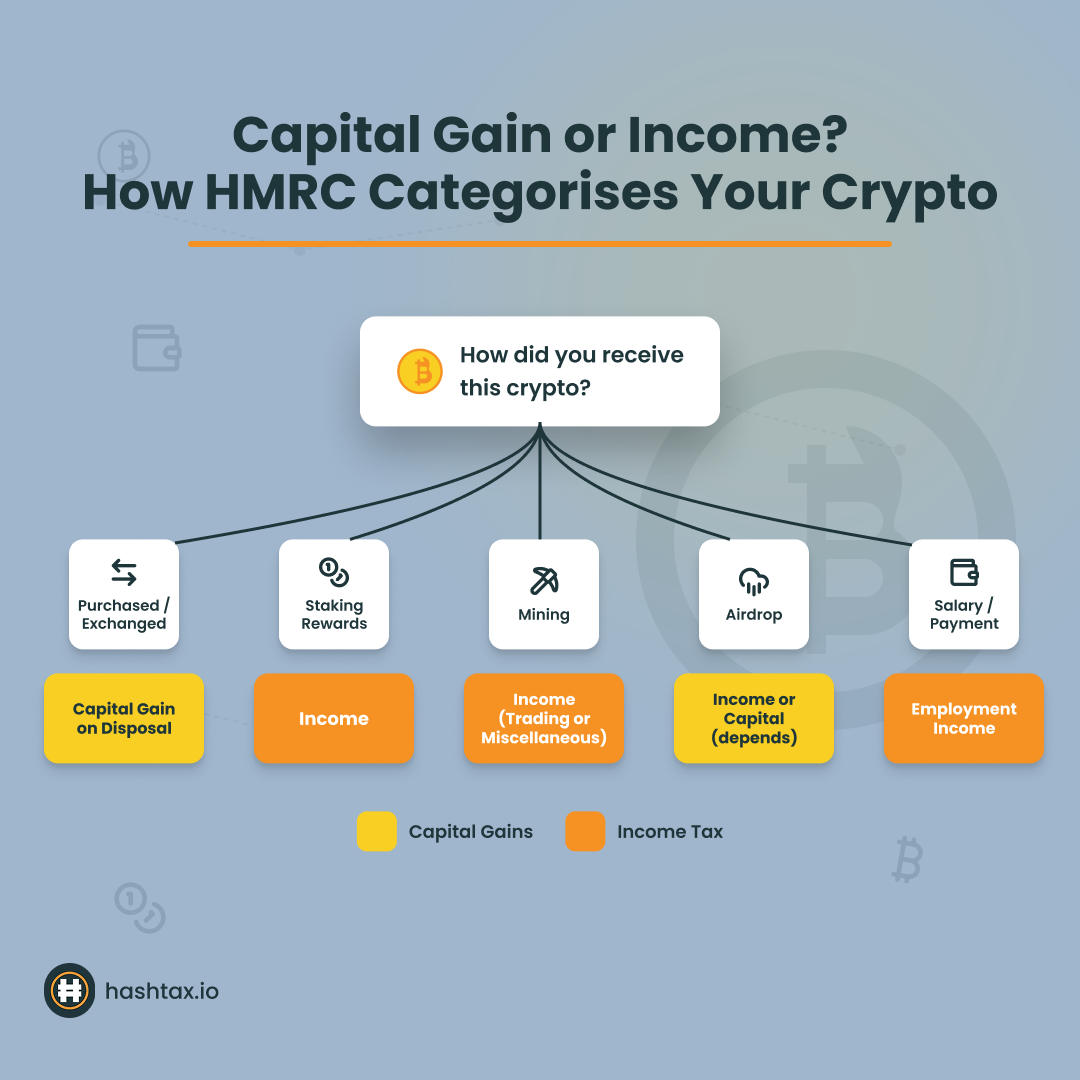

Not all crypto activity produces capital gains. Staking rewards, mining income, and certain airdrops are taxed as income at your marginal rate in the year they are received. These amounts cannot be reduced by your CGT allowance.

If you have been staking consistently throughout 2025/26, you may have accumulated significant taxable income that requires reporting through Self Assessment even if you have not sold a single asset. HMRC's position is that staking rewards are taxable when received, at the sterling value on the date of receipt.

Reviewing your staking activity now allows you to quantify this liability before the tax year closes. It also gives you the opportunity to identify any deductible costs — such as electricity costs for mining operations — that should be recorded before records become harder to locate.

The distinction between income and capital gains is the most consequential categorisation in crypto tax. Getting it wrong has significant financial consequences.

HMRC's approach follows a purpose test. If you are acquiring and disposing of crypto with the primary intention of making a profit from price movements, your activity may be classified as trading — which means income tax, not capital gains tax, applies to all of it.

The threshold for "trading" status is not defined by transaction frequency alone. HMRC considers:

Most retail investors who buy and sell crypto periodically are not classified as traders. But very active participants — particularly those operating bots, high-frequency strategies, or leveraged positions — face genuine uncertainty about their classification.

If you are unsure whether your activity qualifies as trading or investing, this classification should be confirmed before you file. Misclassifying trading income as capital gains is a common error that HMRC identifies during enquiries. Use our Crypto Tax Health Check to assess your risk profile before the tax year ends.

Exchanging Bitcoin for Ethereum is a disposal of Bitcoin. HMRC treats each exchange as if you sold the first asset at its market value and used the proceeds to purchase the second. A taxable gain or loss arises on the Bitcoin at the point of exchange, regardless of whether you received any sterling.

Many investors only consider their tax position when they convert to fiat. This leads to significant underreporting of gains on crypto-to-crypto trades. Review your full transaction history, not just your fiat withdrawals.

Your gain is calculated on the difference between disposal proceeds and allowable costs. Allowable costs include the original acquisition price, transaction fees paid at acquisition, and any costs directly associated with the disposal.

Platform fees, gas fees, and exchange commissions are all potentially allowable. Keeping records of these costs can meaningfully reduce your taxable gains. Most crypto tax software does not accurately capture all allowable costs — professional review is particularly valuable here.

The January 31 filing deadline applies to filing and payment — not to planning. All strategies that reduce your liability must be implemented before April 5. By January, the tax year is nine months closed. Planning options are gone.

The investors who achieve the best outcomes act in March, not January.

Crypto tax strategy is not a DIY-friendly activity. The rules governing identification, pooling, income categorisation, and spousal transfers are precise and technical. A single classification error can alter your tax liability significantly.

HashTax provides expert human analysis — not automated software outputs. Our specialists review your complete transaction history, identify the strategies available to you before April 5, and prepare your Self Assessment submission with full HMRC compliance.

Every engagement is handled by ACCA-registered professionals operating under HMRC supervision. Our clients benefit from an analysis that software platforms cannot replicate.

Services are delivered by qualified human specialists. HashTax is not an automated platform or software solution.

Book a year-end planning consultation

A HashTax specialist will review your portfolio position and identify the strategies available to you before April 5. The assessment takes approximately 30 minutes and carries no obligation to proceed.

We will confirm your current CGT position, flag any income tax obligations from staking or mining, and advise whether any immediate actions are worth taking before the tax year closes.

If you need to act before April 5: Book an urgent year-end consultation — our team prioritises deadline-sensitive engagements.

If you want to understand your position first: Complete the Tax Impact Calculator for an immediate indication of your estimated liability.

If you prefer to manage your own filing: Use the Crypto Tax Health Check to confirm your compliance position before submitting your return.

Every week that passes between now and April 5 reduces the strategies available to you. Losses cannot be crystallised retrospectively. Spousal transfers must be completed before disposal. The CGT allowance cannot be used once the tax year has closed.

HMRC interest and penalties begin accumulating from January 31 2027 if your return is not filed. Deliberate underreporting carries significantly higher penalties. Addressing your tax position before April 5 costs less — in every sense — than addressing it after the fact.

Visit HashTax to learn more about our professional crypto tax services, or book a consultation to speak with a specialist about your specific position.

Your crypto tax compliance matters. Let's address it properly together.

HashTax Specialists

Our team of ACCA-qualified accountants specializing in UK cryptocurrency taxation. We provide expert guidance on HMRC compliance, tax planning, and professional advisory services for crypto investors and businesses.

.svg)

.svg)