A disposal event is any transaction through which you cease to hold a cryptocurrency asset. It is the trigger point at which Capital Gains Tax (CGT) liability — or an allowable loss — is calculated under UK tax law.

HMRC's definition is broader than most investors expect. It does not require the involvement of pounds sterling. It does not require a profit. It does not have a minimum transaction size. Any transaction in which you part with ownership of a cryptocurrency asset is, in principle, a taxable event.

This guide addresses the four misconceptions about disposal events that most commonly lead to incorrect or incomplete Self Assessment returns.

.png)

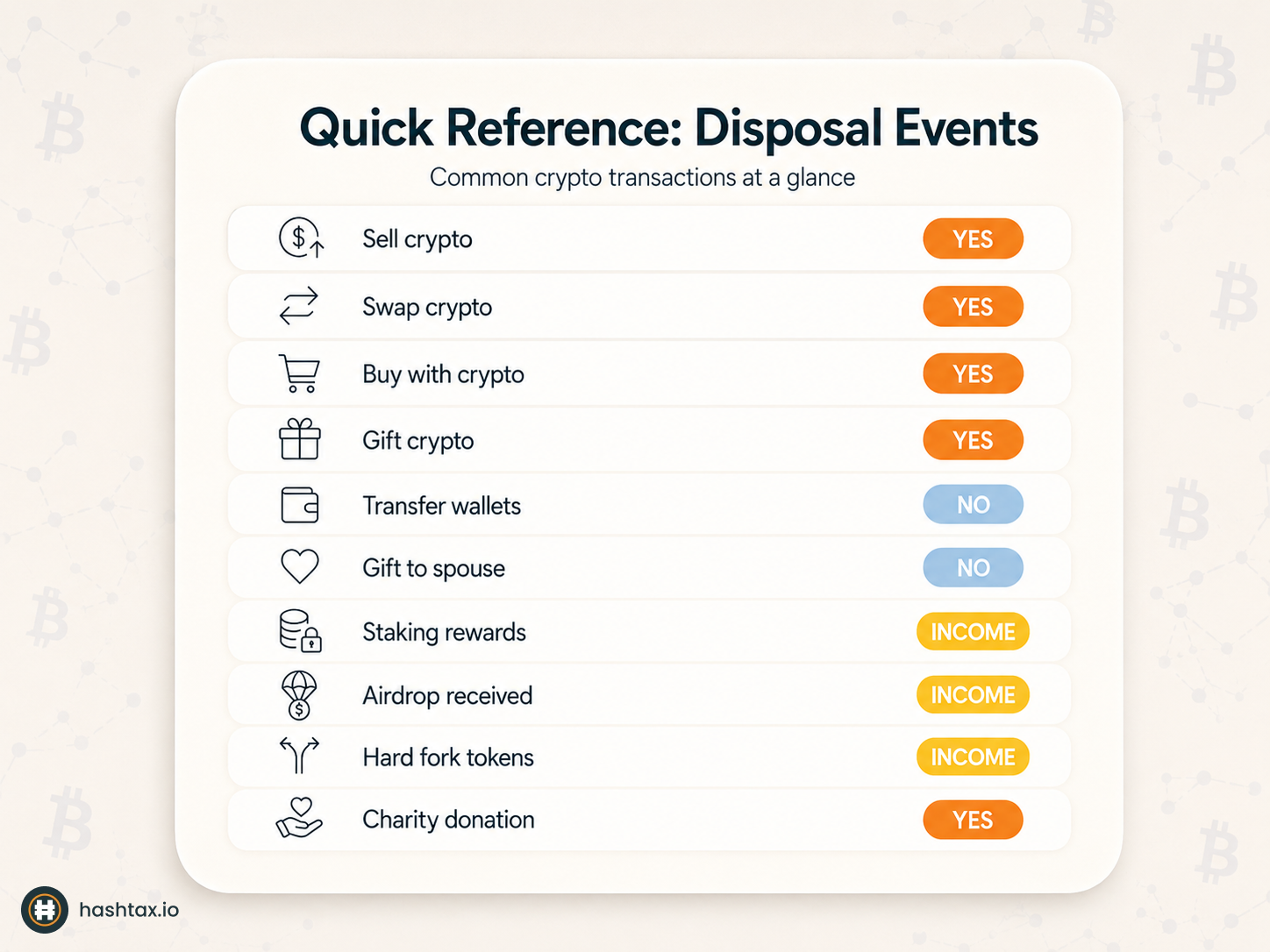

Many investors believe that tax is only triggered when cryptocurrency is converted into sterling. Under this view, swapping Bitcoin for Ethereum, or spending crypto on a purchase, is not a taxable event because no pounds were received.

HMRC treats each cryptocurrency as a separate capital asset. Exchanging one cryptocurrency for another is a disposal of the first asset and an acquisition of the second. The sterling value of the asset at the point of exchange is used to calculate the disposal proceeds — regardless of whether any sterling was actually received.

Using cryptocurrency to pay for goods or services is treated in the same way. You are considered to have disposed of the crypto at its market value on the date of the transaction.

HMRC's cryptoassets manual is explicit: "exchanging one type of cryptoasset for a different type of cryptoasset" and "using cryptoassets to pay for goods or services" are both disposal events. This has been HMRC's confirmed position since 2019 and has not changed.

An investor who has spent a tax year swapping between cryptocurrencies — without ever converting to sterling — may have generated dozens of disposal events, each requiring a gain or loss calculation. Those disposals accumulate toward the annual exempt amount in the same way cash sales do.

Failing to account for these events means the Self Assessment return is incomplete. If HMRC identifies the gap through exchange data — which they routinely collect from UK platforms — the investor faces additional tax, interest, and potential penalties.

Complete the Crypto Tax Health Check if you have made crypto-to-crypto swaps in any open tax year without recording them as disposals.

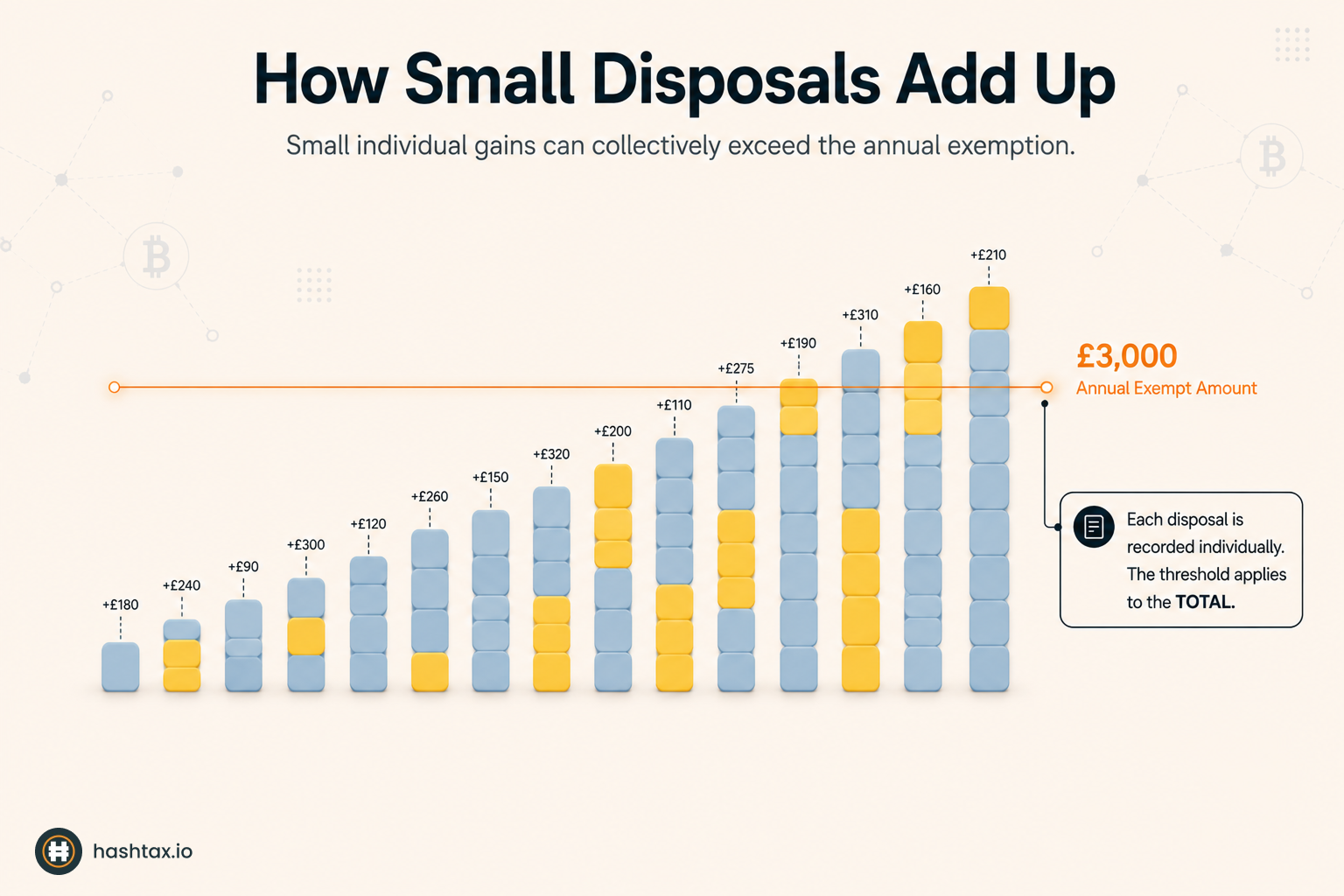

A common belief is that HMRC applies a minimum transaction size below which disposal events can be ignored. Under this view, small swaps, coffee purchases made with crypto, or minor trades under a certain value do not need to be reported.

There is no minimum transaction size for a disposal event. Every disposal in a tax year contributes to your net gain or loss position for that year. The annual exempt amount (£3,000 for 2024/25) applies to your total net gains — not to individual transactions.

HMRC's guidance requires records to be kept of all cryptocurrency transactions. The reporting threshold for Self Assessment is based on total proceeds exceeding £50,000, or net gains exceeding the annual exempt amount — not on the size of any individual transaction.

Multiple small gains can accumulate above the annual exempt amount without any single transaction being large. An investor with fifty modest disposals in a tax year has the same reporting obligation as one with a single large disposal — if their net gains are equivalent.

The record-keeping consequence is equally important. Disposal events with no gain today still establish the cost basis for future transactions. Missing records for small transactions can make it impossible to calculate accurate gains on larger disposals later.

Some investors — particularly those who have read about HMRC's broad definition of disposals — conclude that transferring cryptocurrency between wallets they own constitutes a taxable event.

A transfer between wallets under your own beneficial ownership is not a disposal. You have not parted with ownership of the asset. HMRC does not treat same-owner transfers as taxable events.

HMRC's guidance confirms that transfers between wallets owned by the same individual do not constitute a disposal. The asset remains in your beneficial ownership throughout.

The transfer itself is not taxable — but it must be correctly identified in your records. A transfer from Exchange A to a hardware wallet can appear in transaction history as an outflow on Exchange A and an inflow on the hardware wallet. Without records confirming both sides of the transfer, it may appear as an unmatched disposal and acquisition.

This is one of the most common sources of phantom gains in incorrectly prepared crypto tax returns. Software tools that cannot match transfers across platforms will treat them as separate disposal and acquisition events, producing an inflated gain figure.

Use the Tax Complexity Score if you use multiple wallets or exchanges — transfer mismatching is one of the primary complexity indicators.

Gifting cryptocurrency — to a family member, friend, or charity — is sometimes assumed to fall outside the CGT rules because nothing is sold and no proceeds are received.

Gifting cryptocurrency to anyone other than your spouse or civil partner is a disposal at market value. You are treated as having received consideration equal to the market value of the asset on the date of the gift, even though you received nothing. If the asset has increased in value since acquisition, a capital gain arises.

HMRC's guidance confirms that gifts of cryptoassets are disposals. The market value at the date of the gift is treated as the disposal proceeds for CGT purposes.

Two specific exceptions apply:

Gifts to adult children, parents, siblings, or friends do not qualify for either exception. The market value rule applies in full.

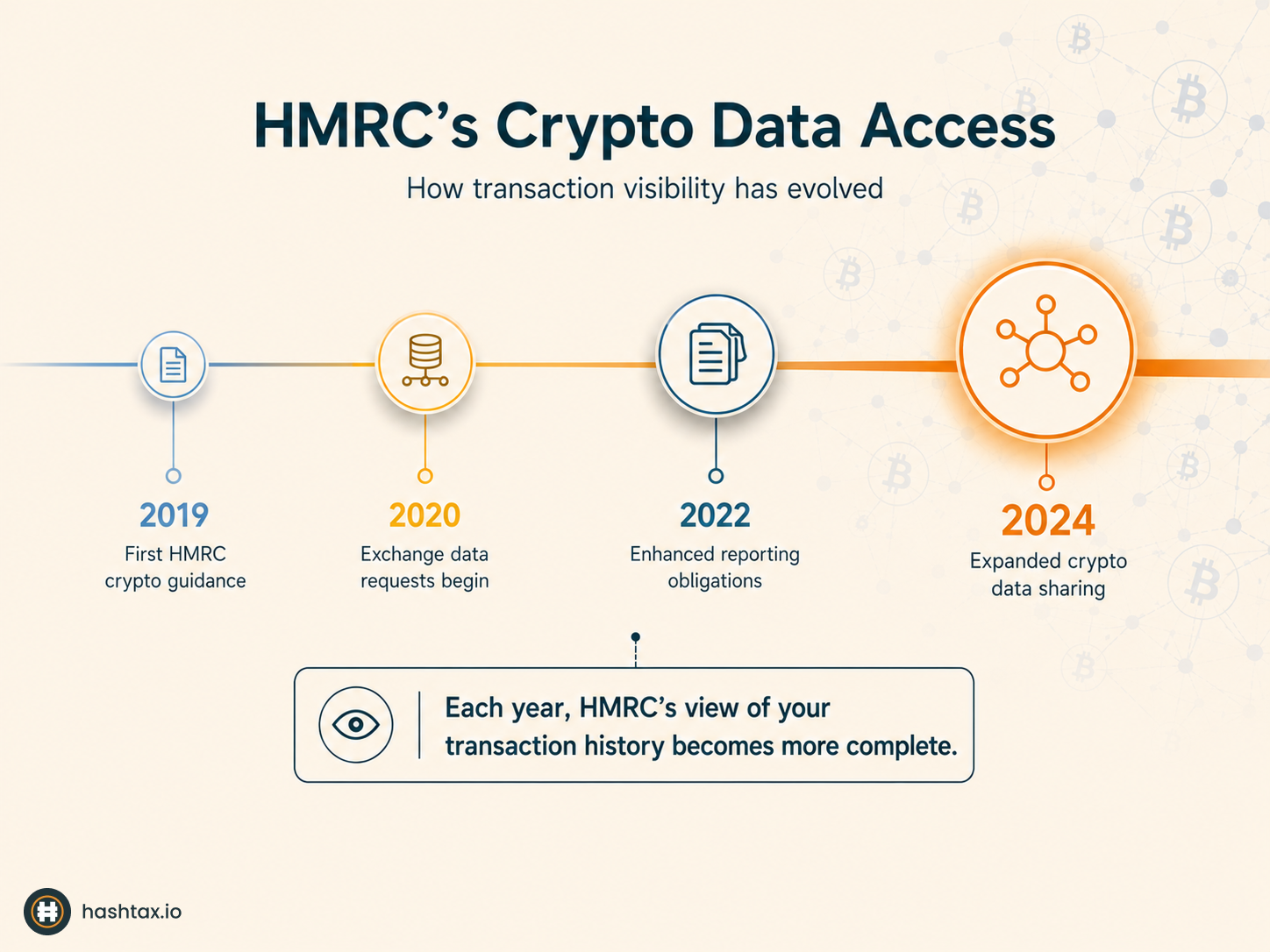

HMRC's data collection from cryptocurrency exchanges has expanded significantly. UK-regulated exchanges are required to provide customer transaction data to HMRC. HMRC has also used its legal powers to request data from major international exchanges operating in the UK market.

HMRC's Connect system cross-references data from multiple sources — exchange records, bank transfers, Companies House filings, and Self Assessment returns. Disposal events that appear on exchange records but are absent from a Self Assessment return create a discrepancy that may trigger an enquiry.

Voluntary disclosure of previously unreported disposals — before HMRC initiates contact — results in substantially lower penalties than correction after an enquiry opens.

Identifying every disposal event across a full tax year — particularly for investors using multiple exchanges, DeFi protocols, or hardware wallets — is a specialist task. The consequences of missing events range from an underreported return to a formal HMRC enquiry.

HashTax provides expert human analysis — not automated software outputs. Our ACCA-registered specialists review your complete transaction history, identify every disposal event, match transfers correctly across platforms, and prepare your Self Assessment with full professional accountability.

Crypto tax software can assist with data aggregation. It cannot replace specialist review of transfer matching, identification rule application, or the treatment of complex transaction types. A software-generated report that contains unmatched transfers or misclassified events is not HMRC-defensible without professional verification.

All our services are delivered by qualified specialists — we are not an automated software platform. Every engagement involves human review of your transaction history and HMRC-compliant reporting prepared under ACCA professional standards.

Book a free consultation with a HashTax specialist

A HashTax specialist will review your transaction history and identify whether all disposal events have been correctly recorded and reported. We will confirm which tax years require attention and advise on the most efficient path to a compliant return. There is no obligation to proceed.

Book your free compliance assessment

Path 1 — Immediate: If you have unreported disposal events from previous tax years, book an urgent consultation with a HashTax specialist — voluntary disclosure now protects against significantly higher penalties later.

Path 2 — Scheduled: If you want to confirm your current year position before the Self Assessment deadline, complete the Crypto Tax Health Check to identify any gaps in your records.

Path 3 — Self-Assessment: If you are unsure whether your transaction history is complex enough to require professional review, use the Tax Complexity Score as your starting point.

HMRC's exchange data collection is cumulative. Each year that passes adds further transaction records to what HMRC can cross-reference against submitted returns. Acting before HMRC identifies a discrepancy preserves access to the most favourable penalty treatment available.

Visit HashTax to learn more about our professional crypto tax services, or book a consultation to speak directly with an HMRC crypto tax specialist about your situation.

Your crypto tax compliance matters. Let's address it properly together.

HashTax Specialists

Our team of ACCA-qualified accountants specializing in UK cryptocurrency taxation. We provide expert guidance on HMRC compliance, tax planning, and professional advisory services for crypto investors and businesses.

.svg)

.svg)