HMRC treats cryptocurrency as a capital asset — in the same category as shares or investment property. When you dispose of a capital asset at a profit, Capital Gains Tax (CGT) applies to the gain.

This treatment has been HMRC's position since 2019 and is confirmed in their cryptoassets manual. It applies to all types of cryptocurrency, regardless of whether you consider your activity investing or trading.

Understanding the CGT rules that apply to your portfolio is the starting point for any compliant Self Assessment return.

%20(1).png)

A disposal is any transaction in which you part with ownership of a cryptocurrency. HMRC's definition is broad. The following all count as disposals:

Transferring cryptocurrency between your own wallets is not a disposal. However, HMRC requires you to maintain records that demonstrate the transfer was between wallets under your own beneficial ownership.

Each disposal in a tax year must be reported individually if your total disposal proceeds exceed £50,000, or if your net gains exceed the annual exempt amount.

Your capital gain on a disposal is calculated as:

Disposal proceeds minus allowable costs = gain or loss

Disposal proceeds are the sterling value you received (or the market value of what you received, in a swap). Allowable costs include:

Any gain is added to your other capital gains for the tax year. Any loss can offset gains in the same year, or be carried forward to offset future gains.

%20(2).png)

The annual exempt amount is the threshold below which Capital Gains Tax is not charged. For 2024/25, the annual exempt amount is £3,000.

This applies to your total net capital gains across all assets in the tax year — not just cryptocurrency. Gains from shares, property disposals, and other assets all count toward the same threshold.

If your total net gains for the year are below £3,000, no CGT is payable and no reporting is required — unless your total disposal proceeds exceed £50,000.

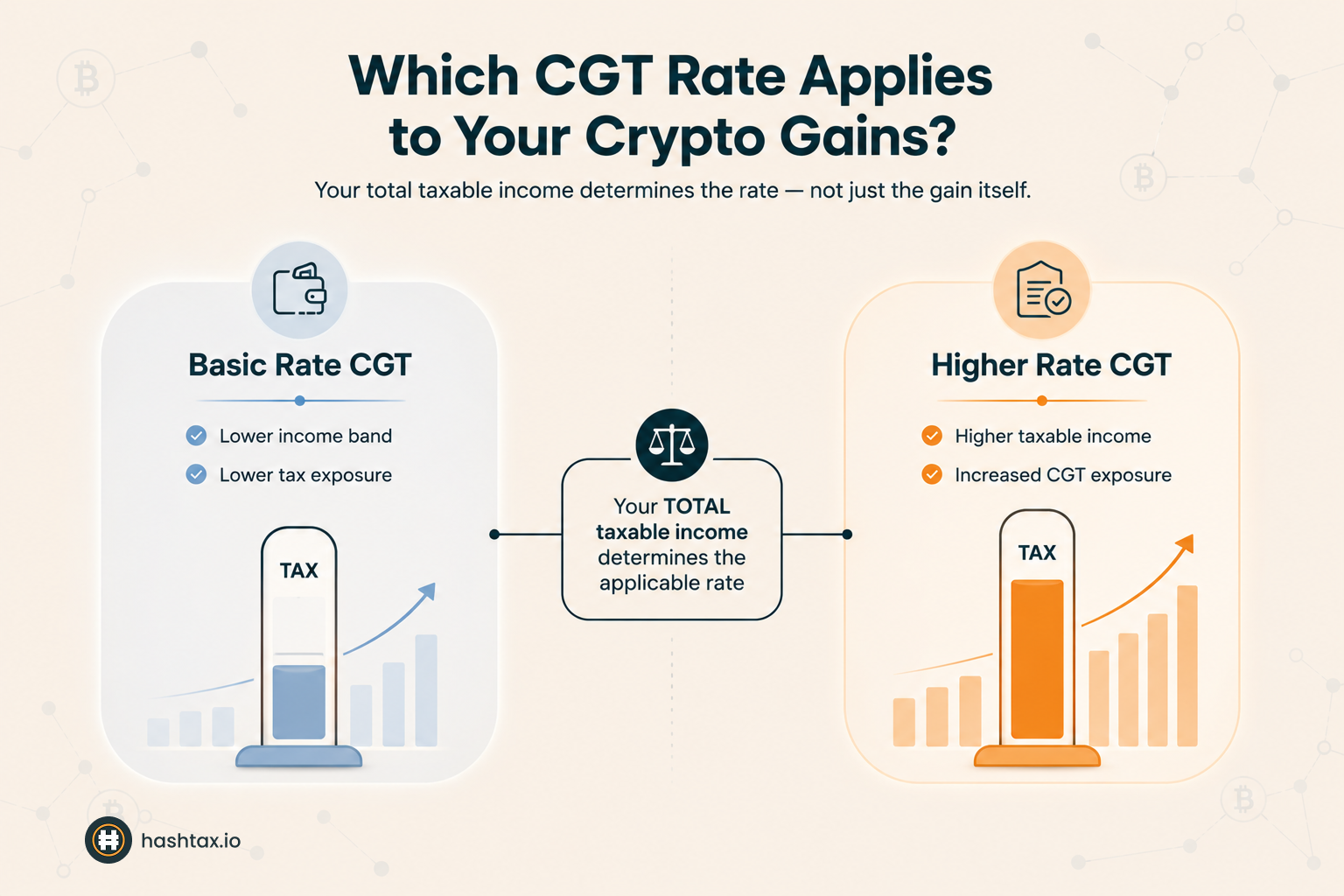

CGT rates on cryptocurrency disposals depend on whether the gain falls within your basic rate Income Tax band or above it.

Note: Rates shown are for 2024/25 following the October 2024 Budget changes. Confirm current rates with a qualified tax professional.

HMRC applies specific rules to determine which acquisition is matched to which disposal. These rules are not optional — they are the legal basis for calculating your gain.

For each cryptocurrency you hold, HMRC requires you to maintain a single pool that tracks the total quantity and total allowable cost of all your acquisitions. When you dispose of part of a holding, you calculate the cost of that disposal as a proportion of the total pool cost.

This means you cannot choose to sell specific batches of a cryptocurrency to optimise your gain. All acquisitions of the same asset are pooled together, and cost basis is averaged across the pool.

If you acquire and dispose of the same cryptocurrency on the same day, the disposal is matched to the same-day acquisition first — before the pool applies. This rule prevents artificial loss creation through same-day sell-and-rebuy transactions.

If you dispose of a cryptocurrency and reacquire the same asset within 30 days, the disposal is matched to the reacquisition rather than the pool. This applies regardless of price movement between the two transactions.

The practical effect: selling Bitcoin at a loss and rebuying within 30 days does not crystallise a loss. The disposal is matched to the subsequent purchase, eliminating the tax benefit of the transaction.

.png)

Depositing cryptocurrency into a DeFi protocol and receiving a liquidity pool token may constitute a disposal of the original asset. The position depends on whether you have disposed of beneficial ownership — a question that requires assessment of the specific protocol.

Withdrawing from a liquidity pool involves a further potential disposal. The treatment of impermanent loss is not definitively addressed in current HMRC guidance and requires professional judgement.

Staking rewards are generally treated as miscellaneous income at the point of receipt, valued at their sterling market value on the date received. This income is subject to Income Tax, not Capital Gains Tax.

A subsequent disposal of those staking rewards triggers a CGT calculation. The allowable cost for that CGT calculation is the sterling value at which Income Tax was originally charged — not zero.

Cryptocurrency received through a hard fork is generally treated as having a nil acquisition cost. Disposal proceeds less nil cost equals the full gain.

Airdropped tokens where nothing was given in return are typically treated in the same way. Where an airdrop requires a service or action in return, the token may be treated as income instead.

These treatments are areas of ongoing HMRC guidance development. Applying the correct treatment requires assessment of the specific transaction and current HMRC published guidance.

Exchanging Bitcoin for Ethereum is a disposal of Bitcoin. Many investors only consider their CGT position when converting to sterling. Every swap is a taxable event and must be recorded.

Selling an asset to realise a loss and immediately rebuying is a legitimate strategy — but only if the rebuy is more than 30 days after the sale. The 30-day rule eliminates the loss if the rebuy falls within the window.

Fees paid at acquisition and disposal are allowable deductions. Many investors do not record these costs, resulting in overstated gains. Platform fees, gas fees, and exchange commissions are all potentially allowable.

All CGT planning strategies — loss harvesting, annual exempt amount utilisation, disposal timing — must be implemented before 5 April. By January, the tax year is nine months complete and most options are gone.

Tokens received through staking, mining, or hard forks do not necessarily have a zero cost basis for CGT purposes. Where Income Tax was paid on receipt, that income value becomes the CGT acquisition cost. Applying zero produces an inflated gain.

The CGT rules for cryptocurrency are technically demanding. Share pooling requires accurate tracking of every acquisition. The same-day and 30-day rules require correct sequencing of matched transactions. DeFi activity involves judgement calls that HMRC guidance does not fully resolve.

A single misapplication of the identification rules can alter your reported gain materially. Professional review ensures the rules are applied correctly to every disposal in your history — not just the straightforward ones.

HashTax provides expert human analysis — not automated software outputs. Our ACCA-registered specialists review your complete transaction history, reconstruct cost basis from source records where needed, apply HMRC identification rules correctly, and prepare your Self Assessment figures with full professional accountability.

The question of crypto tax software versus professional review is worth addressing directly. Software tools can automate data import and produce calculations quickly. They rely entirely on the quality of the data fed into them. Transfer mismatches, incorrect categorisations, and identification rule misapplication produce plausible-looking but incorrect outputs. Professional review catches these errors. Software alone cannot.

All our services are delivered by qualified specialists — we are not an automated software platform. Every engagement involves human review of your transaction history and HMRC-compliant reporting prepared under ACCA professional standards.

Book a free consultation with a HashTax specialist

A HashTax specialist will review your crypto activity and identify whether your CGT position has been calculated and reported correctly. We will confirm which aspects of your history require attention and advise on the most efficient path to a compliant return. There is no obligation to proceed.

Book your free compliance assessment

Path 1 — Immediate: If you have received an HMRC communication about your crypto activity, book an urgent consultation with a HashTax specialist without delay.

Path 2 — Scheduled: If you want to understand your compliance position before the next Self Assessment deadline, complete the Crypto Tax Health Check as your starting point.

Path 3 — Self-Assessment: If you are still assessing your complexity level, use the Tax Complexity Score to determine whether professional review is appropriate for your situation.

HMRC's access to cryptocurrency transaction data has expanded significantly. Exchanges operating in the UK provide transaction data to HMRC under existing reporting obligations. Voluntary disclosure now — before HMRC initiates contact — results in substantially lower penalties than correction after an enquiry opens.

Visit HashTax to learn more about our professional crypto tax services, or book a consultation to speak directly with an HMRC crypto tax specialist.

Your crypto tax compliance matters. Let's address it properly together.

HashTax Specialists

Our team of ACCA-qualified accountants specializing in UK cryptocurrency taxation. We provide expert guidance on HMRC compliance, tax planning, and professional advisory services for crypto investors and businesses.

.svg)

.svg)